Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

In October, global plugin vehicle registrations were close to beating their previous monthly sales record (1,291,000 units), which was just set in September 2023. They reached 1,279,00 units in October. In the end, plugins represented 17% share of the overall auto market (12% BEV share alone). The market share could have been even higher if the overall ICE market hadn’t also been recovering to pre-COVID levels…. It seems that economic crisis or not, people are still buying cars.

Full electric vehicles (BEVs) grew 33% YoY and represented 68% of plugin registrations in October, keeping the year-to-date tally at 70% share.

Plugin hybrids did even better, jumping 46% compared to October ’22, but much of this is due to the range-extended models that are now popping up everywhere in China, with many of these models having batteries of over 40 kWh — which are much more appealing to the public compared to what buyers were used to before. Proof of that is the fact that, if we take out the Chinese market from the tally, PHEVs grew just 11% YoY, or a third of the BEV growth rate….

20 Best Selling EV Models in the World in October

Looking at October best sellers, there were no surprises at the top. The Tesla Model Y was high above everything else, scoring its best first month of the quarter ever, 78,250 registrations, which could mean that December might see the crossover reach a new record.

Behind the Model Y, we have a true BYD armada — 5 models coming from the Shenzhen make. Medal positions went to the Song in the runner-up spot and the Yuan Plus/Atto 3 completing the podium. An interesting note on the Song: the BEV version of the SUV had a record month, 10,832 registrations, meaning that BYD is slowly tilting its Dynasty lineup towards the BEV side. This trend is reinforced by the fact that the Yuan Plus/Atto 3 crossover, Dolphin hatchback, and Seagull city car all hit record performances in October, proving that the most recent BYD growth is coming mainly from the BEV side.

Still on the top half of the table, we have two record performances to celebrate. The #8 GAC Aion Y continued on its record streak, this time with 27,140 registrations. It was the best selling NTNB (non-Tesla, non-BYD) on the table. But the Aion Y’s NTNB monthly titles might start to be challenged soon, as the #9 Wuling Bingo continues on the rise, having delivered a best ever score of 23,744 units last month.

Elsewhere, and as to be expected in a near record month, there were records galore. In the second half of the table, there were several models hitting record results. Starting with the whole Li Auto lineup, with the highlight in particular being the Li Xiang L9 scoring its 3rd record in a row, 12,756 registrations.

Two more models also hit record results. Geely’s Panda Mini, a somewhat cuter take on the Wuling Mini EV formula, scored a best ever score of 13,052 units, allowing it to be 16th in October. And the #13 VW ID.3 had its best result in years, mostly thanks to price reductions in China, which allowed the compact hatchback to reach record heights in that market. (See, Volkswagen — for the right price, people still love you.) Interestingly, the VW ID.3 and its larger sibling VW ID.4 were the only legacy OEM models in October’s top 20, something that speaks volumes to the disruption between the old ICE era, and the emerging EV one.

Outside the top 20, there is plenty to talk about. Going from biggest to smallest, the biggest news in the highest end of the market was the record 11,593 registrations of the AITO M7, a full size SUV with Huawei inside. Still in the 5 meter category, FAW’s Hongqi E-QM5 sedan broke the 5 digit barrier, with 10,021 registrations, all while the Chinese Porsche Zeekr 001 and Denza D9 continued to post solid results, with the former reaching 8,518 registrations and the latter 10,063.

And what about the full size models coming from legacy OEMs? (Crickets….)

In the midsize category, the main highlight is the rise of Xpeng’s G6, the make’s take on the Tesla Model Y recipe. The G6 reached another record score in October, this time 8,741 registrations. Could this new model reach the top 20 soon?

Another fresh model with top 20 prospects is the Lynk & Co 08 PHEV, an original midsize crossover with a 40 kWh battery. For context, 40 kWh is now looking like the bare minimum for plugin hybrids in China. In only its 3rd month on the market, the Lynk & Co 08 PHEV reached 8,038 units.

A mention also goes out to the good scores of the BMW i4 (7,204 registrations), Geely Galaxy L7 (9,336 registrations), Leapmotor C11 (8,772 registrations), and Hyundai Ioniq 5 (8,970 registrations).

As for the compact category, we salute the near record performance from the value for money king, the MG4. It scored 10,026 registrations this month. Still in this category, Great Wall’s Ora Good Cat continues on a high note, in no small part thanks to export markets, getting 9,241 registrations.

In the compact crossover category, it was a rare ray of light coming from European brands, with both the Audi Q4 e-tron (11,352 units) and the Skoda Enyaq (8,570 units) hitting record scores, helping along Volkswagen Group’s fortunes. Meanwhile, the Volvo XC40 (7,905 units) continues to hold the fort down, at least until the much anticipated EX30 lands.

Finally, in the tiny city EVs category, Chery’s take on the Wuling Mini EV, the originally named QQ Ice Cream, registered 7,111 sales, confirming the popularity of the tiny Wuling formula in China. Maybe it is time to export the formula to overseas markets?

Top 20 EV Models YTD

In the year-to-date (YTD) table, the podium is already pretty much decided. The Tesla Model Y has almost twice the sales of the runner-up BYD Song, while the Chinese model is profiting from a sizable advantage of 80,000 units over the bronze medalist Tesla Model 3, which in turn also has a safe 47,000-unit advantage over the #4 BYD Qin Plus.

This will mean that the 2023 podium will be exactly the same as the 2022 edition. The Tesla Model Y will win its second title in a row, followed by the BYD Song, which will earn its second silver medal, all while the Tesla Model 3 gathers its second consecutive bronze medal — after winning the best seller title four times in a row from 2018 to 2021.

Below the podium, another point of interest for the last quarter of the year is around the 7th position. The GAC Aion S had a slow month in October, and because of it, the competition came significantly closer, especially its sibling, the rising GAC Aion Y, which jumped two positions to 8th. Additionally, the #9 Wuling Mini EV and #10 BYD Han could profit if the Aion S doesn’t step up its deliveries again.

But the dark horse in this race is the BYD Seagull, which climbed another position, to #11. The city model is poised to join the top 10 in November — and maybe (who knows?) reach the 7th position by year end.

A few positions below, the Wuling Bingo was also up one spot, in this case to #14. While not experiencing the same level of success as its BYD competitors, the Dolphin and the Seagull, Wuling’s supermini is a much welcome addition to the EV market. And it just begs to be exported. With GM allergic to small cars — just look at the neglect the Bolt is getting — Shanghai Auto could well sell it as an “MG 2” in export markets….

The last positions on the table should have a reshuffle in November, with Li Auto’s L7 probably surpassing the Denza D9 by then, and its 7-seat XL sibling, the #29 Li Xiang L9 (87,509 registrations) probably surpassing the #20 Audi Q4 e-tron next month.

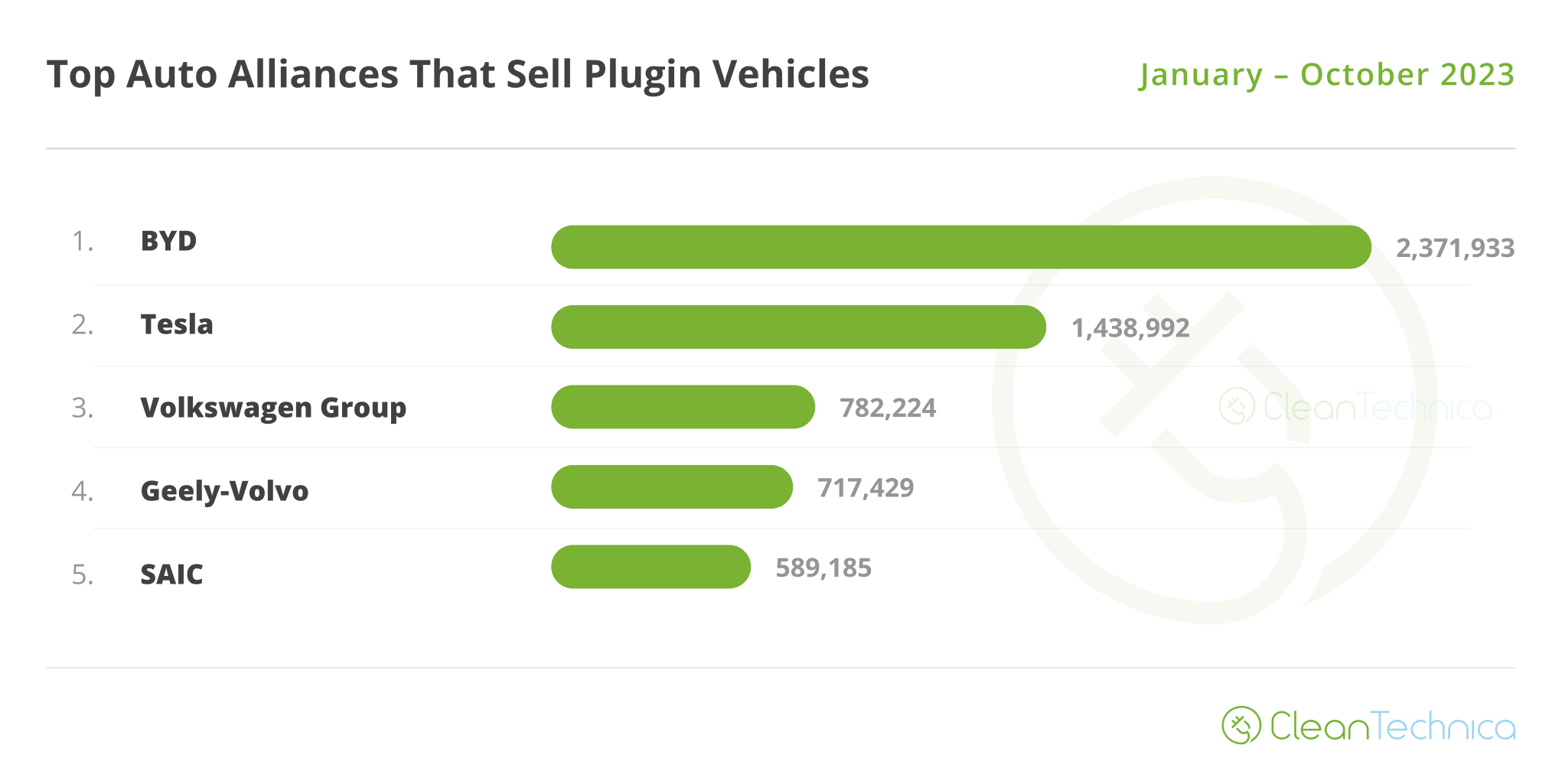

Top Selling Brands

In October, BYD continued its never-ending record streak, thanks to a 289,000-unit performance. It was the 6th record in a row for the Shenzhen make. Tesla went back to its normal self, delivering 115,000 units, a normal result in the first month of the quarter for the brand.

Below the top two galactics, this time we have the SGMW JV ending the month in 3rd, banking on its newfound dynamic duo (Wuling Mini EV & Bingo) to end ahead of the competition. And with a record to boot (54,921 registrations).

#7 Li Auto continues to go from strength to strength, with yet another record month, its 7th in a row. Li Auto had over 40,000 registrations thanks to record results across the lineup. With the startup brand still supply constrained, expect the high-end company to continue beating records regularly in the remainder of the year. But the real fun will start when the midsized L6 SUV and L5 sedan land sometime next year. Oh, and the cherry on top of Li Auto’s cake is a certain bullet train Mega MPV … with mega specs.

Just below it, #8 Changan also hit a record month, much thanks to the success of the little cutesy Lumin and the Deepal S7 SUV. Another record performer was #9 Geely. Thanks to great results across the board, not the least the record score of the Panda Mini, and also the 9,336 units of the Galaxy L7, Geely reached 38,000 units!

Still on Geely’s galaxy of brands, while #14 Volvo had a somewhat meh! result, with just 21,332 registrations, the record score of #20 Zeekr hasn’t gone unnoticed. Its 13,078 registrations allowed Geely to have the most brands — three — in the ranking. The Chinese Volkswagen is rising….

Speaking of Volkswagen, its premium brand, Audi, scored a year best result, 25,577 registrations. But in the private race between the Three Marys (BMW, Audi, & Mercedes), the four-ring brand is still in last place, and far below leader BMW. BMW scored an extra 18,000 units in the same period. The reason? While Audi has only three EV models, of which only the Q4 e-tron and Q8 e-tron can be considered volume models, BMW has twice as volume models on sale (iX1, iX3, i4, iX, and don’t forget the Chinese i3). Even if BMW doesn’t have a star player like the Audi Q4, the combination of those models is enough to easily outsell Audi. The upcoming Audi A6 e-tron and Q6 e-tron are badly needed….

Another big surprise was #15 XPeng, which had its best result ever, 20,002 registrations. The company saw its star player, the G6, shine. It scored another record. Its bigger SUV, the G9, was also up. So, hopefully the Chinese startup will start to have more consistent results.

Another OEM on a record streak is Leapmotor. Thanks to the success of its C11 SUV, Leapmotor scored its third record score in a row, 18,269 registrations. One can say that Stellantis has made a good choice, eh?

In the YTD table, there isn’t much to report regarding the top two positions. BYD is well ahead of Tesla, and both are in a galaxy of their own. The two makes together are responsible for more than one third of the global plugin vehicle market.

Far below these two, which are really in a league of their own, there could be an interesting race for the last place on the podium, Currently, you have GAC Aion in 3rd, which allows it to be the NTNB (not Tesla, not BYD) best seller.

But with the Chinese make experiencing a slower than usual month in October, it has allowed #4 BMW to gain a bit of ground on it. With 13,000 units separating the two, and two stages to go, the German make is hoping that GAC Aion continues in the slow lane, which could allow BMW to steal the bronze medal in the last days of the year.

It is a tall order, and the most likely outcome is for the Bavarian brand to stay in 4th, but if it did manage to pull this off, that would be the first podium presence for BMW since 2016!

In fact, European brands have a poor record when it comes to podium presences in the EV manufacturer ranking. The last one was in 2020, with the #2 spot of Volkswagen, and before that, it was the aforementioned #3 spot of BMW in 2016.

And before that, we need to go waaay back to 2010 to find the Norwegian brand Th!nk, which crossed into EV Heaven back in 2012, in order to find the last podium presence from a European brand. Th!nk had been 3rd that year, behind Tesla in 2nd, while the #1 EV make that year was … Mitsubishi! Yep, there was a time when this Japanese manufacturer was a leader in the EV arena. Hard to believe, right?

“But, when was the last time a European brand won this title?,” one or two of you may ask. The answer is: 2008. Again, that was thanks to the Norwegians and the Th!nk brand.

Coming back to 2023, the first half of the table does not have a lot to talk about, with the main point of interest being the #7 spot, where Mercedes could be pressured in December by a rising Li Auto. The Chinese startup is breaking records every single month, so it could end up surpassing the German make in the last days of December.

The remaining highlights were Kia surpassing its stablemate Hyundai to take the 13th spot, and NIO climbing to #17, surpassing Ford, which experienced a slow month but nevertheless stayed at the front of the race for best selling US legacy OEM.

Looking at registrations by OEM, leader BYD was comfortable at 22.1% share, up 0.2%, while Tesla was down by 0.6%, to 13.4% share.

3rd place is in the hands of Volkswagen Group (7.3%, up from 7.2%), which is keeping itself a good distance ahead of rising #4 Geely–Volvo (6.7%, up from 6.1%). The German OEM profited from great performances with several of its brands, starting at Geely, passing by Lynk & Co, and ending at Zeekr.

While we are too close to the end of 2023 to see the Chinese conglomerate pressure #3 Volkswagen Group, the 2024 race should see an interesting duel between these two in the race for the NTNB title.

As for #5 SAIC (5.5%, up from 5.4% in September), the share drop stopped and seems to be reversing. That was not the case for Stellantis, which is stable in 6th position but saw its share drop by 0.2% to 4.4%.

Below the multinational conglomerate, things are more interesting. #7 BMW Group (4.1% share) kept its position, and even gained ground over #8 GAC (4%, down 0.1%) and #9 Hyundai–Kia (3.9%, down from 4%).

Looking at where the ranking was a year ago, we can see that both of the top two brands gained share, 4.1% in the case of BYD and 0.6% in the case of Tesla. The other beneficiary was Geely–Volvo, which in the meantime surpassed SAIC and added 0.9% of share on the way.

On the losers side, Volkswagen lost 0.7% share year over year (YoY), while SAIC dropped two full points in share, from 7.5% a year ago to its current 5.5%.

Looking just at BEVs, Tesla remained in the lead with 19.3%, down from 20.1% in September. The US make still has a comfortable lead over BYD (16.3%, up from 15.9%), making it unlikely the Chinese automaker will be able to remove Tesla from the BEV throne in the last two stages of the race. The US automaker gained a precious lead in the first half of the year.

Next year, however … it isn’t much a question of if, but more of when. I do not expect it to happen in Q1, as the Chinese market will have new year festivities that will surely slow down BYD’s sales, but Q2 should probably signal the inflection point where BYD surpasses Tesla in the BEV race.

In the last place on the podium, Volkswagen Group (7.8%, up 0.1%) kept some distance over SAIC (7.6%, up from 7.5%). Expect an entertaining race between these two in the remainder of the year.

In 5th, we have a position change. Benefitting from a slower than average month from GAC (5.6%, down from 5.7% in September) — and a quite strong October across the several brands in its galaxy — Geely–Volvo surged from 5.6% share to its current 6.2% share, allowing it to not only surpass GAC, but probably also secure the #5 spot by the end of the year.

Finally, comparing the current picture with what happened three months ago, Tesla’s drop due to the Model 3 refresh is evident (-1.6% share). While BYD’s market gains are relevant (+0.7%), Geely–Volvo’s market share grab (+0.5%) is definitely more impressive, as it starts from a much smaller base.

India

Finally, at the request of our readers, here is a second chapter on the health of some major automotive blocs….

“A healthy market is one where there aren’t monopolies, and diversity breeds innovation.” A few words are due for India and a few other emerging countries.

Looking at India’s EV industry, it reminded me of an article on estimated GDP from a historical perspective. In it, it said that even at the height of the all-mighty Roman Empire, the Mediterranean civilization wasn’t the largest economy of the time. It wasn’t even the 2nd largest. It was the 3rd, behind China and … India. That’s right, throughout several centuries, these two civilizations were the biggest economies in the world, so the fact that China and India are returning to the top of the economic pyramid is just a return to normal.

You might ask, “So, will this mean that the Indian EV industry will replicate China’s current success story?” Then I would say, “Well, not so fast.”

While there is the potential for it, and I am sure the local government is looking to do so — just look at the recent maneuvers regarding Tesla — India is starting from a weaker place than China.

First of all, there’s the timing. If India does get to be in a position to challenge the current status quo, it will do so in a position where the train is already running fast, something that wasn’t the case in 2015 when BYD won its first manufacturer title. There was no Tesla Model 3 at the time and and Volkswagen’s “Dieselgate” had just happened.

Second of all, there’s the strength of the local automotive industry. Ten years ago, China already had 8 local brands among its domestic top 20. A few of them are currently well known, like Changan, Wuling, Chery, and a certain BYD. So, there was plenty of fertile ground to grow a thriving EV industry.

Looking at the current ranking in India, we have … two local brands. Those are Mahindra and Tata.

Looking at Mahindra, it has only one EV, the small crossover XUV400. And while the specs themselves aren’t too bad (40 kWh battery, 456 km range, according to local cycle), it kind of reminds of the Chevrolet Bolt or BMW i3 — in the way that it is a model for early adopters, but not thought through as being part of a more global electrification plan.

Regarding Tata, things are bit more ambitious. It has a small family of EVs, with the Nexon EV small crossover (in 41 kWh and 30 kWh flavors) as the more premium offering, and then the small Tiago/Tigor EVs (24 kWh battery) being the budget choices.

But both brands aren’t really cutting edge when it comes to EVs, and their domestic career profits from the fact that it is a peculiar market, where most foreign brands have some difficulty succeeding, while the local brands have even more problems in selling their models overseas.

Tata could have some precious help from the Jaguar–Land Rover connection. The problem with that is that Jaguar–Land Rover is also scrambling to understand on how to make its own EV transition.

So, while I can see India having a significant EV industry in the future, it won’t be close to what China has right now. It just misses diversity and/or commitment.

Vietnam & Turkey

Finally, I would like to leave a few words on Vietnam’s (VinFast) and Turkey’s (Togg) EV startups.

There are three main differences between the two brands. The first regards timing, as VinFast started with a year and a half of advance, so its EV plans are more developed than Togg’s. The second regards where they were born. The Vietnamese auto market is one third of the Turkish one, so ViMFast’s EVs are more dependent on exports than Togg’s. And finally, the third regards the ambitions that each brand brings. VinFast in two years has launched six(!) EVs, with a seventh model coming a year from now, while Togg is taking a different approach, with the second model, the T10 S sedan, only expected in 2025, two years later than the current T10X SUV.

So, while VinFast is expecting to emulate the Chinese model by launching a plethora of EVs as soon as possible, and aims to start exports relatively soon with them. Due to the small size of its domestic market, Togg is taking its time, with a second model only coming when the first has reached maturity. Export plans aren’t a priority for now, with the first units only expected to be sent to European markets in 2025, two years after the EV was launched in Turkey.

As such, while VinFast is going in a somewhat risky strategy of fast growth, Togg is being more conservative, looking to iron out the kinks first before going into the more troubled waters of export markets and multiple models.

Who is going to best succeed? Please place your bets.

One thing is certain, though, as these two cases prove: the EV business is more open to new players and new geographies, Soj once the EV transition is done, it is likely that we end up with a more diverse and fragmented automotive landscape than in the previous ICE era.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

CleanTechnica Holiday Wish Book

Our Latest EVObsession Video

I don’t like paywalls. You don’t like paywalls. Who likes paywalls? Here at CleanTechnica, we implemented a limited paywall for a while, but it always felt wrong — and it was always tough to decide what we should put behind there. In theory, your most exclusive and best content goes behind a paywall. But then fewer people read it!! So, we’ve decided to completely nix paywalls here at CleanTechnica. But…

Thank you!

CleanTechnica uses affiliate links. See our policy here.