Graphite, a crystalline form of carbon, is a crucial component of lithium-ion batteries. It is the sole material, besides a small amount of silicon, in the anode, the battery’s negative terminal that makes up 50% of the cell.

Graphite is therefore imperative for the energy transition. Yet, unlike other similarly critical minerals such as lithium and cobalt, it has hit the headlines much less. This is because, unlike the other two, graphite is relatively abundant.

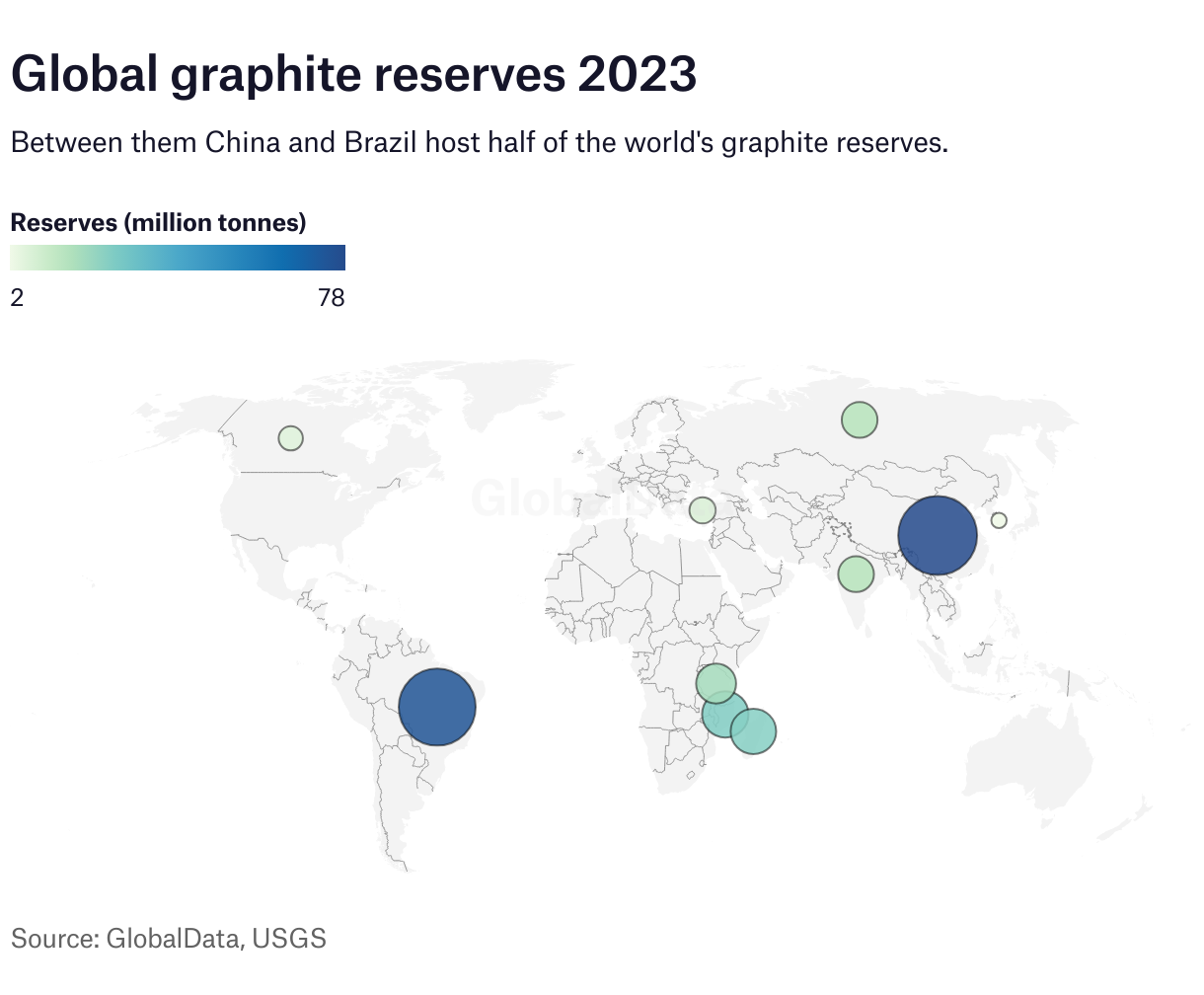

The US Geological Survey estimates there are 800 million tonnes (mt) of recoverable graphite reserves globally, though the US’ share is small. Despite this, graphite supply is monopolised by China, as it is for other battery-integral minerals. Chinese production accounts for 77% of all graphite production and 97% of global anode output – meaning almost all non-Chinese-produced graphite is sent to the country for processing.

The US Government, which has a target of 56% of all new US vehicles sold to be electric by 2032, is starting to take this monopoly seriously, scaling up incentives for battery makers to diversify their supply chain away from China.

To spur development, the US has reinstated 25% tariffs on natural and synthetic graphite anodes sourced from the country, which it designates a ‘foreign entity of concern’. Natural graphite processed in China will have the same tariffs from 2026.

The US will also end a waiver on allowing vehicles with batteries containing Chinese graphite to continue to qualify for generous federal subsidies under the Inflation Reduction Act (IRA) in 2027.

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Your download email will arrive shortly

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalData

These moves present a notable opportunity for the mining and upstream processing sector – but as the projects currently in development are finding, it is not always easy competing with their Chinese counterparts.

Projects start to emerge

In the US in 2019, only a few battery factories existed, but today there around 34 either planned, under construction or operational in the country. Yet while a non-Chinese supply chain for other, more complex core battery minerals for the cathode (cobalt, lithium) has emerged in response to this growing market, it hasn’t for graphite.

“This is most likely because China has an established ecosystem and suspected generous government subsidies making production cheaper. But to me, that is not an excuse for non-Chinese firms not to have emerged,” says Ross Gregory, partner at advisory business New Electric Partners. “Especially as it is less complex to make active anode material than cathode,” he adds.

This is slowly changing, however, as several projects get under development. One of these is operated by Syrah Resources, which is setting up a small processing facility in Louisiana and mining natural flake graphite in Mozambique. Canada-based Nouveau Monde Graphite is producing graphite from its Matawinie mine in Quebec and is developing a manufacturing plant in the same region that will produce 43,000 tonnes per annum (tpa) of active anode material when operating.

US-based Urbix is developing a commercial-scale processing plant in Arizona, which it plans to bring online in 2027 to produce battery-grade graphite. The company says it is currently in active negotiations with a site for a facility that will produce 30,000tpa. It has secured some conditional offtake and early-stage agreements and has investment from Appian Capital, which has graphite mines in Brazil. Urbix is also building a demonstration pilot plant in Arizona.

The graphite price differential

Northern Graphite, which has a graphite flake mine in Canada, is also looking to develop an anode processing plant in the country, as well as a graphite mine in Namibia it hopes to restart next year. CEO Hugues Jacquemin says defining more clearly what is a ‘foreign entity of concern’, as well as plans to restrict subsidies if graphite material from one is used in US batteries, has really pushed the dial for a supply chain to start to emerge.

“What the tariffs do is raise the bar for pricing these materials in the region, and that creates a more fertile environment for us to attract investment and to develop the supply chain in North America,” he says.

However, raising capital for these projects is still challenging, he adds, because their cost structure is higher than in China. There is also uncertainty around the election and the fact that some of the incentives will come into force afterwards.

The average selling price for the company’s natural graphite flakes is around $1,500 per tonne (t), compared with around $600–800/t in China. To commercially process the material in Canada, the company needs to sell it for $8,000–10,000/t , says Jacquemin. Today, it can be bought in China for $6,000–7,000/t. Factoring in the 25% tariff, the product becomes more competitive on the lower end of the scale, he says.

“Battery and EV [electric vehicle] makers are not too happy paying more for their material. Their argument is, why do we need to pay more and develop a local supply chain when there is one available in China? The answer is because that supply chain is not secure,” he says.

Patrick Ahlm, a communications manager at Urbix, believes, however, that the IRA credits are motivating battery makers and OEMs to establish a domestic supply chain – and, in turn, investors such as Appian are becoming motivated to develop projects in the US.

“I think our challenge is to scale up our technology and demonstrate it at commercial scale, then continue through the testing and validation work with battery makers,” he says.

Ahlm adds that the graphite anode the company eventually produces will be competitive with China with the tariffs, but the ambition is to not be reliant on them, but for them instead to be ‘sweeteners’.

Gregory agrees higher costs shouldn’t be a barrier in the long term.

“This is the case with every component [when] compared with China’s pricing, graphite is not alone – and remember the graphite anode expenditure only makes up around about 8–9% of the battery cost, so it should be the least price sensitive component.”

The ESG factor

It is not just tariffs and subsidies that could drive the development of a non-Chinese supply chain, however. As environmental, social and governance requirements become more stringent, Jacquemin believes the graphite and graphite anodes Northern Graphite will produce will be attractive to OEMs because of their lower carbon footprint. A smaller supply chain and the use of hydroelectric power means the graphite produced will be much more environmentally friendly.

“We believe the higher price we would charge would be viewed by customers as attractive because of the lower CO2 footprint, but not just this, [with China] there are [potential] issues around environmental protection, remediation, labour and much less transparency overall,” he says.

Similarly, one of Urbix’s selling points is its unique process that doesn’t require hydrofluoric acid, making it much less damaging to the environment.

In a similar vein, the anode market is composed of both synthetic and natural flake graphite, currently split around 65:35, respectively. However, there is an expectation that natural flake graphite demand will increase because synthetic graphite is more expensive and much more carbon intensive to produce because it is made from pet coke or other hydrocarbons. Natural flake graphite, on the other hand, is simply mined, concentrated and then purified.

Getting non-Chinese graphite projects over the line

Non-Chinese graphite anode supply is still nascent. To continue to support its development Gregory says it is important there are no more extensions to the IRA subsidy regime.

“If you really want to set up a non-Chinese supply chain, you have got to be ruthless in your implementation of that [IRA] legislation. Governments should be putting money in at the project level, such as equity, or at least authorising pension funds and the like to take some equity risk around mining projects,” he says. “That means they have got to pick winners, but I think there is no choice, and that is how it works in China – they pick winners.”

Overall, there is optimism around the potential to grow the graphite industry further and faster. Graphite can be obtained widely, and mining it is much cheaper than mining the cathode components like cobalt and lithium.

Furthermore, despite EV uptake being slower than expected, the transition is considered inevitable, but experts agree more urgency is needed.

“It takes time to develop a mine, build the processing facility, to qualify the material [it must be tested by the battery maker]. It is important the government understands the sense of urgency,” says Gregory.

China could restrict or ban the export of graphite at any time. It already does so to some extent by requiring export licences from last year. In fact, from 2022, exports from the country have fallen from 81,000t to 58,000t in 2023.

Furthermore, global demand is projected to grow. Jacquemin says his company forecasts hat by 2030 the demand for graphite will be six to seven times what it is today. Similarly, Statista estimates that by 2025, batteries will demand nearly 700,000t of natural graphite, up from 133,000t in 2018.

“There really is no time to waste,” says Jacquemin.