Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

Tesla is the best selling brand in Europe, but Volkswagen Group is the #1 OEM

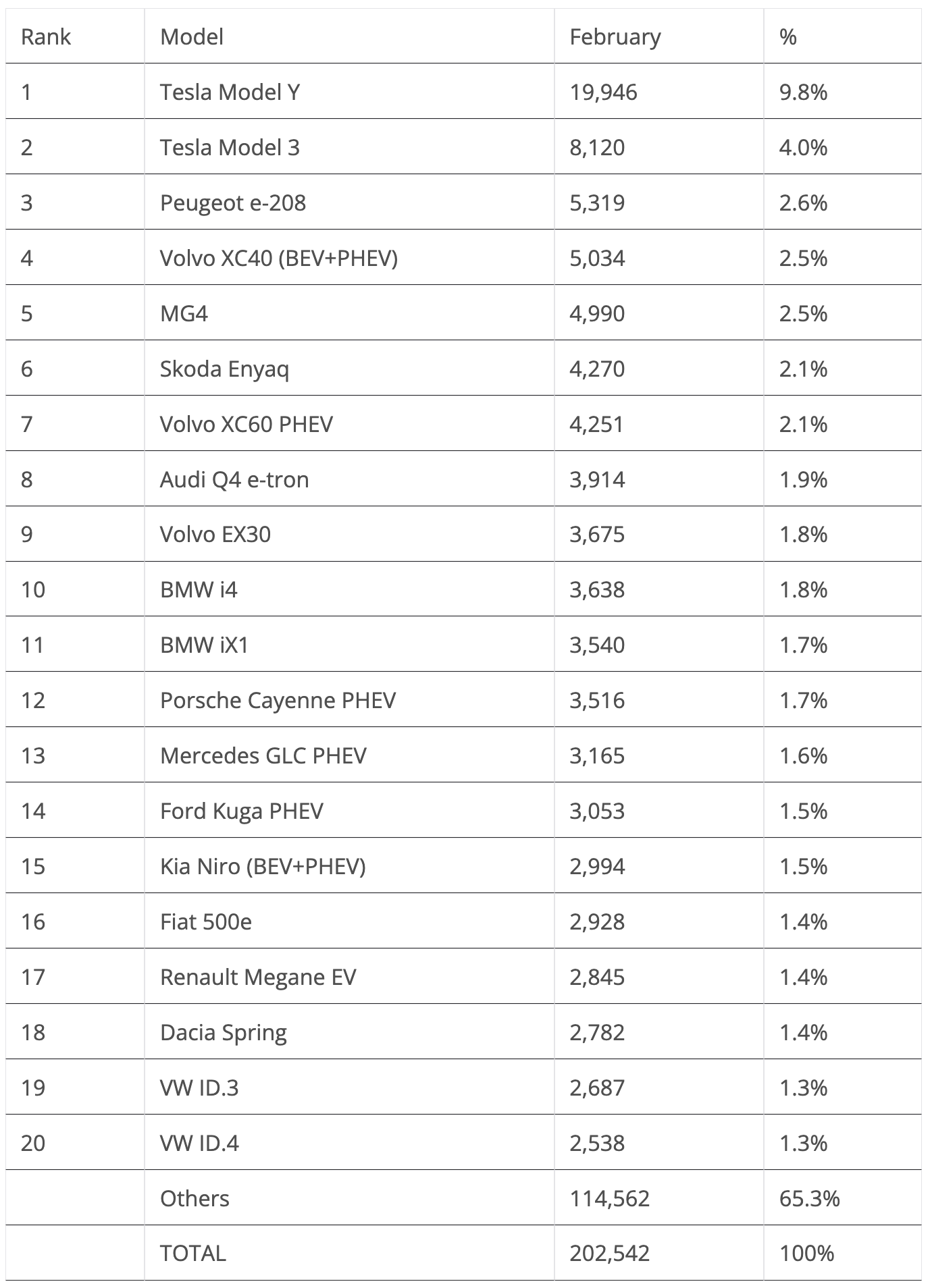

Some 202,000 plugin vehicles were registered in February in Europe — which is +10% year over year (YoY). Unfortunately, it was the same growth rate in the overall market, +10%, so there were no real gains when it comes to EV market share.

Last month’s plugin vehicle share of the overall European auto market was 20% (13% full electrics/BEVs). That result kept the 2024 plugin vehicle share at 20% (13% for BEVs alone).

BEVs (+10%) and PHEVs (+9%) grew at similar rates, as the BEV market is currently in a sort of no man’s land. It is still feeling the pain of the end of incentives in a number of countries, especially in Germany. On the other hand, new mass-market EVs (the Renault 5, Citroen e-C3, etc.) are still not on the road. Expect this to ease in Q2, but significant growth should only come in the second half of the year.

Looking at the other powertrains on the market, plugless hybrids are the fastest growing technology (+24% YoY), and they represented 29% of the total market in February. Added to the 20% of plugin vehicles, one can say that half of the European car market is already electrified, in some way. But for some to grow, others must come down, and diesel (-5% YoY) is the starkest example. Diesel vehicles had only 12% of the European passenger car market in February, a far cry from the 50% share it had in 2015 or the 55% average it experienced before that. At this rate, in this category, diesel will be dead by 2027, well before the 2035 ICE ban….

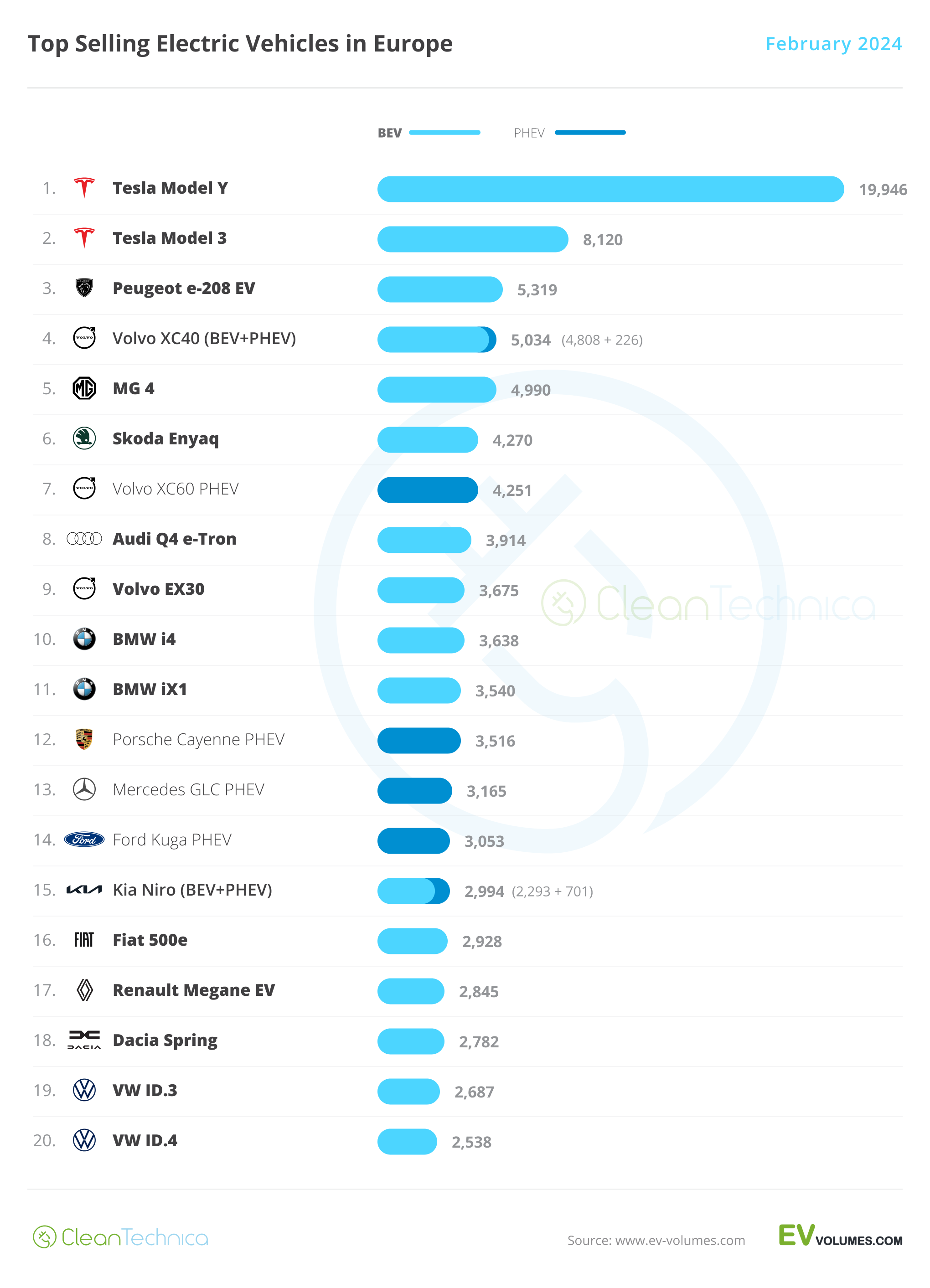

The highlight of the month was the Peugeot e-208 jumping into 3rd. But let’s look closer at February’s plugin top 5:

#1 Tesla Model Y — For the nth month in a row, Tesla’s crossover was the best selling EV in Europe. In February, the midsizer had 19,946 registrations. This year could be considered “Peak Model Y” in Europe. The midsized crossover should continue to post similar results in the coming quarters in Europe, but do not expect sales to increase significantly over current volumes, as I am confident the Model Y has already reached the market’s natural limits. Also limiting its growth will be the refreshed Tesla Model 3, which might steal some sales in some markets, even if Europeans aren’t really into sedans these days. Regarding last month’s performance, the Model Y’s biggest European markets included Germany (5,482 units) and France (1,982 units), with the UK (1,759 units), Norway (1,749), Belgium (1,737), and Italy (1,252) being the remaining countries posting four-digit results.

#2 Tesla Model 3 — The Tesla sedan won another podium position in February thanks to 8,120 registrations. With demand recovering, due to the recent refresh, the Model 3 now has enough volume to stay in the #2 spot in 2024. It is benefitting from currently slow demand from the local heroes. But, will it stay there through the end of the year? That will depend more on the others’ capability to recover (see: VW ID.4 …) or ramp up production (see: Renault 5 …) than on the Tesla model’s performance, as it is now in full maturity. Regarding the Model 3’s February performance, its main markets were the UK (1,410 registrations), France (1,216 registrations), and … Portugal(!), with 762 deliveries.

#3 Peugeot e-208 — The French hatchback is a sure value in the EV arena, but the Peugeot EV had a bumpy road in the past few months, in no small part due to the recent refresh, which created some delivery hiccups. These seem to already be a thing of the past, as the model had 5,319 registrations in February, its best result since last September. Expect sales to continue strong in the coming months now that the model’s production constraints seem to have ended. Regarding the 208’s February results, the distribution of deliveries show a big push in its domestic market, with France (4,132 units) being responsible for over 75% of deliveries. France was followed from afar by the Netherlands (326 units) and Italy (173).

#4 Volvo XC40 (BEV+PHEV) — Although it didn’t reach record sales levels, the compact Belgian-Swede had a positive month, allowing it a top 5 presence. This is even more impressive considering that its younger (and cheaper) sibling, the EX30, is already ramping up — Volvo’s newest model ended February in 9th, with 3,675 units. With 5,034 sales, 4,808 of them belonging to the BEV version, it seems the XC40 is not being too cannibalized by its younger sibling, which will allow it to go on as Volvo’s cash cow in the EV arena. Looking at February’s performance, the highlight is the Netherlands (1,367 registrations), but Germany (532 registrations), Belgium (636), and Sweden (561) also deserve a mention.

#5 MG4 — The compact hatchback is fulfilling MG’s best expectations, proving right its dragon-slayer nickname and earning another top 5 presence in February thanks to 4,990 registrations. With original looks, good handling, and good enough interior materials, the 2023 CleanTechnica Car of the Year for Europe is sort of the electric Ford Focus that the US brand has refused to make. With Dearborn’s European arm now little more than an extension of the US marketing team (SUVs = Freedom & Americana), there is a hole in the B and C segments for mainstream hatchbacks with a focus on good handling and smart design. With the MG4 now filling the role of the electric Ford Focus, who will fill the role of the electric Ford Fiesta? But I digress. Back to the MG4’s February performance. Its main markets were Germany (1,503 registrations), France (1,491 registrations), and its adopted home market of the UK (850 registrations). Incidentally, these are three big markets for hatchbacks.

Looking at the rest of the February table, the highlights go to two record performances. The #9 spot of the Volvo EX30 was celebrated as the first of many in the top 10 for the compact crossover, thanks to a record 3,675 sales, and expect the Polestar-looking Volvo crossover to continue climbing in the table, with top 5 presences likely in the next couple of quarters.

But the most unexpected record performance came from the #12 Porsche Cayenne PHEV, with the German SUV scoring a record 3,516 sales. That allowed it to be both February’s best selling full size model and that month’s 2nd best selling PHEV model, only behind the #7 Volvo XC60 PHEV. The midsize Swede, meanwhile, was the 3rd Volvo model on the top 10 in February. Regarding the Cayenne’s performance, the refresh of the current generation is proving to be a real success, especially thanks to the improved specs (26 kWh battery) of the PHEV version. A good omen for the upcoming Porsche Macan EV?

The BMW iX1 also had the opportunity to shine, ending the month in 11th with 3,540 registrations. We should also salute the return of the VW ID.4 and ID.3 to the table, in … #20 and #19, respectively.

Below the top 20, there wasn’t much to talk about, with the highlight being the new-generation Hyundai Kona EV. With 2,076 deliveries in February, it is looking to return to the table soon.

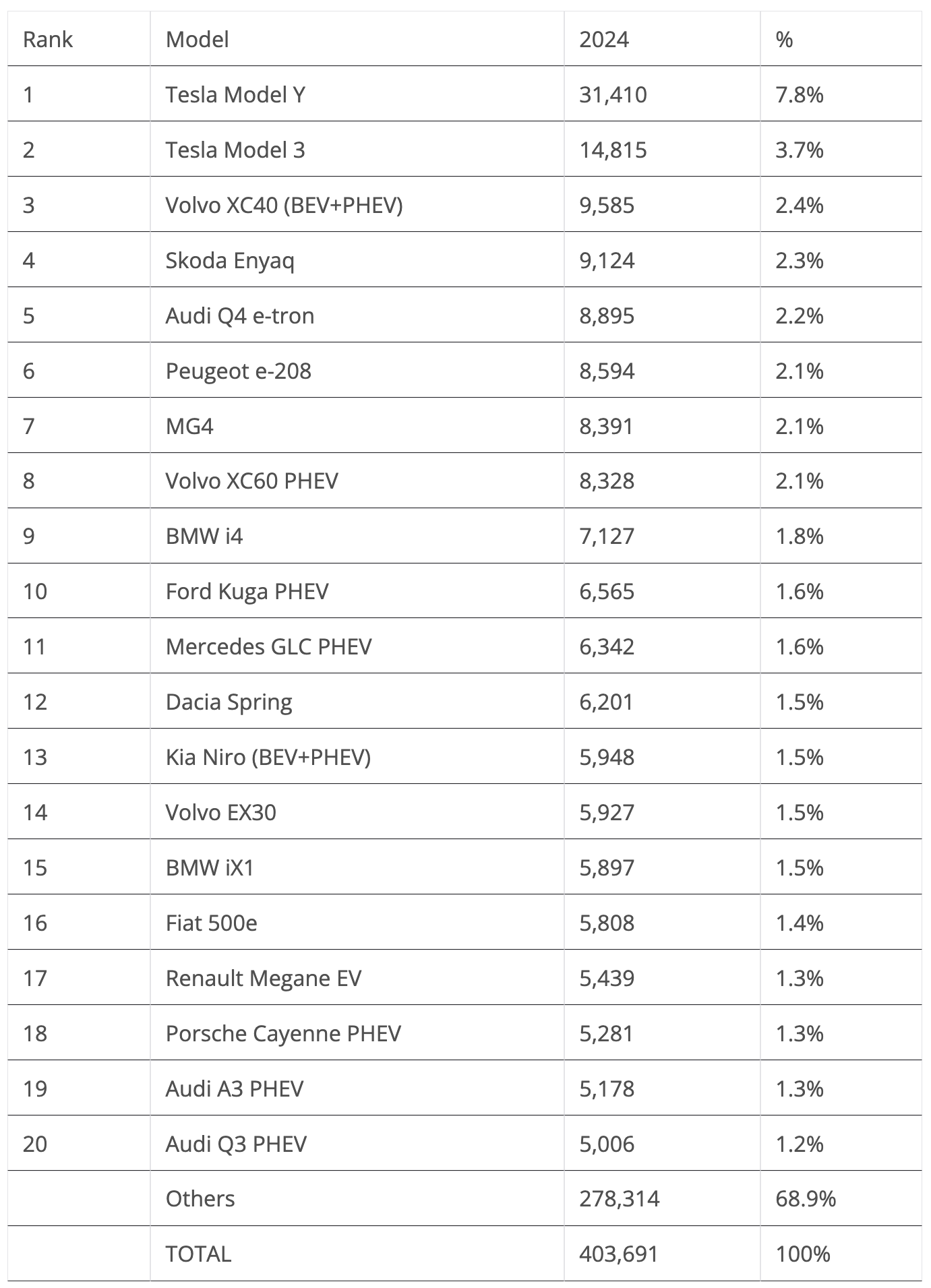

Looking at the 2023 ranking, with the Tesla Model Y having twice as many deliveries as the runner-up Tesla Model 3, the attention is now focused on the remaining podium positions.

On that topic, the Volvo XC40 jumped two positions in February, to 3rd place, ending the month with an advantage of some 400 units over the #5 Volvo XC40, but with 5,000 registrations fewer than the current runner-up, the Tesla Model 3.

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Elsewhere, the Climber of the Month was the Peugeot e-208, which jumped five positions to 6th. The French hatchback is set to climb a couple more positions in the following months. The Mercedes GLC PHEV continued to climb up the table, having risen one position in February to #11.

In the last positions on the table, there were a few new entries, like the BMW iX1 in #15 and the Porsche Cayenne PHEV in #18, but without a doubt, the most important is the 14th position of the Volvo EX30, a model destined for stardom. The Swede is surely looking to join the top 10 soon.

Still in the top 20, the Renault Megane EV was up to 17th. An important absence is the VW ID.4, 3rd in 2023. Due to a slow start to this year, it is still off the table. Maybe March will bring it (and the ID.3) onto the best sellers table?

In the auto brand ranking, Tesla is leading with a comfortable 11.6% share of the plugin market, while BMW is in the runner-up position with 10.2%, down 0.1% compared to the previous month.

3rd placed Mercedes (8.7%, down from 9%) has kept its podium position, but the lead over #4 Volvo (8.1%, up from 7.8%) has decreased, so a lot can still happen between them.

Finally, Audi (7.2%, down from 8.3%) dropped to 5th and is losing share by the day. So, we might see #6 Volkswagen (5.1%, up from 5% in January) surpass it sometime in the future.

A sign of the current times, all top 5 brands are premium makes, with the best selling mainstream brand, Volkswagen, only in 6th.

Arranging things by automotive group, Volkswagen Group was down to 19.5%, from 20.5% in January, keeping a comfortable lead over runner-up Stellantis (12.2%, up 0.2% from the previous month).

#3 Tesla had 11.6% share, and expect the US automaker to try to go after the #2 position in March, looking to profit from Stellantis’ apparent weakness.

Off the podium, #4 BMW Group was down to 10.9%, while #5 Geely–Volvo continued on the rise, gaining 0.3% share and climbing up to 9.9%.

With #6 Mercedes-Benz Group (9.2%, down from 9.5%) losing share, Geely is comfortable in its #5 spot in the next few months.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica TV Video

CleanTechnica uses affiliate links. See our policy here.