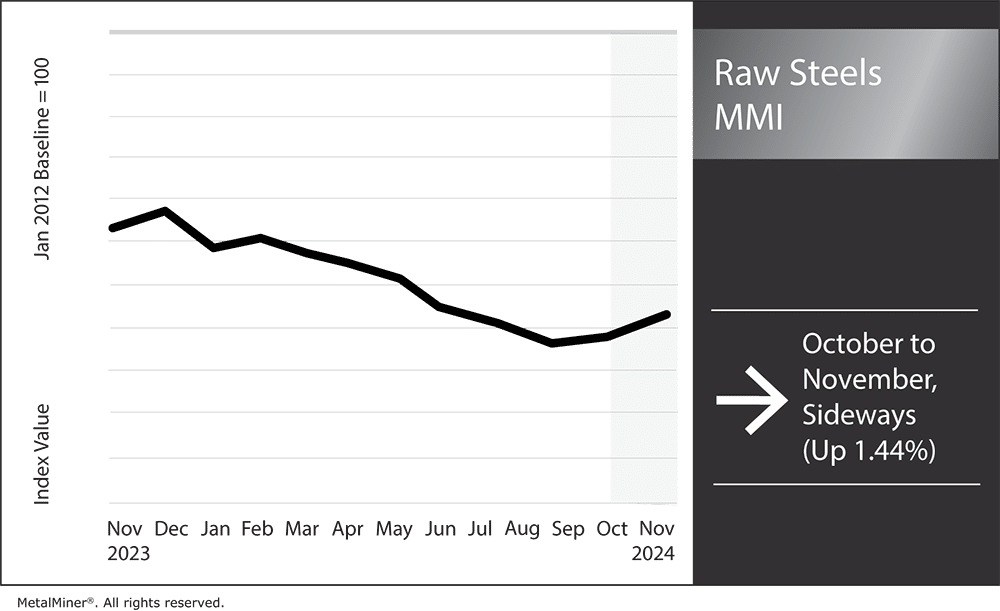

The Raw Steels Monthly Metals Index (MMI) remained sideways with a slight upside bias, showing a modest 1.44% increase from October to November.

U.S. flat rolled steel prices mostly moved sideways during October. HRC prices edged lower, with a 1.29% decline, while CRC prices rose by a mere 0.95%. HDG prices skipped the sideways trend as prices remained in search of a new bottom, falling 3.78% from the September close.

Cut steel expenses without compromising quality using the Monthly Metals Outlook report. Start with a free sample report snippet and subscribe for ongoing savings.

Q3 Witnessed Steel Demand Slowdown

Q3 proved challenging for steel suppliers, with most witnessing significant shipment slowdowns. Steel shipments during the third quarter across the four largest U.S. mills, Nucor, Cleveland-Cliffs, Steel Dynamics (SDI) and U.S. Steel, fell 3.13% year over year, reflecting a 2.37% drop from Q2.

According to the company’s financial results, SDI was the only mill able to increase shipments from Q3 2023, with a 1.05% rise. However, shipments were still down 0.69% from the previous quarter. The company noted, “Underlying steel demand continued to be stable in the third quarter.” The three other U.S. mills saw demand declines, with U.S. Steel, Cliffs and Nucor experiencing respective 7.03%, 6.57% and 0.47% year-over-year drops.

In its most recent financial results, Cliffs attributed weak demand to the “negative impact of two of our top four automotive clients who continue to underperform their own expectations. Due to our high exposure to the automotive sector, Cliffs was more affected than our competitors.” This ultimately forced the mill to temporarily idle its Cleveland #6 blast furnace.

Suppliers Pinched by Falling Steel Prices

Although a slowdown in shipments does not necessarily translate into lower steel prices, it certainly proved to be the case in Q3, as the average selling price for steel declined considerably across all four mills. Nucor saw the largest price decline from Q2, with a 7.99% drop. Meanwhile, Cliffs, SDI and U.S. saw their average steel prices fall by 7.11%, 6.94% and 5.52%, respectively.

Lower selling prices ultimately dragged earnings from the mills. Nucor noted, “The largest driver for the decrease in earnings in the third quarter of 2024 as compared to the second quarter of 2024 is the decreased earnings of the steel mills segment, due primarily to lower average selling prices.”

Despite witnessing a modest year-over-year increase in shipments, SDI reported “earnings declined sequentially, based on lower average realized steel pricing, primarily within the flat rolled operations as generally 80% of this business is contractually based and tied to lagging pricing indices.”

Meanwhile, the declines also extended beyond mills. Leading distributor Ryerson highlighted the bearish climate in its most recent results, noting, “Gross margins continued to be under pressure in the quarter as demand conditions saw continuing contraction and selling price declines continued to outpace the decline in our average inventory costs.”

While Ryerson saw Q3 outperform the previous year with regards to shipments, falling prices appeared to force the supplier to make deals in order to stem the declining value of its inventory.

Get all the latest news on shifts in steel prices and other valuable commodity news. Sign up for the free weekl MetalMiner newsletter here.

Mills Expect Steel Price Rebound in 2025

By Q4, mills had primarily managed to stabilize prices, aided by strategically timed maintenance outages. While there are few signs of a recovery in demand, steelmakers appeared hopeful that 2025 would see conditions rebound.

Cliffs stated, “We expect steel demand to rebound in early 2025, supported by a number of economic and political factors.” The comments fell in line with sentiments from SDI, which expects prices to recover, stating, “Based on domestic steel demand fundamentals, we are constructive regarding the outlook for 2025 metal market dynamics.“

Realistically, 2025 will likely witness a mix of drivers for the steel market. Mills will conclude the remainder of maintenance outages, which could see output begin to recover during the remainder of the year. This will likely challenge mill efforts to stabilize prices, especially as mill lead times appeared to shorten last month.

Don’t get caught off guard by rapid steel market fluctuations. Stay ahead of the curve with MetalMiner Insights and make the right purchasing choices at the right time. Learn more.

Demand Support and Potential Protectionist Measures

Oppositely, the combined effect of lower interest rates, public spending from the Bipartisan Infrastructure Law and the Inflation Reduction Act will offer support to demand. While the Trump administration could unravel certain aspects of the Inflation Reduction Act, like subsidies, the government has already allocated the bulk of Federal spending.

Meanwhile, trade barriers are expected to help insulate the domestic market from competitively priced imports. This includes both the barriers already announced to date and potential upcoming ones. The coated steel market, in particular, faced a number of challenges throughout 2024 due to an influx of imports from countries like Vietnam.

This saw HDG prices drop below both plate and CRC prices during November and triggered several producers to file a trade case. While the world still faces a considerable steel overhang driven by overcapacity in China, protectionist efforts appear more likely to increase than decrease in 2025.

Biggest Moves for Raw Material and Steel Prices

- Chinese HRC prices appeared bullish, with a 9.92% rise to $463 per metric ton as of November 1.

- U.S. shredded steel scrap prices increased 3.76% to $366 per short ton.

- Meanwhile, Comex HRC three month futures fell 4.55% to $755 per short ton.

- Chinese coking coal prices dropped 8.78% to $194 per metric ton.

- Standard Korean steel prices witnessed the largest decline of the overall index, with a 10.22% decrease to $181 per metric ton.

MetalMiner should-cost models: Give your organization levers to pull for more price transparency, from service centers, producers and part suppliers. Explore the models now.