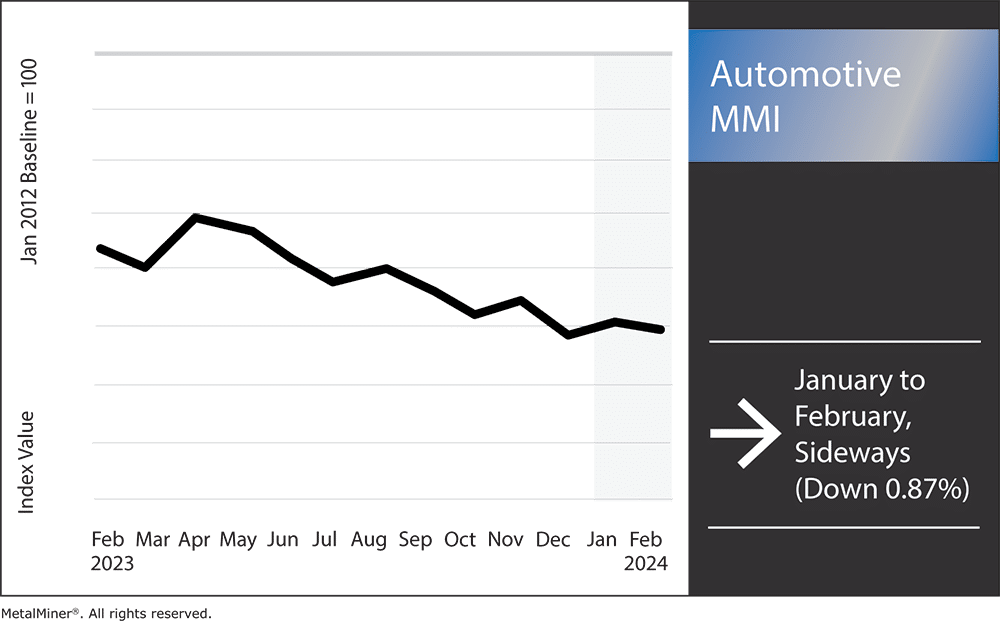

All components of the Automotive MMI moved sideways or down month-on-month. Moreover, January saw prices flatten out across the steel market, causing hot-dipped galvanized steel prices to trend close to support zones. Meanwhile, China’s wavering economy continues to prove a concern for global markets because the country is such a large steel demand driver. Many fear that if HDG demand were to drop too much within China, it could impact global demand overall. Therefore, HDG buyers for vehicle manufacturers should to keep a close eye on China’s economy for the foreseeable future.

Overall, the Automotive MMI (Monthly Metals Index) moved sideways, dropping by 0.87%

Subscribe to MetalMiner’s free weekly newsletter and MMI report to keep up with steel market trends and trends for 9 other metal industries on a monthly basis here.

EV Push: Too Fast?

A recent Automotive News article touched on President Biden’s approach to advancing electric vehicles and whether or not the plan was pushing the industry forward too quickly. The article addresses numerous concerns involving EVs, such as lower-than-anticipated consumer demand, lack of infrastructure to charge vehicles on the go, and EVs remaining unsold on dealer lots. The Biden Administration implemented its EV plan in April of 2023, establishing consumer tax credits for purchasing electric vehicles. However, the U.S. has yet to see a significant rise in consumer EV sales.

Overall, EV sales projections for 2023 met the actual number of EV vehicles sold. However, while last year’s projections met expectations, individual manufacturers and deals still want to lower EV production due to lower-than-anticipated sales.

Ford and GM Adjusting Electric Vehicle Outputs, Potentially Impacting Steel Market

Several large vehicle producers, both domestically and globally, recently chose to adjust EV output levels. According to a statement from General Motors (GM), the company plans to delay the production of several electric vehicle models, providing several different reasons why. Although the company’s Q3 earnings surpassed forecasts, the EV industry continues to prove more difficult than expected. The statement says that the goal of the delay is to improve the vehicles’ efficiency and lower production costs, which will increase future profits. For now, the high cost of vehicle production and end-user purchases continues to plague the EV industry.

Meanwhile, Ford also modified its plans to produce electric vehicles due to lower-than-expected sales. For instance, Ford recently halved its projected output of electric F-150s because demand hasn’t proved as strong as anticipated. While the scale-back doesn’t necessarily reflect the outlook for EV sales in 2024, it does shed light on issues the industry still faces, namely high expenses. Moreover, such cutbacks could have wider implications for the broader steel market.

To prepare your steel purchasing departments for any shifts the automotive industry may cause on global steel demand, read The 5 Biggest Cost-Saving Sourcing Tactics.

Will Higher Labor Costs Impact Detroit’s Big 3?

The three major automakers in Detroit will likely see increased labor expenses resulting from the new UAW contracts. Analysts predict that each company’s annual labor expenses could surpass $1 billion due to these increased costs. Meanwhile, General Motors anticipates an average cost rise of $500 per car in 2024, while Ford forecasts that the new deal will boost labor expenses by $850 to $900 per vehicle.

It seems hard to predict what impact these higher labor costs will have on the overall U.S. automotive market in 2024. One significant worry is that the manufacturers would try to offset these cost increases by charging consumers more for vehicles. However, if the affordability of cars sees an impact from the anticipated price increases, it could restrict the long-term equilibrium level of sales and manufacturing.

The increased labor expenses could also impact the competitiveness of Detroit’s Big 3 in the U.S. market. Furthermore, certain analysts in the sector remain concerned that the corporations’ heightened expenses will potentially harm them in the race for market share, particularly given the intensifying competition from rival manufacturers.

Automotive MMI: Notable Price Shifts

Don’t settle for stagnant steel savings. MetalMiner’s custom price forecasting unlocks the true potential of your volume commitments, ensuring you maximize profit. View our full metal catalog.

- Chinese lead prices moved sideways, rising by 2.84%. This brought prices to $2,249.73 per metric ton.

- Hot-dipped galvanized steel moved within a tight sideways range. Prices only declined by 0.36%, leaving them at $1,385 per short ton.

- Finally, Korean aluminum 5052 coil premium over 1050 traded flat, remaining at $3.92 per kilogram.