Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

How many ways to resist electrification are there? How many cognitive biases get in the way? I’ve found a lot of them, but recently I discovered another. Ports are in the business of handling big honking masses of gases, liquids and solids, and so are predisposed to think that there are going to be lots of energy carrying molecules in their ports to be used by port vehicles.

How do I know this? In recent months I’ve had a couple of great conversations with Sahar Rashidbeigi. She is the global head of decarbonization for A.P. Moller Maersk’s APM Terminals division. APM has the concessions for about 70 of the roughly 800 ports globally that handle over US$8 trillion of containers annually. Maersk is a globally integrated logistics company that has a core in container shipping, but divisions like APM that handle container logistics off of the deep blue sea as well.

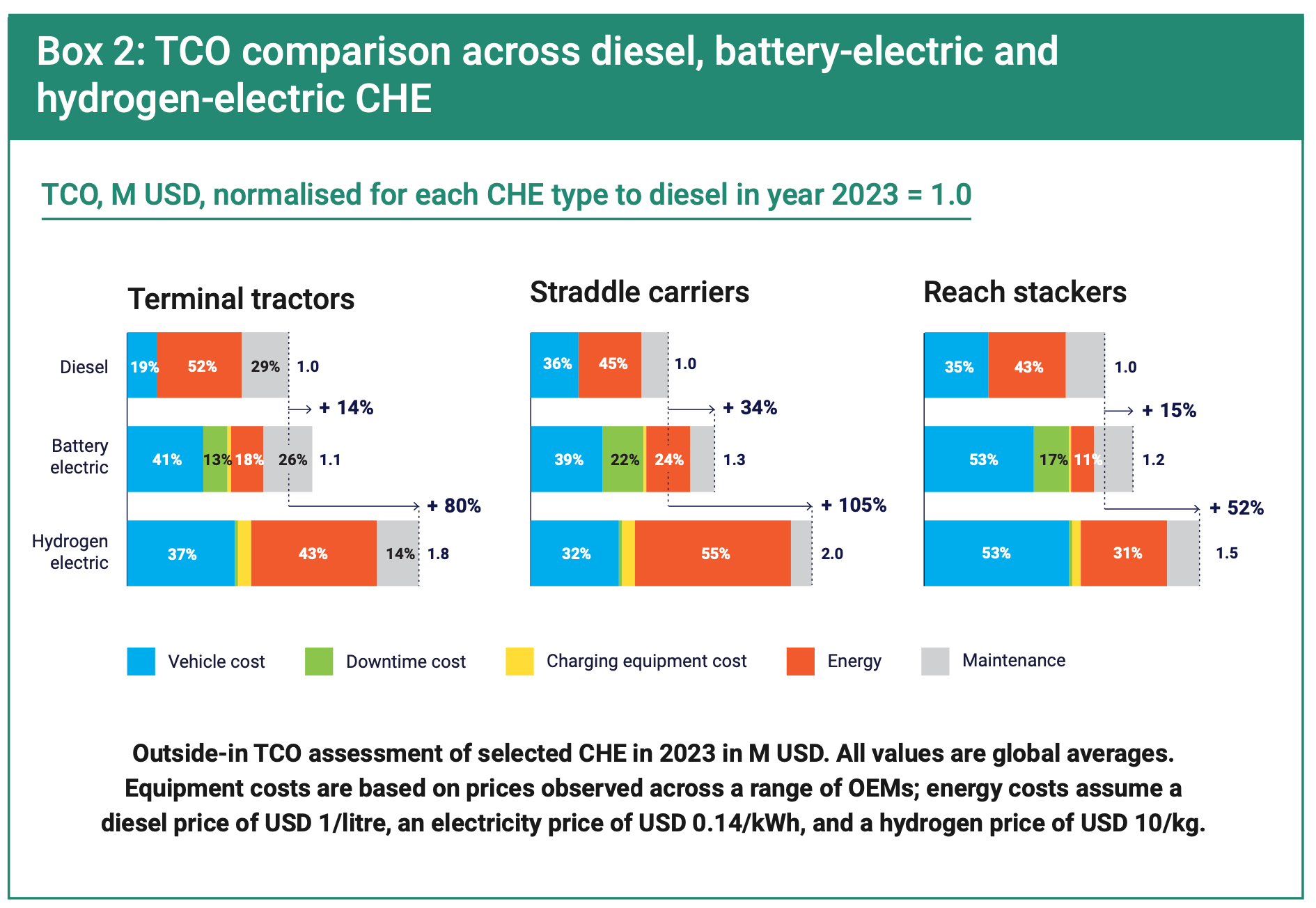

Rashidbeigi and her team recently dropped a report, Reaching a tipping point in Battery-Electric Container Handling Equipment, where yet again a total cost of ownership comparison had been forced upon them, and which yet again found the bleedingly obvious, that the total cost of ownership (TCO) for hydrogen powered vehicles was a lot higher than for battery electric vehicles.

Rashidbeigi engaged Auke Hoekstra, Program Director NEON research at Eindhoven University of Technology, and his team to build the TCO model. Hoekstra founded the 35 PhD research group to light the way to zero emission energy and mobility. I’m sure that there’s something he and I disagree about after running the numbers, but I haven’t found it yet. He and his team do rock solid work.

When Rashidbeigi joined APM after stints with McKinsey, Schlumberger, an investment fund and with a civil engineering degree from Iran and an MBA from Harvard, she thought she was taking an implementation job. From the outside, the domain is obviously one where direct and battery electrification is the clearly obvious solution, just as it is in every other form of ground transportation.

The cranes and overhead gantries were already heavily electrified, plugged into the grids and the gantries that were still running on diesel would be tied to the grid too. The various ground vehicles — flatbed trucks with containers dropped onto them, straddle carriers that rolled over containers to pick them up from above and reach stackers that are like upside down fork lifts grabbing carriers from the top instead of sliding prongs under them from the bottom — were all in the sweet spot for electrification. As a civil engineer, Rashibeigi looked at top speeds of 50 kilometers per hour, short distances, flat and fully paved surfaces and the requirement for high-torque and like everyone else leapt to the conclusion that battery electric vehicles would be the only real solution worth considering.

And yet, two years into her role, she’s released a report where the first six pages are spent outlining the bleedingly obvious again, with more time and money wasted redoing TCO studies that have been done to death. She had her team had to write a hydrogen FAQ and a set of hydrogen questions for the executives and teams who ran APM ports globally, enabling them to fend off the droves of people pushing for hydrogen or derivative fuels with straightforward questions about long-term scaled costs without subsidies.

What caused this? One of the reasons Rashidbeigi and I know each other is because she reached out to me early this year to ask what was driving this clearly odd behavior around hydrogen for energy and transportation. She’s STEM and business cases literate from education and career, so it’s obvious without much difficulty at all to see that hydrogen just isn’t effective, efficient or cheaper than more directly electrifying, and she was baffled at the insistence of so many that it had to be considered.

As I said to her, there were several overlapping groups that shared common motivations that deeply biased their thinking. The fossil fuel industry is the geological hydrocarbon industry, and that hydro is hydrogen. They clearly know that hydrogen for energy is an economic nightmare, with green hydrogen requiring far more renewable electricity than we have in the world today. Further, they knew that blue hydrogen would get lots of governmental money to capture the CO2 and put it back underground, furthering fossil fuel subsidies. They knew that blue hydrogen would likely always be cheaper, even if much less environmentally friendly, than green hydrogen, and so the only source of hydrogen for energy would be blue hydrogen. They also know that with hydrocarbons, splitting off the carbon will not only cost money, but eliminate a lot of the energy in the fossil fuel. In the case of methane, 45% of the energy comes from the carbon in it. Blue hydrogen is a lose lose proposition for energy for everybody except the fossil fuel industry. for them it’s a win-win.

As Michael Liebreich says, they can’t lose by pushing hydrogen for energy. Either they delay real decarbonization by another decade, and they are succeeding well in that. Or they get governments to give them a lot of money to build and operate carbon sequestration technologies on top of hydrogen manufacturing facilities. Without blue hydrogen being a major source of energy, the value of fossil fuel firm’s reserves plummets. That cliff is coming.

Enter the bankers. The firms heavily into providing loans and equity for the fossil fuel industry are typically populated by STEM-illiterate finance types. Nothing wrong with that, but they depend on the fossil fuel firms for STEM literacy and what will work. And they really don’t want to believe that the fossil fuel firms’ finances are on quicksand because if they are, the banks go down with them, or at least the specific bankers they work with. They are highly motivated to believe the story the fossil fuel industry is pitching.

Similarly, governments with high fossil fuel royalties like Norway, Canada, Australia and the USA are easy pickings for the fossil fuel industry’s story. They don’t want the direct and indirect GDP contributions to go away. They don’t want all of the fossil fuel workers to be out of work. They don’t want the people who feed, clothe and entertain the fossil fuel workers to run short of customers. And politicians are frequently many great things, but STEM literacy is nowhere in the requirement set. Leaders like Angela Merkel with her PhD in quantum chemistry are radical outliers, not the norm.

Then there are the industries which depend on using fossil fuels, most notably the ones that build and sell internal combustion engines of various descriptions. If hydrogen or synthetic fuels derived from hydrogen aren’t dominant winners in the decarbonization sweepstakes, their intellectual capital is worthless. I’ve dealt with people from Daimler, MAN, Bosch and Wärtsilä now who are all struggling to push the hydrogen rope uphill because otherwise their careers, their companies and probably their retirement are at risk.

But after speaking with her again recently, I have to add another group to my list of motivated thinkers: port organizations and the people in them. As she shared with me, the assumption she dealt with again and again was that there would be huge tonnages of decarbonized energy-carrying liquids and gases — green or blue hydrogen, ammonia, methanol or something else — flowing through and stored in ports, so why not use a fraction of them to power port equipment?

I’ve dealt with a couple of major shipping concerns with large bulk shipping divisions. They are not expecting massive volumes of replacements for coal, oil and natural gas to magically appear, although they are undoubtedly hopeful. Instead, they are trying to figure out what they are going to do in the coming years. One engaged me to assist them with strategic options for 2030. As I noted earlier this year, only one new very large crude carrier is on order in 2023. The shipping industry has figured out that big volumes of bulk molecules are going away.

But port people apparently aren’t as aware of this. Given the sheer volume of hype related to hydrogen and the reactive sheer volume of hydrogen TCOs that make it clear it isn’t economically viable, it’s pretty easy to have confirmation bias overwhelm the cognitive dissonance of reports like APM’s.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

CleanTechnica Holiday Wish Book

Our Latest EVObsession Video

I don’t like paywalls. You don’t like paywalls. Who likes paywalls? Here at CleanTechnica, we implemented a limited paywall for a while, but it always felt wrong — and it was always tough to decide what we should put behind there. In theory, your most exclusive and best content goes behind a paywall. But then fewer people read it!! So, we’ve decided to completely nix paywalls here at CleanTechnica. But…

Thank you!

CleanTechnica uses affiliate links. See our policy here.