Australian Mining examines how mining companies can adapt to legislative changes in emission-reduction requirements and reporting on climate risks.

Mining companies will benefit from being well prepared for changes to two key pieces of Australian government legislation that will affect their response to decarbonisation and its reporting.

According to SRK Consulting senior consultant ESG Ludovic Rollin, recent reforms to the Safeguard Mechanism and mandatory climate-related financial disclosures will add complexity to environmental compliance and reporting requirements.

“These are very important changes,” he told Australian Mining. “There will be more pressure on mining companies to accelerate their progress in reducing greenhouse gas emissions, and to report on how they are managing climate change risks.”

Rollin’s colleague, SRK Consulting principal consultant ESG Kate Vershinina, said smaller mining companies, in particular, could struggle with the reforms.

“Large mining companies with internal ESG resources have capacity to respond to the changes,” she said. “Smaller firms might not recognise the impact of the changes, how quickly the new requirements will be upon them, and what will be required of them.”

Mining suppliers are also affected by the changes, particularly through mandatory climate-related financial disclosure reforms.

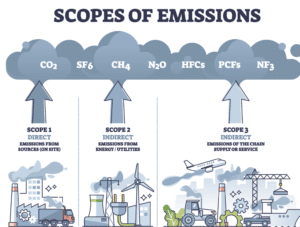

“Mining companies will increasingly require more information from their suppliers on their greenhouse gas emissions as part of Scope 3 reporting requirements,” Vershinina said.

Scope 3 refers to indirect emissions that occur as part of a company’s value chain.

Safeguard Mechanism

The first reform relates to the Safeguard Mechanism, which applies to facilities that emit more than 100,000 tonnes of carbon dioxide equivalent in a year. There were 219 such facilities in Australia in the 2022–23 financial year (FY23).

Put in place in 2016, the Safeguard Mechanism sets legislative targets, known as baselines, on the net greenhouse gas emissions from defined facilities. The legislative framework for the Safeguard Mechanism is set out in the National Greenhouse and Energy Reporting Act 2007 (the NGER Act).

In March 2023, the Australian Government secured parliamentary support to amend the Safeguard Mechanism.

The Bill, which officially commenced on July 1 2023, mandated that Australia’s largest industrial facilities reduce emissions in line with national targets – and from a baseline – by 4.9 per cent each year to 2030.

If a safeguard facility exceeds its baseline, it must manage excess emissions through on-site abatement or by purchasing Australian carbon credit units (ACCUs). Facilities that don’t exceed their baseline may be eligible to earn, trade or store Safeguard Mechanism credits (SMCs), which are awarded to facilities that surpass their reduction targets.

The Bill also introduced a carbon emission ‘trigger’, which requires the Climate Change Minister to assess new or expanded projects that meet the Safeguard Mechanism threshold against the targets. Mining companies will have to account for their potential emissions during the project approval process.

Image: chayanuphol/shutterstock.com

Rollin said this change has ramifications for mine planning.

“Companies seeking government approval for new mines, or to expand existing ones, will need to understand how their facility achieves the baseline target,” he said. “They’ll need to incorporate data from emission-reduction modelling into their mine planning and approval processes. This could add significant new costs.”

Some mining companies may need additional studies to justify their emission-reduction targets.

“There is a risk of greenwashing if companies disclose emission-reduction targets for new projects that cannot be achieved,” Rollin said.

The Bill provides some flexibility through ‘disclosure buffers’ for emission-reduction targets. Companies can choose different mechanisms to reduce emissions (on-site abatement, ACCUs or SMCs) and choose to manage their reductions in a way that best meets their operational needs.

Also included in the Bill are transparency and accountability measures requiring companies that rely heavily on carbon offsets (more than 30 per cent of their baseline) to disclose why they have not made more on-site progress with emission reduction.

“Mining companies will need to think through any potential ramifications of this disclosure, particularly if they have not achieved their baseline target,” Rollin said.

Mandatory climate-related financial disclosures

Introduced to Parliament in March 2024, this legislation aims to enforce climate-related financial disclosures for companies that prepare annual reports under the Corporations Act 2001 or have emission reporting obligations under the NGER Act.

The Bill is designed to provide investors with greater transparency and more comparable information about an organisation’s climate change risks and opportunities, and their strategy to address them.

“Mining companies will have to disclose information to the market about environmental risks that they have not disclosed previously,” Rollin said. “Again, they’ll need to gather data to assess climate change threats and opportunities, and develop an action plan aligned with their governance strategy.”

Vershinina said increases in extreme weather events add complexity to climate-related disclosures.

Image: VectorMine/shutterstock.com

“For example, a mining project will estimate the probability of flooding based on existing parameters and use this probability in the mine design,” she said. “A climate change risk assessment might demonstrate that the parameters have to be re-estimated due to the elevated risk of flooding from extreme weather, and this may require changes to the mine design.

We’ve also worked with mining companies that have reviewed their operational mining plans to account for a higher probability of extreme weather which affects the operational mine schedule.”

This legislation breaks entities into three groups based on their size, emissions and reporting obligations: group 1 (larger companies) must report these disclosures from January 1 2025; group 2 entities (mid-sized companies) start reporting from July 1 2026; group 3 entities (small companies) begin reporting a year after group 2.

“This change is not far away for large mining companies and will be upon smaller mining companies in a little over two years,” Rollin said.

“It’s vital that mining companies prepare now for these legislative changes, particularly if additional studies and data are required to support their emission-reduction targets and climate-related disclosures and strategy.”

Tips for responding to climate resilience reforms

Prepare early and move quickly

For some mining companies, adapting to the two reforms may involve months of work. Start working on understanding your risks early, and note that these reforms are part of a larger package of expected reforms relating to decarbonisation this decade, including the ongoing JORC Code update and the Commonwealth Environment Protection and Biodiversity Conservation Act 1999 reform (Nature Positive law).

Risk assessment and gap analysis

Assess the reforms’ impact on your organisation and its internal resources to respond, particularly in areas such as ESG and financial reporting. Assess risks related to climate change and the additional regulatory requirements, and whether additional studies are required to provide data to support reduction targets or the disclosure of climate-related threats and opportunities to stakeholders.

Strategy and action plan

Develop your company’s strategy – aligned with your governance strategy – to address climate-related threats and opportunities, and support this with an action plan to demonstrate a pathway to achieve strategic aims.

Resources

Review your company’s internal resources to implement the strategy and action plan. Consider budget implications and identify what external resources might be required and ensure your organisation has access to expert advisers to assist on studies that provide data to support disclosures.

Say no to greenwashing

The difference of the reforms is the transition from reporting on good-looking assumed initiatives to the actual implementation of specific actions and the requirement to prove that declared targets will be achieved. Implement your plans and be ready to report on and disclose the required targets and the work done.

SRK Consulting is a leading independent international consultancy that advises clients mainly in the earth and water resource industries. Its mining services range from exploration to closure. SRK experts are leaders in fields such as due diligence, technical studies, mine waste and water management, permitting, and mine rehabilitation. To learn more about SRK Consulting, visit www.srk.com

This feature appeared in the October 2024 issue of Australian Mining.