Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

Geely is Rising

Following up on our latest report on the top selling electric vehicle models in the world, here’s a broader look at the top selling auto brands and auto groups/OEMs.

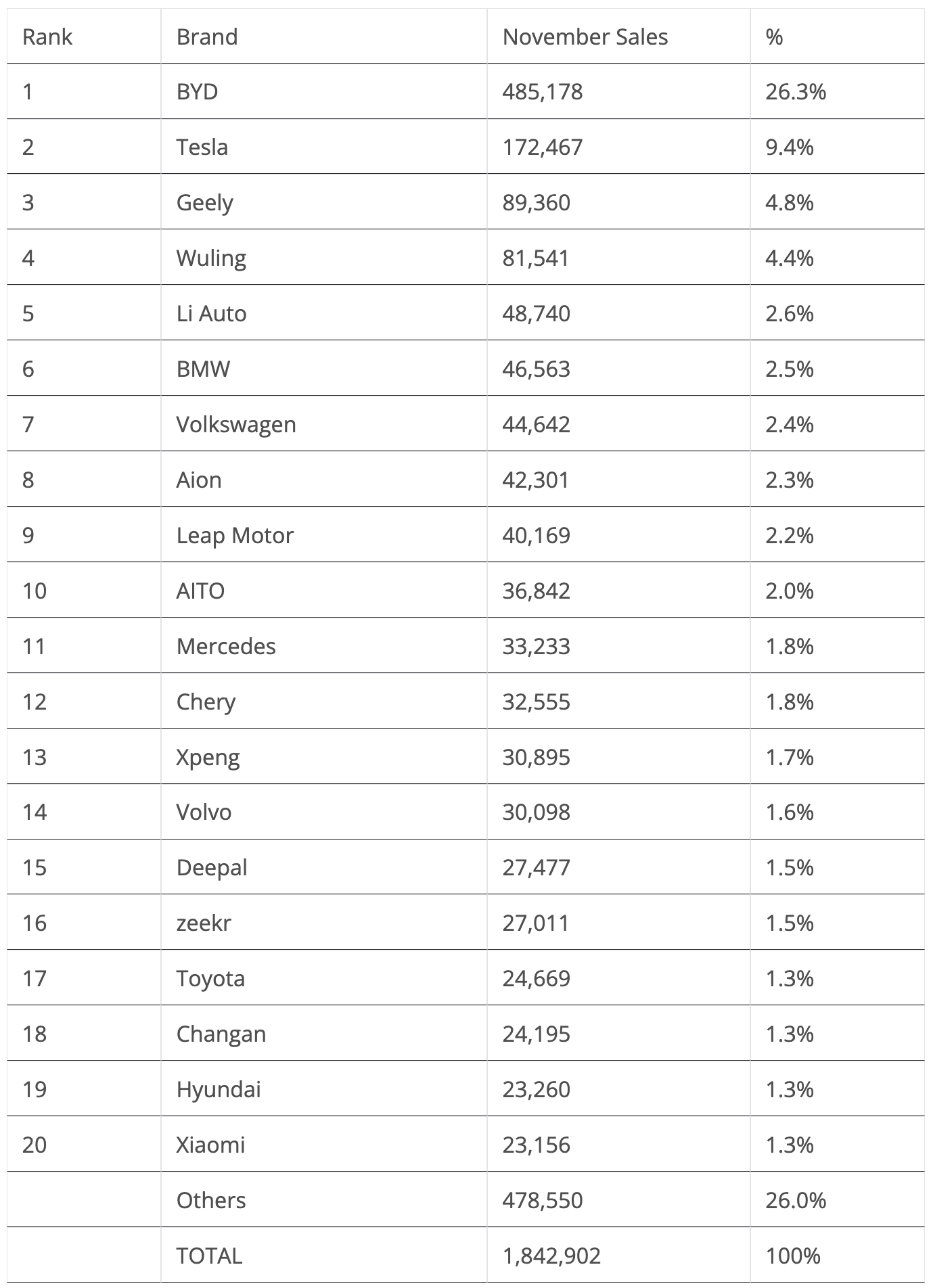

Top Selling Auto Brands

In November, #1 BYD, deep into pricing out the competition (fossil fueled and electric…) didn’t disappoint. It scored some 485,000 registrations, which is, of course, a new record. With sales at this level already, one starts to wonder how high the Shenzhen make’s sales could go. Would 800,000 units per month be possible?

Interestingly, only 31,000 were exports. This could be seen in two ways: On one hand, it means that the Shenzhen maker is highly dependent on its domestic market, where it sells over 90% of its production, but on the other, this means that there is plenty of of potential growth still to be fully explored. Large markets like Brazil, Mexico, Australia, and others are surely ready to receive its models with welcoming arms.

As for Tesla, it continues randomly switching between black and red, between growth and dropping sales. In November, sales were down by 1% YoY, after a 6% rise in October. Through the first 11 months of 2024, there have been five growth months (January, May, July, September, and October) and six months in the red (February, March, April, June, August, and November).

Regardless of what happened in 2024, expect 2025 to be a year of growth, with the Model Y refresh and (maybe) a new, cheaper model in the second half of the year — with the question now being: “By how much will Tesla grow?”

Below the top two, we have three Chinese brands, with rising Geely winning the last position on the podium with over 89,000 registrations, another record, followed by #4 Wuling, which got 81,000 registrations, a new record — and still, this wasn’t enough to keep Geely off of the podium.

Because Geely has a number of models ramping up (Galaxy E5, Geome Xingyuan, Panda Mini) or in the pipeline (Galaxy Starship 7), expect it to continue shining in 2025, probably ending the year in 3rd, which would be a first for the Chinese make.

In 5th, we have Li Auto. Despite not hitting a record result, it was still up a solid 20% YoY.

A few positions below, the highlights also came from China, with four brands scoring record results. #9 Leapmotor scored 40,000 registrations, its 4th record performance in a row. #13 Xpeng is also rising fast, with 31,000 registrations in November, its 6th record in a row, mostly thanks to the success of the Mona M03 and P7+ liftbacks. #15 Deepal scored a record 27,477 registrations, with its S7 crossover representing 45% of its sales. #16 Zeekr also had a record, 27,000 registrations, which is based on the success of its 7X midsize crossover.

And in #20, we have Xiaomi. Thanks to a record 23,156 deliveries of its SU7 sedan, it is already showing up on the brand radar — despite having just one model available. Now, imagine where the company will be 12 months from now….

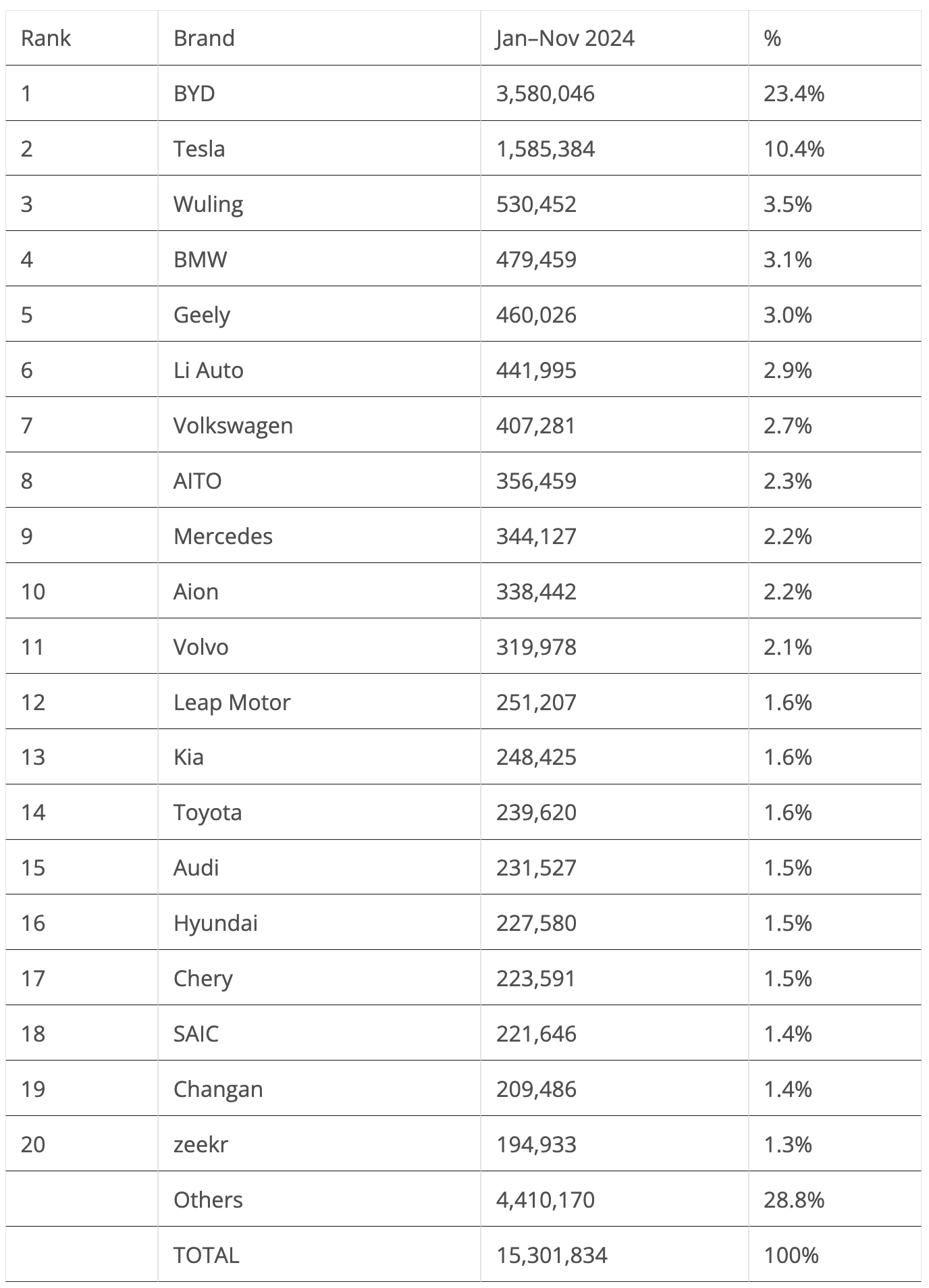

In the YTD table, BYD has double the sales of Tesla, and the US brand has almost three times as many registrations as the third placed brand, Wuling. The Chinese brand now has a 50,000-unit advantage over #4 BMW, so the German can already say auf wiedersehen to the bronze medal it received in 2023. 2024’s bronze is for Wuling. (And 2025’s will be for Geely.)

Speaking of Geely, there was a position change in the 5th position, with Geely surpassing Li Auto. With BMW just 19,000 units ahead of it, will the German brand be the next to be outdone? One thing is for sure: the Taizhou make is fast becoming the 3rd musketeer in the EV race.

In the second half of the table, Leapmotor profited again from a never-ending record streak of performances to continue climbing up the table, jumping two positions to 12th! (At this pace, Leapmotor will soon sell more EVs than the whole of Stellantis….) 😮

Rising Chery was up to #17, and with #16 Hyundai and #15 Audi within target range, it wouldn’t be surprising if the Wuhu-based brand ended 2024 at #15.

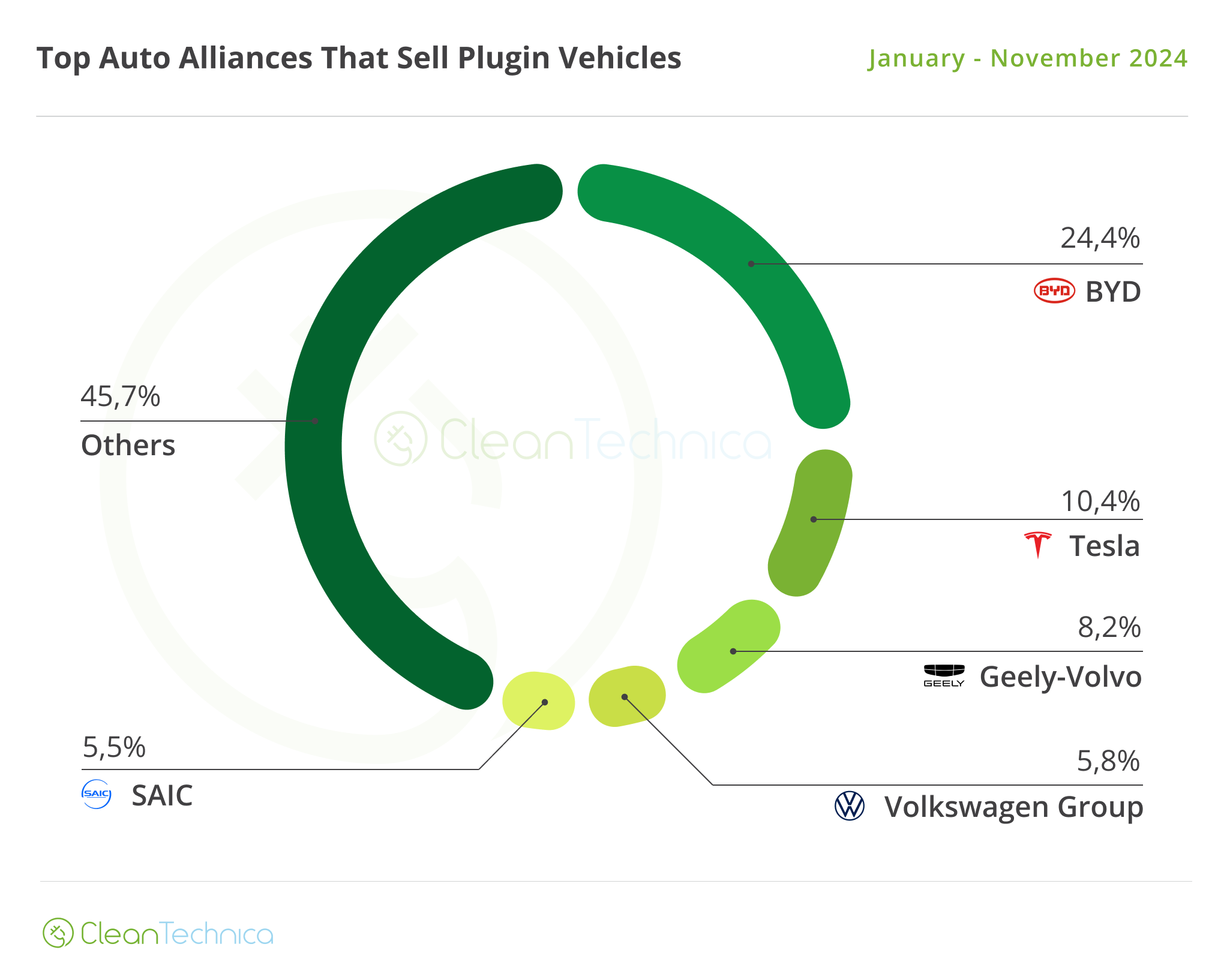

Top Selling Auto Groups

Looking at registrations by OEM, #1 BYD again gained share, thanks to refreshes and new model launches, going from 24% to its current 24.4% (it had 22.1% a year ago). Tesla ended November with 10.4 % share (it had 13.3% in the same period of 2023).

3rd place is in the hands of Geely–Volvo, with the OEM growing by 0.2% to 8.2% share. Along with BYD, Geely is the only other OEM to grow share in the top 10, going from 6.8% in November 2023 to its current 8.2%.

Considering Tesla’s eroding share and Geely’s continued growth, we could see the Chinese juggernaut threaten Tesla’s silver medal and maybe even surpass it in the second half of 2025.

(Even BYD should look over its shoulder, as Geely has the potential to go after it in a few years … say, 2028? 2029?)

Meanwhile, Volkswagen Group stayed in 4th (5.8%) but lost some of its advantage over #5 SAIC (5.5%, up from 5.4%). Thanks to Wuling’s positive output, the Shanghai-based OEM managed to compensate for the slow month from the rest of the lineup.

Below SAIC, #6 Changan (3.8%, up from 3.6% in October) profited from Deepal’s success to increase the distance over #7 BMW Group (3.5%). Further underlining the current sales blues of legacy OEMs, #8 Hyundai–Kia was down by 0.1% (in this case to 3.2%), while Stellantis was down (again) by 0.1% (to 2.9%), being surpassed by the Chinese startup Li Auto (2.9%). The multinational conglomerate is now #10 in the OEM ranking.

A worrying sign of the Stellantis performance is that in 12 months it has lost almost a third of the EV share it had a year ago….

It feels like one should say it’s not EV sales that are down, it’s legacy EV sales that are falling….

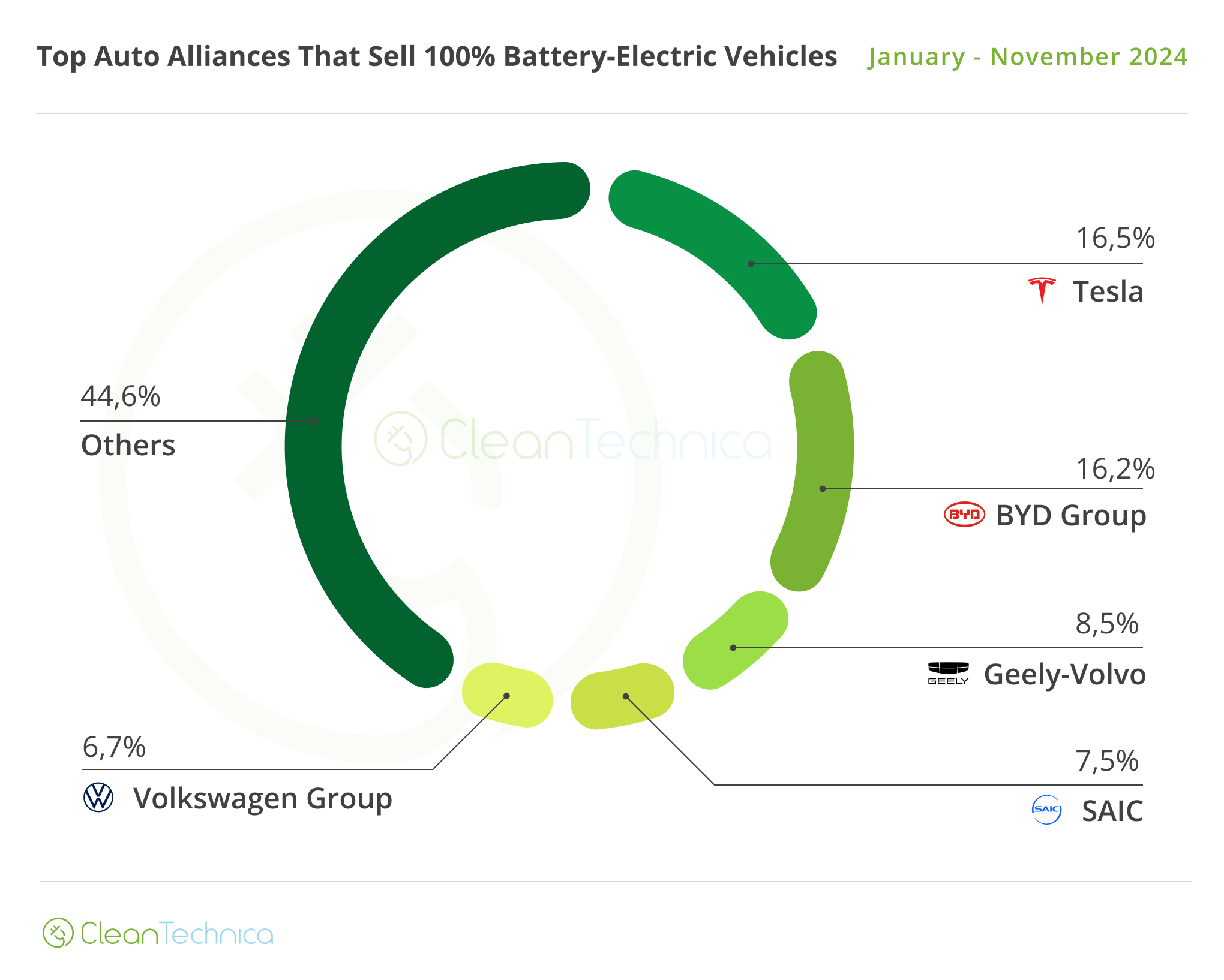

Looking just at BEVs, Tesla remained in the lead with 16.5% share, but it has lost 2.7% share compared to the same period last year. In second is BYD (16.2%, up from 16.1% in October).

Despite narrowly keeping the title in 2024, with Tesla continuously losing share, we should see BYD surpass it in the first half of 2025.

Geely–Volvo (8.5%, up from 8.2%) was up strongly thanks to good results across its long lineup of brands. Comparing the OEM’s performance to where it was 12 months ago, the progress is visible, jumping from 6.3% share in November 2023 to its current 8.5%! At this pace, it won’t be surprising to see Geely competing for #1 in a couple of years (say … 2027?), especially considering it’s not as PHEV-heavy as BYD.

SAIC (7.5%, up from 7.4% in October) is also on the rise, much thanks to Wuling, with the Shanghai OEM having a significant advantage over #5 Volkswagen Group (6.7%), which should remain there at the end of the year.

Below the top 5, BMW Group (4%, down from 4.1% in October) is steady in 6th, followed by #7 Hyundai–Kia (3.9%, down 0.1%).

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy

- CleanTechnica")