(Reuters) – Oil prices will struggle for traction this year as global economic headwinds stymie gains that could be fuelled by a rebound in China and OPEC+ cuts, a Reuters poll showed on Friday.

The survey of 37 economists and analysts forecast Brent crude would average $83.03 a barrel in 2023, versus the $84.73 consensus in May.

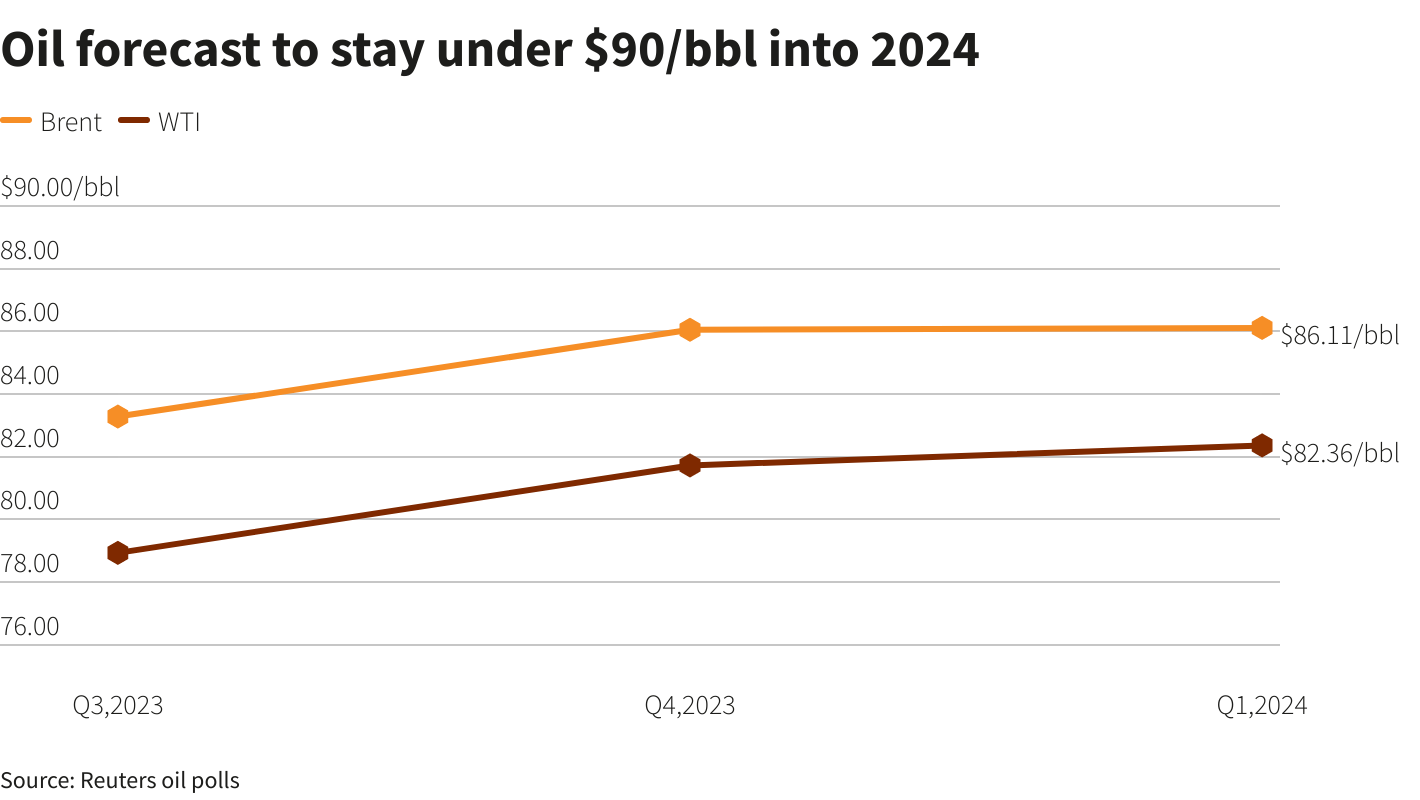

The global benchmark, now trading around $75 a barrel after having shed about 13% thus far in 2023, was seen averaging $83.28 in the third quarter before popping above the $86 mark in the next two quarters.

Forecasts for U.S. crude were also scaled back to $78.38 a barrel in 2023 from last month’s $79.20.

The third quarter will be a “make-or-break quarter ahead as lofty demand growth expectations from OPEC and IEA need to come to fruition to avoid additional downward pressure on prices,” said Ole Hansen, Saxo Bank’s head of commodity strategy.

Goldman Sachs said this week that rising interest rates would remain a “persistent drag” on oil.

But while the rising rates and weaker economic readings from China have weighed on oil markets, some analysts saw prices getting a small fillip from stimulus measures and OPEC+ supply curtailments led by Saudi Arabia.

Earlier this month, the International Energy Agency (IEA) said the OPEC+ output deal sharply increases prospects of higher prices, while Saudi Aramco predicted demand from China and India would offset recession risks in developed countries.

“There’s been little sign of weakness in China’s oil demand even if the general reopening boost has disappointed some investors. China’s refineries produced at record levels over the first five months this year,” said Ian Moore, senior research associate at Bernstein.

“Further growth should come as economic activity continues to expand, albeit at a slower rate.”

Global oil demand is forecast to grow between 1 to 2 million barrels per day (bpd), as per the poll.

Five respondents also predicted a supply deficit in the second half of 2023.

The deficit would come even as Russia’s seaborne oil exports hit a 4-year record in May, Refinitiv Eikon data showed, as Moscow caters to demand from India, China and Turkey.

“Once these deficits become visible in on-land oil inventories, we expect prices to trend higher,” said UBS analyst Giovanni Staunovo.

Respondents also largely agreed that the Organisation of the Petroleum Exporting Countries would take measures to keep the floor for oil prices at $80.

Share This: