By Jake Fuss and Grady Mumro

Summary

- Budget deficits and increasing debt have become serious fiscal challenges facing the federal and many provincial governments recently. Since 2007/08, combined federal and provincial net debt (inflation-adjusted) has nearly doubled from $1.18 trillion to a projected $2.18 trillion in 2023/24.

- Between 2019/20 (the last year before COVID) and 2023/24, the combined federal-provincial debt-to-GDP ratio is expected to grow from 65.7% to 76.2%. Moreover, the federal and provincial governments are on track to have collectively accumulated $425.8 billion (inflation-adjusted) in total net debt between 2019/20 and 2023/24, an increase of 24.3%.

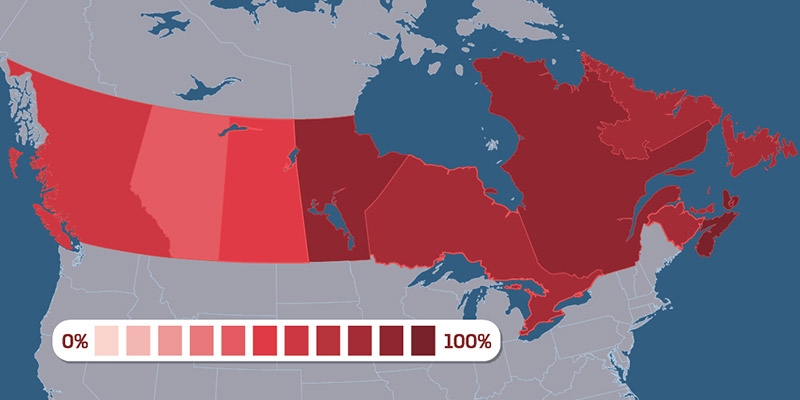

- Among the provinces, Nova Scotia has the highest combined federal-provincial debt-to-GDP ratio (96.8%), while Alberta has the lowest (42.9%). Newfoundland & Labrador has the highest combined debt per person ($67,471), followed by Ontario ($60,609). In contrast, Alberta has the lowest debt per person in the country with $42,293.

- Interest payments are a major consequence of debt accumulation. Governments must make interest payments on their debt similar to households that must pay interest on borrowing related to mortgages, vehicles, or credit card spending. Revenues directed towards interest payments mean that in the future there will be less money available for tax cuts or government programs such as health care, education, and social services.

- The federal and provincial governments must develop long-term plans to meaningfully address the growing debt problem in Canada.

More from this study

Share This: