Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

June’s auto market saw plugin EVs take 28.2% share in the UK, up from 25.1% year on year. BEVs grew volume modestly, while PHEVs grew more strongly. Overall auto volume was 179,263 units, up 1% YoY and well below pre-2020 seasonal norms (~225,000). The UK’s leading battery-electric vehicle brand in June was Tesla.

June’s sales saw plugin EVs take 28.2% share in the UK, with full electrics (BEVs) taking 19.0% and plugin hybrids (PHEVs) taking 9.3%. These are an increase from shares a year ago of 25.1% combined, 17.9% BEV and 7.2% PHEV.

While overall market volume was up just 1.1% YoY, plugins saw higher volume growth. BEV volume increased by a modest 7.4% YoY to 34,034 units. PHEV grew volume more strongly, by 30% YoY, to 16,604 units.

For context, HEVs (plugless) grew in volume by 27% YoY to 26,702 units (with market share of 14.9%). Old-school petrol vehicles (including MHEV variants) still dominate the UK market with 50.9% share, but that’s a new record low, down from 55.8% YoY. These powertrains saw volume falling by 7.8% YoY to 91,277 units — despite the growing overall auto market. Later this year should see them fall below 50% share of the market on a more or less permanent basis.

Diesel (including MHEV variants) was also close to a record low share of 6.0%, from 7.3% YoY. Volume fell 17.2% YoY to just 10,696 units. These are on track to fall under 5% share around the end of this year.

Best Selling Brands

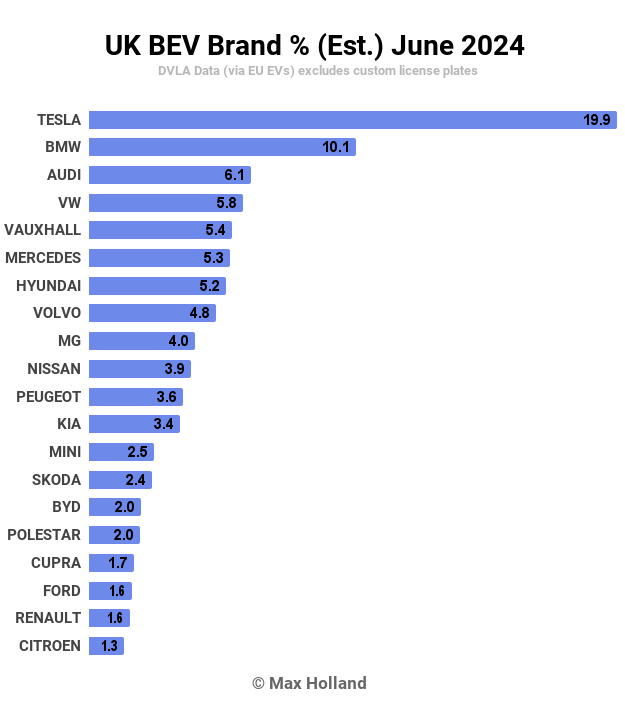

Tesla was back in the lead of the BEV brands in June, with a strong 19.9% share of the BEV market. The runner up was BMW, with 10.1% share, and Audi came third, with 6.1% share.

Tesla’s registrations were fairly evenly split between the Model Y (3,642 units) and the Model 3 (3,111 units). Both were amongst the UK’s overall top ten best selling vehicles (of any powertrain) for June.

BMW’s biggest seller remained the i4, with an estimated ~1,000 registrations, with the iX1 not far behind, and the iX3 (and others) in a supporting role.

Audi’s biggest selling BEV remained the Q4 e-tron, with an estimated ~1,700 registrations in June. The new Q6 e-tron (see the Sweden report for a summary) has not yet debuted in the UK, but should prove popular once it does.

Back in fourth place, Volkswagen brand had a better month than usual (more typically 10th or below), led by the ID.4 with an estimated ~820 registrations and the ID.3.

Other decent selling BEV models in June included the Hyundai Kona, Volvo EX30, and MG4.

Mini’s new BEVs are starting to sell in decent volume, with the brand now rising to 13th place, having been close to 20th in the recent past.

Let’s check in with the 3-month results:

Tesla still has a decent lead. Although, the gap over BMW (now a 2.6% difference) has narrowed compared to Q1 (4.6% difference). The other brands are a long way back, with Audi, Mercedes, and Volvo filling out the top 5 spots.

MG and Kia have stepped back slightly since Q1. Although, this is likely only temporary — bear in mind that the UK is an unusual RHD market, and most brands make shipments in erratic batches.

Toyota fell back 7 spots since Q1, and is now in 17th place (weak considering it is the largest auto brand in the world). Climbing up the ranks is Mini, now in 19th, from 29th previously, thanks to the new BEV model launches.

Outlook

With the auto market being scarcely more than flat YoY, the wider UK economy continues to be weak, with Q1 registering 0.3% GDP growth, from -0.2%, 0.2%, and 0.2% in preceding quarters. Inflation reduced to 2.0% in May (latest data) from 2.3% in April, and interest rates remained high, at 5.25% (now for close to a full year). Manufacturing PMI was 50.9 points in June, slightly down from 51.2 points in May.

The UK’s auto industry association, the SMMT, has said: “Industry calls on the next government to back consumers as fewer than one in five new battery electric cars go to private buyers.” This is code for the reintroduction of purchase subsidies that ultimately go to automakers’ bottom line. Given that there is now a strong stick in place with the new ZEV mandate, and BEV powertrain components continue to fall rapidly in cost, do automakers really need more taxpayer money?

Bear in mind that 4 out of 5 BEVs that go to fleets or businesses are mostly going to leasing companies, and thus anyway get leased mostly to private consumers in the end. It’s just that the fleet buyers’ bulk purchase advantage means less margin for the automakers.

This latest SMMT appeal for more handouts seems to me to be just another sign that most legacy automakers are having to be dragged kicking and screaming into the EV transition.

What do you think about the UK’s auto market, and the transition towards EVs? Please join in the debate in the comments section below.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Videos

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy