Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

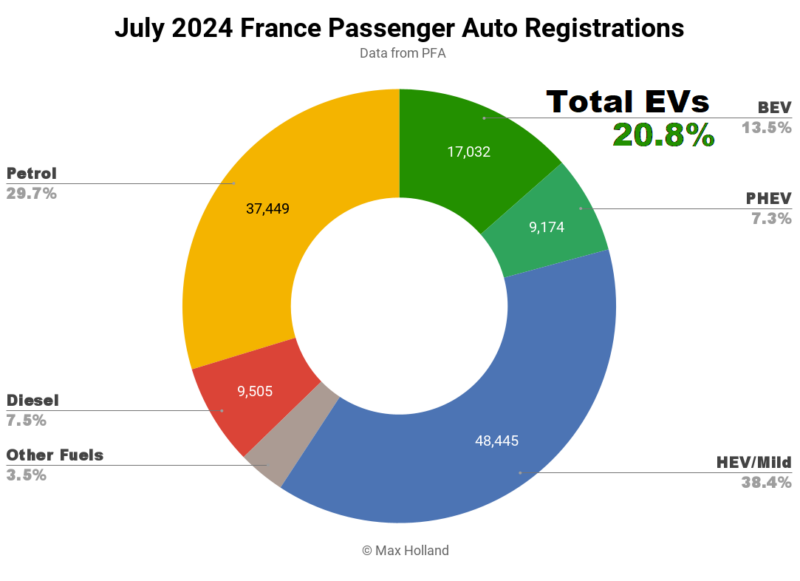

July’s auto sales saw plugin EVs take 20.8% share in France, a drop from 23.3% year-on-year. BEV share was roughly flat YoY, while PHEV share fell. Overall auto volume was 126,037 units, down by some 2% YoY. The Renault Megane took the lead in the BEV rankings.

July’s market tally saw combined plugin EVs take 20.8% share in France, comprising 13.5% full battery-electrics (BEVs), and 7.3% plugin hybrids (PHEVs). These compare with YoY figures of 23.3% combined, with 13.1% BEV, and 10.3% PHEV.

In volume terms, BEVs were essentially flat YoY, growing sales by less than one percent. This was enough to marginally improve BEV market share, given the overall market’s 2% volume shrinkage. PHEV volumes fell 31% YoY to 9,174 units (the lowest volume in almost 2 years), and thus saw a loss in market share.

Some BEV puritans may be tempted to celebrate the decline in PHEV sales, but this is not Norway, a country near the end point of the transition, where the alternative for an avoided PHEV sale is almost always a BEV sale.

In France, the de facto alternative to a PHEV sale is typically either a combustion vehicle or more likely a plugless hybrid (or mild hybrid). Hybrids grew volume by almost 50% YoY to 48,445 units, overtaking combined combustion-only sales for the first time.

Why are France’s BEV sales now lacklustre in terms of YoY progress? European BEVs remain far overpriced compared to where they should be, given the radical cost declines in BEV powertrains. Recall that BEVs in China are now competing on price with ICE vehicles in almost all market segments.

The EU rules have effectively frozen the requirement for auto emissions improvements in 2024 compared to 2023 — and many legacy auto makers are only moving to BEV because they have to, not because they want to lower emissions. Don’t expect them to do more than legally obligated.

The EU rules will only see the next step of tightening in 2025, so we can’t expect EV progress in Europe until then. The biggest European legacy players actually reduced their BEV sales in Q1 2024, over Q1 2023 (see Sweden report). Keeping out affordable EVs made in China, to protect European legacy auto’s record profits (in the short term), is also part of this picture — strong competition is apparently bad for shareholder profits and executive salaries.

Health, climate, and consumer pocket books, are all paying the price for legacy auto’s record profits.

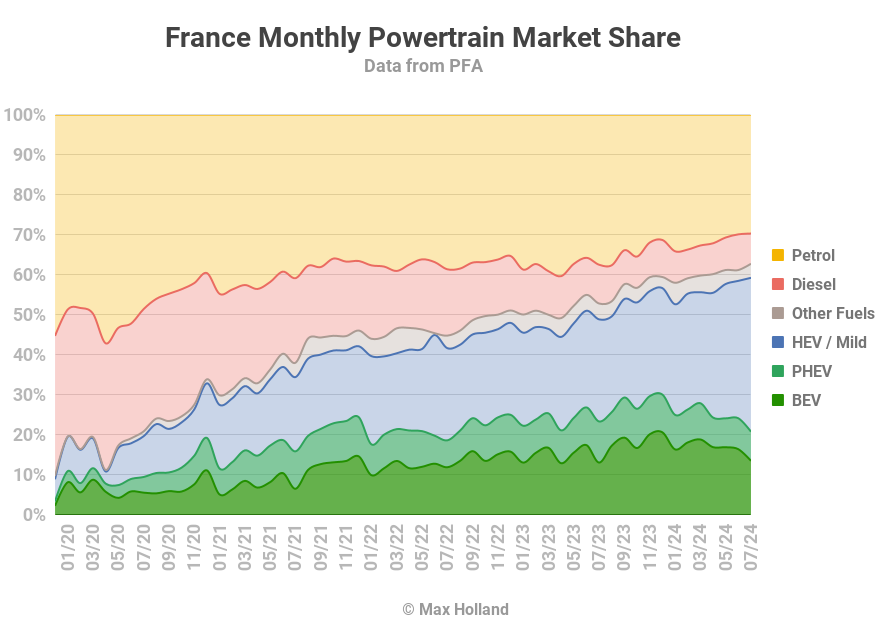

The short term boost to YoY BEV sales in France at the start of the year — which came from the temporary “social leasing” programme — is now firmly in the past. We can expect, at best, a flat BEV YoY market until 2025, unless the Citroen e-C3 has a record-breaking production ramp up, and funnels almost all its output into the French market.

The e-C3 was originally scheduled to launch in Q2, but none have delivered yet (as of early August 2024), with the reason given for the delay — “software issues”. But of course. Now the first delivery timing is guided vaguely as “after the summer break” — does that effectively mean October and onwards? My advice — don’t hold your breath for this promised wave of affordable BEVs from European legacy auto. Most of them remain unashamed foot-draggers on the EVs transition. Decent volume probably won’t appear until well into 2025.

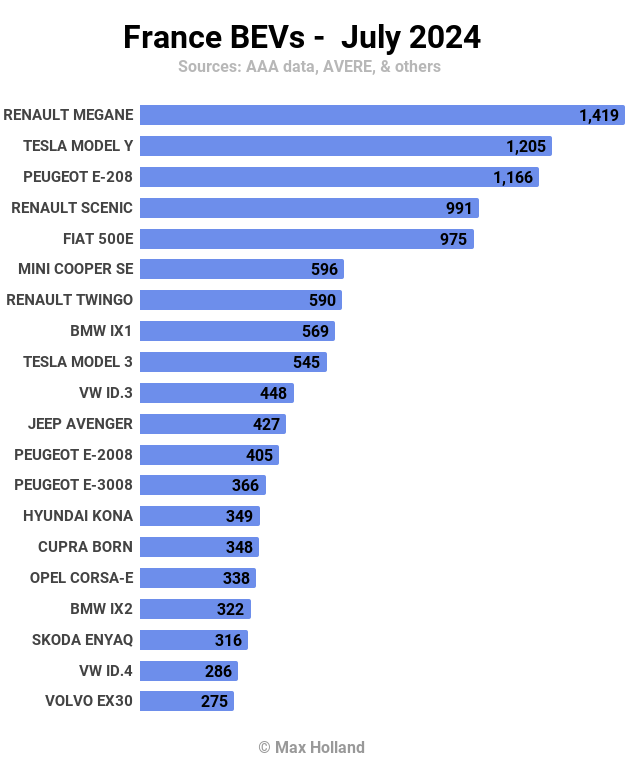

Best Selling BEV Models

The Renault Megane was the best selling BEV — for the second consecutive month — in July, with 1,419 units delivered.

In runner-up spot was the Tesla Model Y, with 1,205 units. The Peugeot e-208 took third, with 1,166 units.

The new Renault Scenic (in 4th) has broken into the top 5 for the first time since its January debut. Let’s see if it can become a regular, or even climb higher.

The only surprise in the top 20 was the BMW iX2, entering for the first time (17th position) after its French debut in February. The surprising aspect is that the iX2 is essentially a slightly lowered and coupe-backed variant of the iX1, which is already a top 10 regular in France.

Both these BMW SUVs are reasonably affordable, given the premium positioning. Both can be had for prices starting from €46,900. The iX1 is more boxy and practical for families, the iX2 is more sporty looking.

One point to note is that — whereas the iX1 MSRP is about 7.5% more expensive than its combustion “X1” variants — the BEV iX2 undercuts its combustion variants (the “X2”), even if only by ~€1,000.

This likely makes many prospective BMW SUV buyers look at the iX2 BEV as relatively “great value”, and helps its sales. The first example of a BEV priced below its ICE siblings that I am aware of in Europe (jump in the comments if you know of others) — though not too surprising to see it in a premium segment. After all, it is much easier and less costly to offer “power and refinement” via an EV powertrain, than via an ICE powertrain.

We don’t have enough data resolution to identify France’s July debutants, but see our other reports to check regional debutants emerging in neighbouring markets.

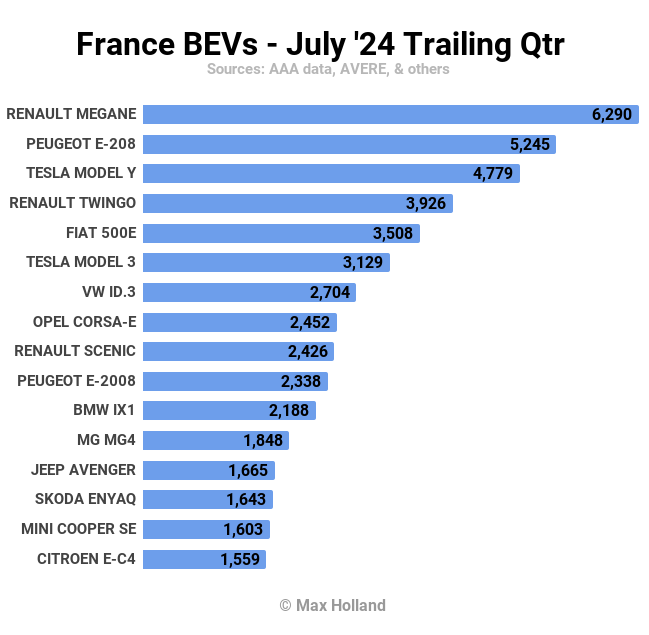

Let’s check in on the trailing 3-month rankings:

There are few big surprises here, except to note that the Renault Megane has climbed steadily over the last few months to now take the top spot. The Peugeot e-208 still has a big lead in the full year race, however.

Note also the rise of the Megane’s younger sibling, the Renault Scenic, now inside the top 10 for the first time, and likely to climb higher.

When the Citroen e-C3 finally does arrive in good volume (again, likely not before 2025), it will shake up this chart a bit. Renault and Volkswagen will have to respond by offering better value on their own small BEVs, which will increase their respective sales volumes. This relative increase will likely push some of the more premium and expensive BEVs (BMW iX1, perhaps the Tesla Model 3) a few steps down the rankings, even if their unit sales remain largely unchanged.

Outlook

France’s BEVs saw healthy YoY growth for the first 4 months of 2024, but have since stagnated for the reasons we discussed above. The overall auto market has also been slightly down YoY for the past 3 months. The broader economy is still above water YoY, but only weakly so, with Q2 2024 GDP up 1.1% YoY, from 1.5% in Q1. This is nevertheless better than the Netherlands, Germany, Denmark, and Sweden, which are all in negative territory as of latest data.

France’s inflation rate remained relatively steady at 2.3% in June (latest), and interest rates are flat at 4.25%. Manufacturing PMI took a downturn in July to 44 points, from 45.4 in June.

The outlook for the BEV transition in France is likely to continue to be uninspiring for the rest of this year. The temporary social leasing programme is now mostly played out, 2024 EU regulations don’t require emissions progress over 2023, and the “affordable” home-grown European BEVs won’t arrive in volume until 2025. In fact, they will arrive just in time for the tighter emissions regulations — not a coincidence.

What are your thoughts on France’s EV transition? Please jump into the discussion below to share your perspective.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Videos

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy