Copper prices today remain trapped in a sideways range. Prices lack enough bearish or bullish momentum to establish a strong trend in either direction. Prices declined during the first weeks of January, falling to their lowest level since November. However, they rebounded in the second half of the month. This brought them a mere 0.52% above where they stood at the close of December.

Overall, the Copper Monthly Metals Index (MMI) moved sideways, with a 0.32% decline from January to February.

Stop obsessing about the actual forecasted copper prices today. It’s more important to spot the trend. See why.

Liquidation of China’s Evergrande Raises Questions About Copper Demand

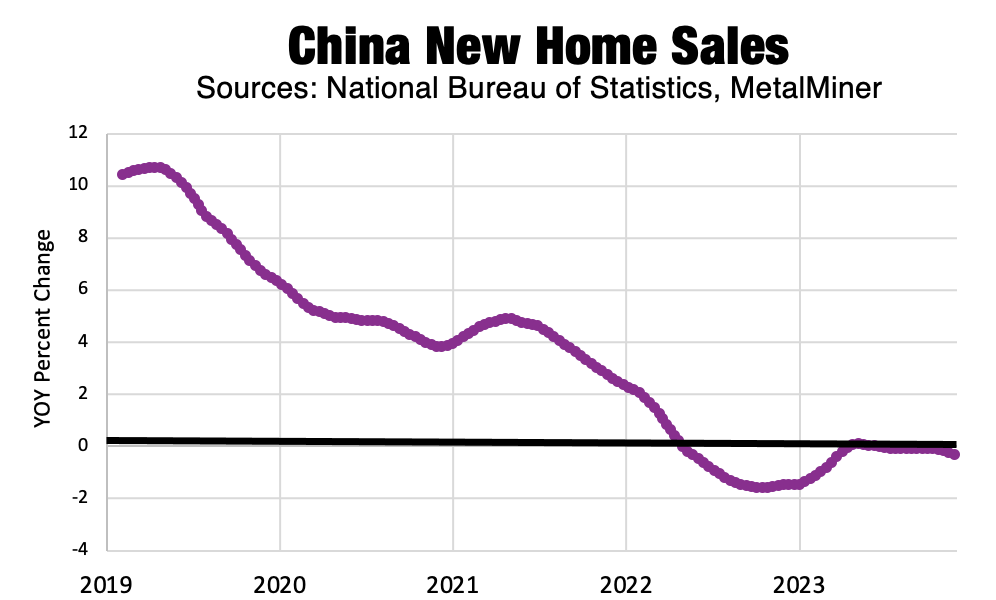

A Hong Kong court recently ordered the liquidation of Chinese property developer Evergrande. The decision comes more than two years after the company first started to miss debt repayments. The risk of reflating the property bubble led to only limited support for the company from Beijing, while new home sales spent most of the last two years in decline. Although declines appeared to moderate throughout 2023, the sector has yet to see a turnaround. Moreover, December saw newly-built home sales drop by 0.4% from December 2022.

The property giant is far from an anomaly within China’s property sector. Numerous other developers have also struggled to make repayments. In most cases, their woes triggered support from local governments attempting to stem a more widespread collapse. However, China’s housing supply already far surpasses its population. While estimates vary, those most extreme projections suggest there are around 3 billion unoccupied homes, more than double its current 1.4 billion total population. Adding in the complication of ongoing population declines in China, the question becomes: who are they building things for?

Can China EVs and Renewables Make Up The Difference?

Even with policy support, the problems with China’s property sector will take years to resolve. Meanwhile, these issues will continue to raise questions about the future growth of China’s economy. Beyond GDP, China’s construction sector historically accounted for an estimated 30% of the country’s total copper consumption, leaving uncertainty about the outlook of global copper demand.

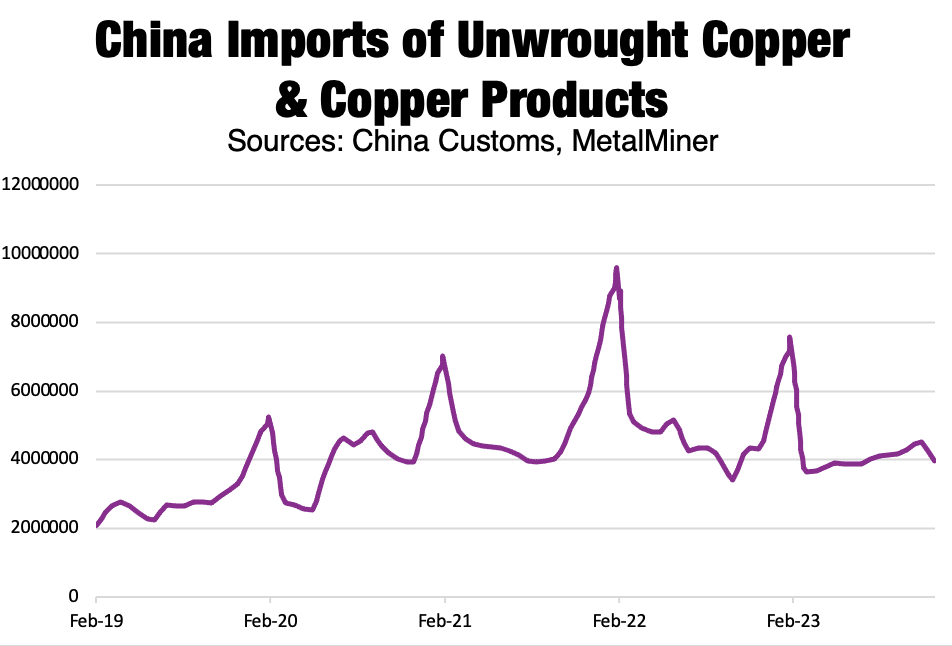

Thus far, China continues to see strong demand for copper. In fact, import levels for both copper products and copper ores remain robust. Much of China’s stimulus efforts over recent years strategically targeted its renewable and EV markets, both of which consume considerable amounts of the metal. While analysts expect both sectors to expand in the coming years, the outlook for copper prices today hinges upon whether that growth can outweigh declining copper demand from China’s property market.

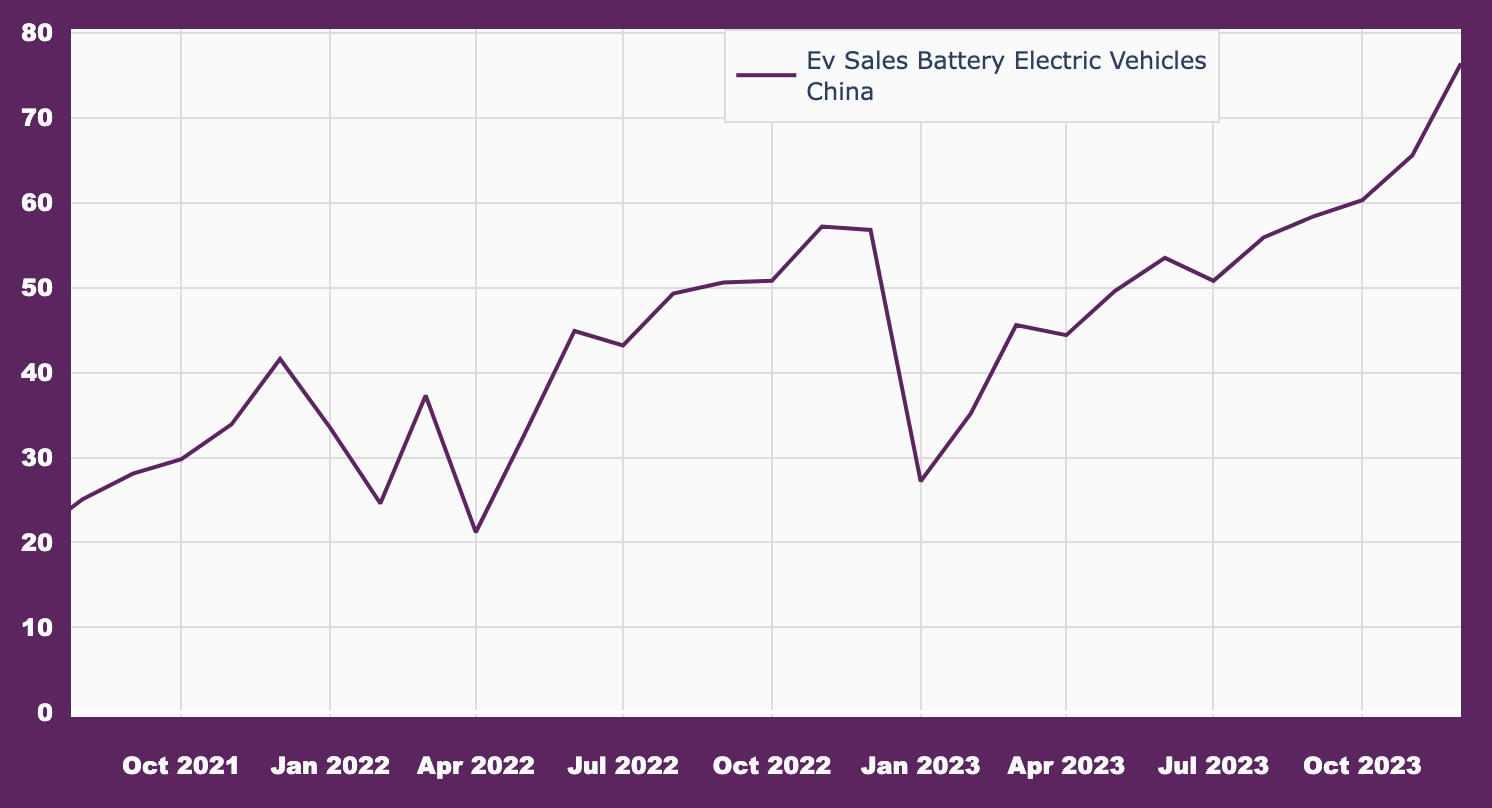

Meanwhile, China’s EV sector continues to report strong sales domestically and abroad. Furthermore, ample subsidies helped propel the sector into the world’s largest EV market. Though some long-term risks remain regarding Chinese consumer demand, producers continue to aggressively target the export market to support the sector’s growth. Data from the China Association of Automobile Manufacturers showed a 64% rise in overall auto exports from China in 2023. While the export data did not include auto type, EVs accounted for 24% of China’s total new car sales during the year (follow global macroeconomic trends impacting copper markets with MetalMiner’s weekly newsletter).

EVs use an estimated 3.5-4 times more copper than their ICE counterparts. Should China’s EV sector continue to grow, this fact alone would offer strong demand for copper. Moreover, EVs produced in China, aided in part by subsidies, sell at a discount to EVs produced elsewhere. According to the European Commission, Chinese-made EVs are, on average, a fifth cheaper than EU-made EVs. The discounted price of Chinese EVs not only gives China a competitive advantage within the global marketplace but also supports the widespread adoption of EVs, as prices remain a leading factor in consumer purchases.

Global Copper Price Trends Reveal Surprising Variations

Price differentials in other markets continue to see EV prices trend above their ICE counterparts, while subsidies in China caused EV prices to trend at a discount to ICE vehicles. And while export demand continues to support the growth of China’s EV sector, over-reliance on the export market comes at a risk should other countries institute protectionist measures against the lower-priced cars. Tesla CEO Elon Musk was among the industry voices calling for trade barriers against Chinese EV companies, which he said would “demolish most other car companies.”

Should governments heed Musk’s warning, this could cause a slowdown in both China’s EV sector and global demand for EVs. This, in turn, would threaten the outlook for overall global copper demand.

If you want copper market intel on a monthly basis that you can use as a purchasing indicator, opt in to MetalMiner’s MMI Report and stay posted on the global copper market, along with 9 other metal industries.

Tighter Ore Supply, Falling Stocks Offer Copper Price Today Headwinds

Despite China’s property sector risks, copper prices today continue to avert a downtrend, remaining within a long-term sideways range. Furthermore, tighter supply, global renewable growth, and eventual pivot from the Fed continue to offer support to prices.

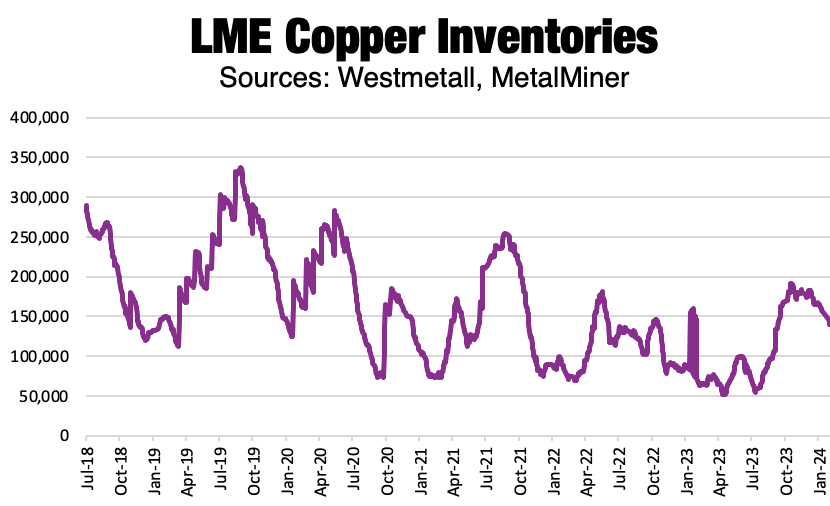

Following a strong rebuild during the second half of 2023, LME inventories have again started to trend lower. Meanwhile, mine supply constraints due to disruptions and closures have led to a tighter ore supply, which will prove a limiting factor for global copper supply over time. In fact, competition for ore saw Chinese processing fees drop to a record low, leading some smelters in the country to begin weighing production cuts.

While both mine supply and inventories offer a negligible correlation to copper prices, tightening supply will likely continue to fuel concerns over the projected supply deficit, particularly amid ongoing global renewable efforts.

Biggest Moves for Copper Prices Today

Read what’s next for copper prices in this month’s Monthly Metals Outlook. The report provides short- and long-term forecasts plus buying strategies to give you the edge in navigating market volatility. Secure a free sample report.

- LME primary three-month copper prices remained sideways, but still saw the largest increase of the index with a 0.52% jump to $8,625 per metric ton as of February 1.

- U.S. producer prices for copper grade 110 and 122 rose 0.4% to $4.97 per pound.

- Meanwhile, Indian primary cash copper prices fell 0.35% to $8.74 per kilogram.

- Japanese primary cash copper prices saw a modest 0.57% drop to $8,747 per metric ton.

- Chinese copper wire prices fell 0.7% to $9,687 per metric ton.