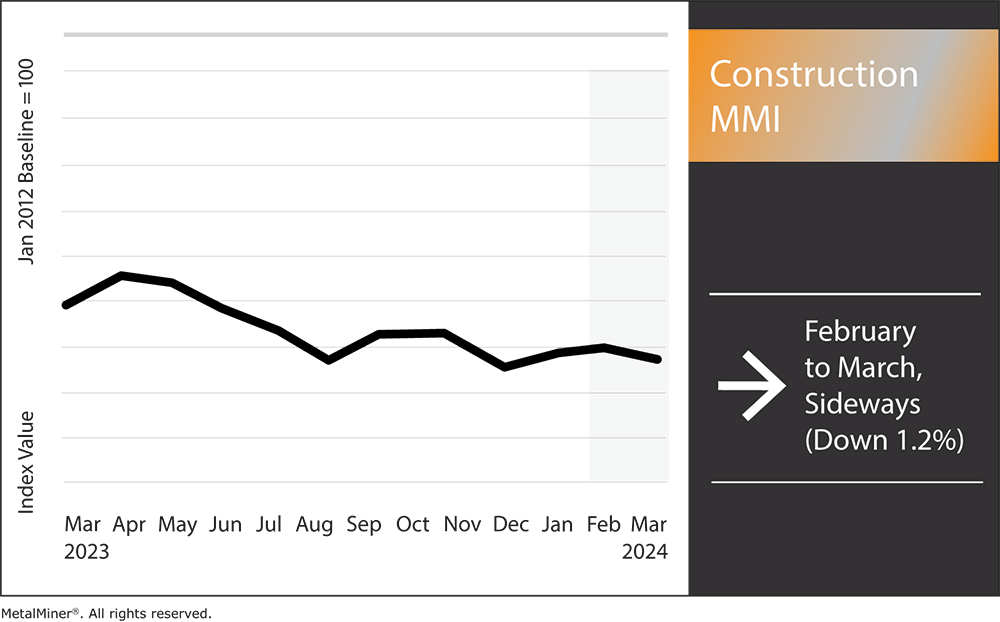

Month-over-month, the index experienced little movement. Overall, the Construction MMI (Monthly Metals Index) moved sideways, inching down just 1.2%. Steel prices moving downward placed some bearish pressure on the index. However, several significant factors continue to press on construction from both a bearish and bullish standpoint, including the Fed holding off on adjusting interest rates, weak domestic demand within China, and the strengthening manufacturing industry. With all of these factors in play, the index will likely continue its sideways movement, at least in the short term.

Potential Manufacturing Boom: Impact on Steel Prices

The recent increase in manufacturing activity transcends a temporary phenomenon. It now represents a fundamental transformation within industrial economics, with a significant chance of impacting steel demand. As industrial facilities experience heightened production and operation, the requirement for steel changes demonstrably.

The association between the manufacturing sector and steel prices dates back to the Industrial Revolution. However, this relationship has assumed a novel character within the context of the contemporary, hyper-connected global economic landscape. In most cases, it remains driven by technological advancements, shifting consumer preferences, and the evolving geopolitical landscape. The revitalization of manufacturing within key markets, including China, the United States, and Europe, continues to serve as a critical catalyst in propelling global steel demand.

Don’t settle for stagnant steel savings. MetalMiner’s custom price forecasting unlocks the true potential of your volume commitments, ensuring you maximize profit. View our full metal catalog.

Automotive and Infrastructure Helping Drive Steel Demand

A principal impetus for the potential resurgence in manufacturing activity stems from the rapid growth observed in sectors such as automotive production and infrastructure development, both of which hold the potential to dramatically impact steel prices. Notably, the automotive industry has once again emerged as a significant contributor to the escalating demand for steel. Likewise, the construction sector continues to experience a surge in activity, mainly driven by governmental investments in infrastructure projects aimed at stimulating economic growth.

Are you under pressure to generate steel cost savings? Make sure you are following these 5 best practices.

Manufacturing Industry’s Role in Driving Steel Prices

The manufacturing sector exerts a significant influence on the trajectory of steel prices. Industry analysts affiliated with the World Steel Association have documented a recent double-digit surge in steel prices (followed by a stabilization period and subsequent decrease, as noted in MetalMiner Insights). Such price volatility presents an opportunity steel producers to increase revenue, contingent upon the sustained strength of manufacturing demand.

Furthermore, the possibility of a manufacturing resurgence could constrict global steel supply chains, with certain regions encountering shortages and logistical impediments. In response to such situations, steel producers typically direct investments toward capacity expansion and operational efficiency enhancements to satisfy any escalating demand from manufacturing sectors.

Construction MMI: Noteworthy Price Shifts

Enjoying this article? MetalMiner’s monthly MMI report gives you updates on steel prices, market trends, and industry insights. Sign up for free.

- Chinese steel rebar moved sideways, shifting up by just 1.19%. This brought prices to $571.74 per metric ton.

- Chinese h-beam 200 steel barely at all, instead exhibiting a sideways movement. Prices rose just 0.33% to $496.44 per metric ton.

- European commercial 1050 sheet also moved sideways, dropping 2.24% to $3,148.57 per metric ton.

- Lastly, Weekly Midwest bar fuel surcharges dropped by 14.15%, leaving prices at $0.50 per mile.