Located approximately 25km south-west of Broken Hill in far western NSW, Australia, the Broken Hill cobalt project was primed to be a dedicated “ethically sourced, low emissions” cobalt mine.

The ready-to-build project, valued at A$560m ($348.76m) in 2020, was expected to offer around 400 full-time jobs and produce almost 17,000 tonnes (t) of high-quality cobalt sulphate yearly.

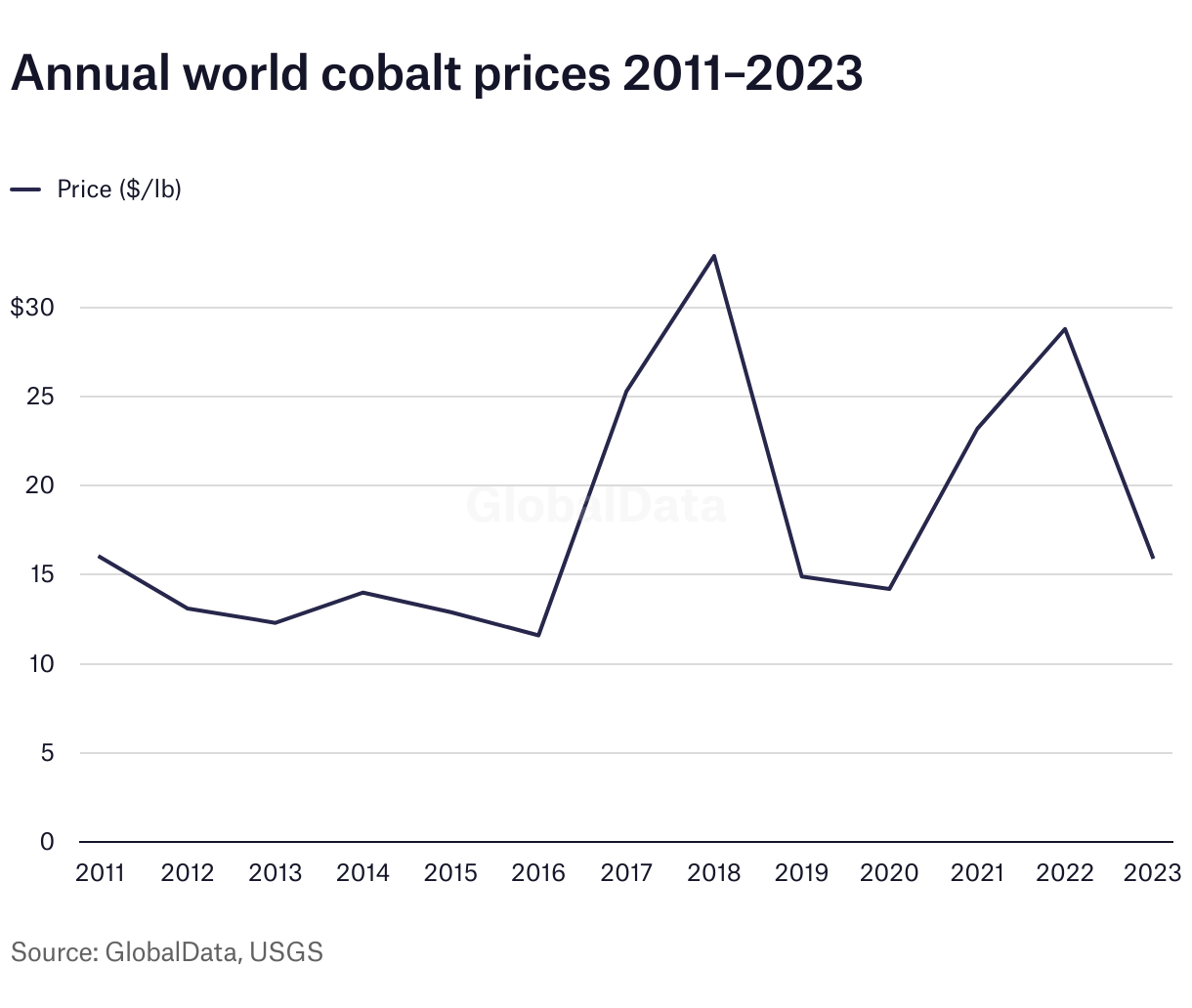

Then the price of cobalt crashed.

“It was just really bad luck,” says Joel Crane, commercial manager at Cobalt Blue, the company developing the project.

The price of cobalt has plunged from highs of $81,000/t in 2022 to around $24,000/t today due to an oversupply in the market. Similarly, the global price of nickel, of which cobalt is usually produced as a byproduct in Australia, fell from a high of $50,000/t in 2022 to an average of $16,200/t in the third quarter of 2024, according to GlobalData analysis.

The effect has been significant. BHP, for example, suspended all of its domestic nickel operations in October 2024.

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Your download email will arrive shortly

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalData

“You have got basically all the nickel mines in Australia shut, all the major lithium producers cutting. It is death out there. It is horrific,” says Crane.

Cashing in on subsidies and green premiums

Australia is one of the top three countries in the world for cobalt reserves, which in 2024 were estimated to be around 1.7 million tonnes (mt), according to GlobalData, Mining Technology‘s parent company. Yet the mining nation only produces around 2% of the global supply, with Glencore’s Murrin Murrin project being the largest supplier, producing 2,100t in 2023.

Along with other energy transition minerals, many miners are keen to maximise the untapped opportunity Australian cobalt presents. Cobalt Blue’s Broken Hill project is one of them. The project is unusual because it is a dedicated cobalt mine – 98% of which is normally produced as a by-product from nickel or copper. It also plans to integrate the whole value chain from production to producing battery grade material, whereas most mines produce an intermediate that is sent to China for processing.

Cobalt Blue is targeting the market for so-called “responsibly mined” cobalt. The Democratic Republic of Congo (DRC) produces around 70% market supply, but its industry has at times been marred by corruption and human rights abuses and is said to have lesser regulatory standards than Australia. Australian supply can therefore market itself as being easily traceable and more ESG (environmental, social and governance)-compliant.

However, it is not just the ESG market that has attracted Cobalt Blue and others. Generous US subsidies have been on offer since 2023 under US President Joe Biden’s Inflation Reduction Act (IRA) for electric vehicles (EVs) that contain 40% of non-Chinese produced critical minerals.

Chinese companies control nearly half of all cobalt supply and China refines 73% of the world’s cobalt (predominantly from the DRC).

Subsidies have been a big driver for new projects in compliant countries such as Australia, the US, Canada, as well as in Europe and some of the Americas. It was hoped they will galvanise sales in the slower-than-expected EV market, but so far have not been enough to counteract the plunging cobalt price.

Premium pricing for sustainably produced Australia cobalt

Cobalt Blue, which was founded in 2016 and is Australian Securities Exchange (ASX)-listed, is now building only the refinery part of its project. The first phase of this is a A$60mn facility that will process 3,000 tonnes per annum cobalt (tpa) as cobalt sulphate and around 500tpa as nickel (as nickel metal). Construction is expected to start in early 2025 and will take 12 months.

The mine, which had been designated federal ‘Major Project Status’ and given a federal grant of A$15mn, has been mothballed – for now.

This highlights the tough economics for projects in Australia that are subject to high labour and overall costs compared with their African and Chinese counterparts – and the need for a price premium to be paid. This is something Crane strongly believes will eventually be available for non-Chinese products.

“The reason I feel so strongly about that is because if you are going to purchase lithium, cobalt or nickel from non-Chinese sources, you will have to pay more simply because – and we know this well – the cost structure is about 30% cheaper in China,” he says.

“But right now, it is very difficult to speak to a procurement officer at BMW, for example, and say it is going to cost you more.”

Investments in IRA-compliant products that come with a higher price tag are starting to happen, however. In October, General Motors signed a prospective deal worth $500m for a lithium project in Nevada. Crane, who used to work for Rio Tinto, says the company operates renewable-powered aluminium smelters in Quebec and sells its product to Apple and Nespresso at a premium.

Managing director and CEO of Alliance Nickel, Paul Kopejtka, says companies are also already paying a premium for more sustainably produced nickel and cobalt.

“I can say that because we have a contract with [carmaker] Stellantis. And I can tell you that the Western OEMs and all battery manufacturers will pay that premium for low carbon IRA-compliant nickel,” he says.

Alliance Nickel is developing the NiWest Nickel Cobalt project in the West Australian nickel belt, adjacent to Glencore’s Murrin Murrin nickel-cobalt operation.

In November, the NiWest project released its definitive feasibility study, which Kopejtka says proves its bankability. It is now looking to secure financing.

Due to the unique geology of the project, it can use less-carbon-intensive heap leaching instead of high-pressure acid leaching. The process burns sulphur to make acid generating steam that can be used to power the mine and refinery, meaning it is lower carbon and also lower cost than comparable mines in Indonesia, Kopejtka says.

Kopejtka has also committed to independent ESG audits as “part of the deal” with Stellantis.

What if the IRA is rolled back?

Regulation such as the IRA and the EU’s Critical Raw Materials Act (CRMA), which require percentages of domestically produced minerals, are clearly driving interest in Western-based development of cobalt and nickel projects that can possibly negotiate a premium – but what if the IRA gets rolled back under Trump’s anti-green incoming administration?

The belief among affected industry – relevant mining projects but also those in the renewables space – is that it won’t, or at least not completely.

“I think, at the end of the day, it won’t be as bad as it is made out because the Trump administration can’t just walk away from this energy transition and much of the IRA money, hundreds of billions, has gone to red Republican-voting states,” says Kopejtka.

However, he acknowledges that between now and 20 January 2025, when Trump takes office, “there be will uncertainty”.

Future outlook for cobalt in Australia

Marina Demidova, head of communications at the Cobalt Institute says it expects the price of cobalt to be “back in good shape” by 2030. At this point demand will pace supply, and Australia will be “well positioned” in the market, she says. The region, like others, should focus on developing its value chain to create more opportunities, she adds.

GlobalData also points out in a recent report that Australia and Canada, among others, “are rapidly becoming key players in the global cobalt market, though they account for only 1.9% of the global share in 2024”. This figure is projected to increase to 6% by 2030, close to the current market share of Indonesia, they add.

To support the industry in the more immediate term, the Australian Government is offering a Critical Minerals Production Tax Incentive worth 10% of relevant processing and refining costs for Australia’s 31 critical minerals, of which cobalt is one. This incentive covers critical minerals processed and refined between 2027 and 2028 and 2039 and 2040, for up to ten years per project.

When considered through the lens of available capacity for IRA-compliant, battery-grade cobalt (sulphate), it is clear there is an immediate shortfall that only grows as the IRA restrictions tighten into 2027 (from 40% to 70%).

Globally, the International Energy Agency predicts a 16% cobalt shortfall by 2035, when many EV mandates kick-in, versus project pipeline, with a high political risk of mining from one single country.

For now, it is a waiting game. “If the long-term price was higher [$40 per pound] there would be plenty of particularly progressive automakers or battery makers who see what is going to happen over the next few years, and they will buy,” says Crane.

Cobalt Blue already has a provisional agreement with a Japanese partner, which Crane describes as “very progressive”.

However, Crane does not believe there is going to be a new mine built in Australia for five years, unless it is for gold or copper, but there will be processing – something seen as a strong value-add for the sector.

Things are expected to shift but “it could be tomorrow, and it could be in five years”, he says.

“Some of these cycles have churned along the bottom for a long time. I don’t think that’s going to [continue to] happen, because the world is very different now, and things change very quickly.”

“The demand for lithium, nickel, cobalt is absolutely outstanding – 5–10% annual demand growth, which in the commodity world is massive.”