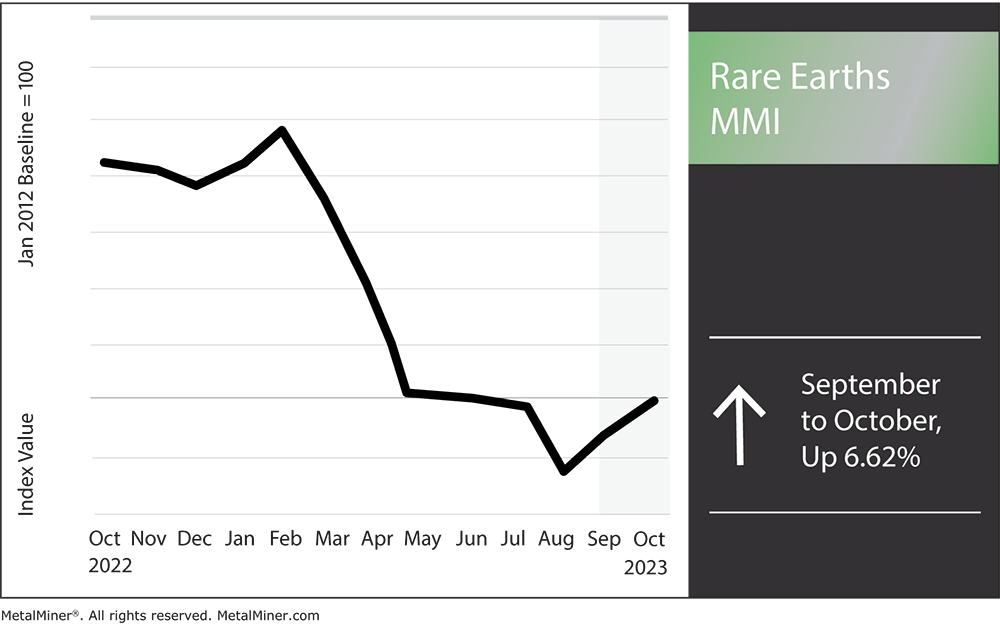

The Rare Earths MMI (Monthly Metals Index) witnessed yet another steep increase month-over-month. Indeed, supply disruptions remain a massive concern in the rare earths industry, so rare earth magnets and other materials witnessed renewed bullish strength across the board over recent months.

In August, market worries arose prior to a planned environmental inspection of China’s Jiangxi province. The Chinese region serves as a major location for Chinese rare earth supplies. Along with this, Chinese stimulus efforts managed to boost rare earth production (although this cannot add long-term support to the index).

Following this, Myanmar’s Kachin State suspended mining activities. Myanmar (formerly Burma) is a pinnacle producer of global rare earths and rare earth magnets, and any change in Burmese mining activity can significantly alter the market. Therefore, the mining suspension led to stockpiling ahead of peak consumption and caused Chinese rare earth prices to hit their highest point in over 20 months.

As a result of all of this, the index jumped up by 6.62%

Stay ahead of rising rare earth prices and make timely purchasing decisions with MetalMiner Insights’ instant market-shift alerts. Ready to learn more?

How Will the Burmese Mining Suspension Impact Rare Earth Prices Globally?

From January to July 2023, Myanmar’s Kachin State supplied 38% of rare earth materials imported by China. Despite this, mines in the Burmese state shut down in early September to prepare for inspections. This shutdown raised anxiety about supply interruptions and prompted the hoarding of rare earth materials worldwide.

For now, analysts expect the recent mining restriction in Myanmar’s Kachin State to have the most impact in the short term. However, it could also affect long-term rare earth pricing.

Short-Term:

- Pricing has already factored in the immediate effects of the mining ban. Still, rare earth prices will continue to see support from the long-term supply disruption and stable demand outlook.

- Fear of higher prices will also drive increased demand in the fourth quarter of 2023, as rare earth consumers stockpile cargo for use during China’s public holiday from September 29 to October 6.

Long-Term:

- While the long-term effects of the mining restriction remain unknown, it could result in a scarcity of rare earth minerals, further increasing costs.

- The restriction might also lead to increased illicit mining, which is already a significant problem due to China’s control over rare earth mining in Myanmar. Over time, this could exacerbate environmental issues in the region and lead to political unrest.

- Additionally, the restriction could eventually cause harm to Myanmar’s economy and its mining sector workforce.

Get insights on global rare earth dynamics and commodity price drivers with MetalMiner’s free weekly newsletter.

Global Rare Earth Trading Dynamics Changing

China’s sluggish economy has negatively impacted rare earth prices for months, even without the Burmese mining ban. Therefore, a rise in Chinese economic activity could benefit the market. However, recent predictions indicate that China’s economy will slow down in 2024 due to ongoing domestic challenges and a lackluster property sector.

While China’s property sector does not directly influence the production of rare earth magnets, a potential “domino effect” could continue to harm the pricing of industrial metals that rely on Chinese imports.

China’s rare earth policies have long affected the market power and pricing of rare earth metals. Private Chinese enterprises engaging in intense rivalry lowered rare earth prices during the first two decades of their worldwide availability. China then started reducing rare earth shipments in 2006, citing the need for resource conservation and environmental concerns, which resulted in a sharp increase in rare earth prices.

Don’t ship your pants. Learn all about near-shorting as an alternative to sourcing rare earth magnets and other metals from China in MetalMiner’s October Workshop “Don’t Ship Your Pants – Options for Near-Shoring.”

Geopolitical Risks Heavily Tied into Supplies of Rare Earth Magnets

China’s current economic slowdown has substantially impacted the rare earth elements market. It has also emphasized the necessity of diversifying sourcing and the risks associated with excessive dependence on a single country for essential raw materials. Indeed, as China’s domestic demand for rare earths increases, the nation will rely more and more on imports from countries like Myanmar to meet its resource requirements.

Interestingly, a recent study utilizing the wavelet decomposition method established a link between rare earth price fluctuations, geopolitical risk, and global economic activity. According to this study, there is a positive correlation between rare earth pricing and global economic activity. This implies that a slowdown in China’s economy may lead to a drop in rare earth prices. However, the study also found an inverse relationship between the price of rare earth magnets and geopolitical risk, suggesting that political unrest in China could instead cause rare earth prices to rise even more.

Rare Earths MMI: Notable Price Shifts

- Neodymium oxide rose by 4.81%, bringing prices to $73,333.88 per metric ton.

- Rare earth carbonate also increased month-on-month. Prices ultimately went up by 4.03%, reaching $5,780.19 per metric ton.

- Praseodymium neodymium oxide increased by 4.07%, leaving prices at $71,394.25 per metric ton.

- Finally, terbium metal increased the most month-on-month. Altogether, prices went up by 7.31%, reaching $1,457.14 per kilogram.