Support CleanTechnica’s work through a Substack subscription or on Stripe.

BEVs had a record month and represented 37% the total Chinese car market in September.

We saw plugins score another million-plus sales in September (1.3 million plugins, in a 2.2-million-unit overall market, up 6% YoY), but growth has been slowing down, with September showing a 16% increase over September 2024.

Digging deeper into the numbers, BEVs continued to grow, going up by 29% to 826,000 units, a new record, or 37% of overall sales. PHEVs were down again, this time by 3% YoY, to some 469,000 units. Counting both powertrains together, we get 1.3 million units, the second best month ever, and only a few thousand units below the all-time high set last December.

With BEVs continuing to grow by double digits and PHEVs accumulating months in red, have we reached a turning point in PHEV adoption?

These results pull the year-to-date (YTD) tally to over 8.9 million units. So, we should see plugins reach the 10 million unit mark if not in October, then surely in November….

This result pulled the September share to 58%, or 5% above the 53% result of September 2024. BEV share of the market rose to 37%. Expect to see plugins continue to grow their share in the following months. For now, plugins have 52% of the total auto market this year (32% just for BEVs), which means that most new cars sold in China this year have a plug!

(Could China reach 55% plugin vehicle share by year end? And be fully electrified before 2035?)

Regarding exports, in September, they were up 97% YoY. Plugins represented 40% of the total number of passenger cars exported from China, which means that exports are less electrified than domestic sales.

Interestingly, much of the export market growth is coming from PHEVs. This technology now represents 33% of all Chinese plugin exports, whereas 12 months ago, it represented just 17% of total EV exports….

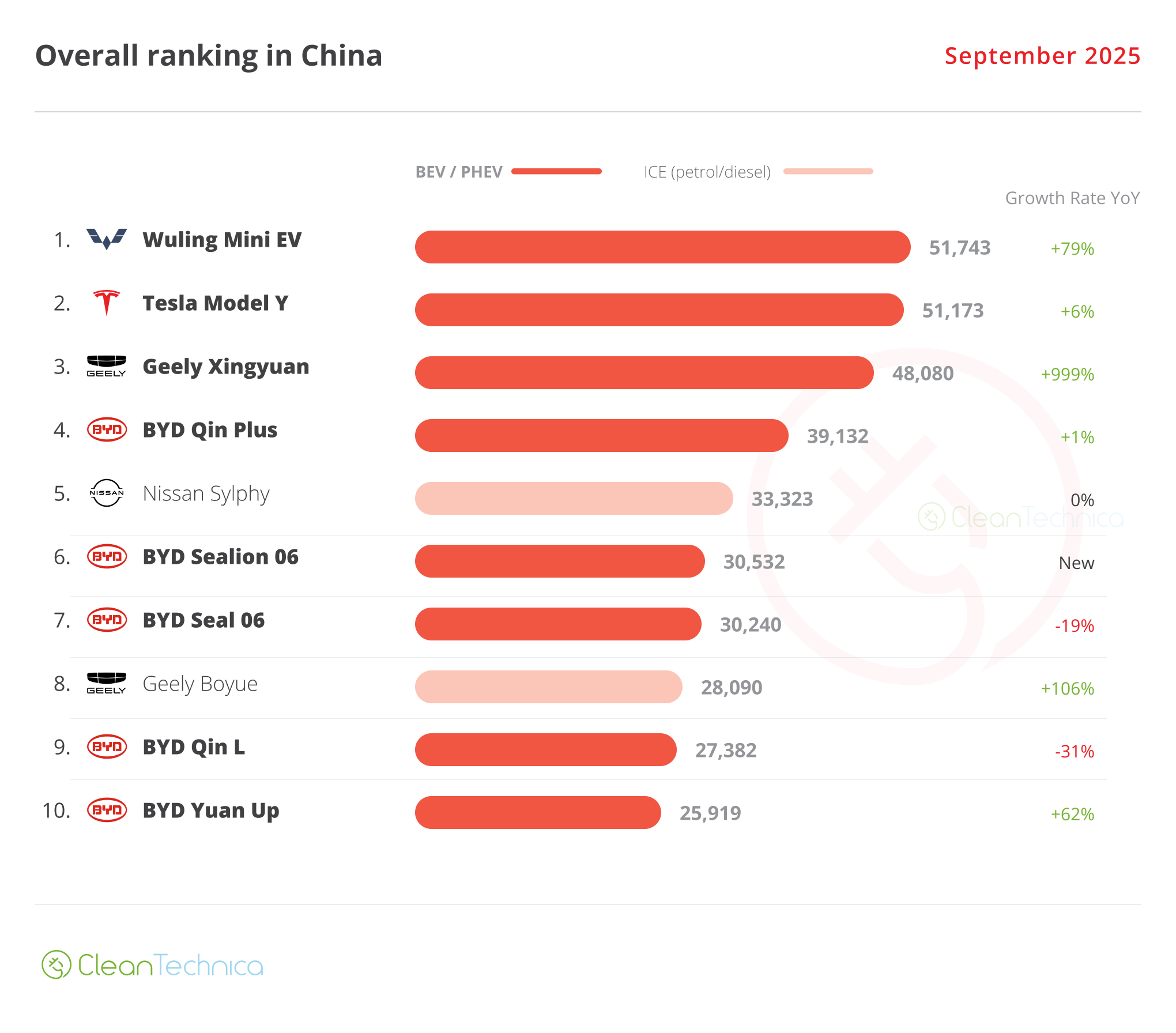

In the overall ranking, in September, fully fossil-fueled models had just two representatives in the top 10. The best placed was the Nissan Sylphy in 5th, a surprisingly good standing for the compact sedan, while the other 100% ICE model, the Geely Boyue, was something of a surprise. The Chinese crossover saw its sales double year-on-year, currently something of a rarity for an ICE model.

Still, I believe it will be only a matter of time before we have just one pure ICE representative on the table. But it should still take some time until we see a 100% plugin top 10.

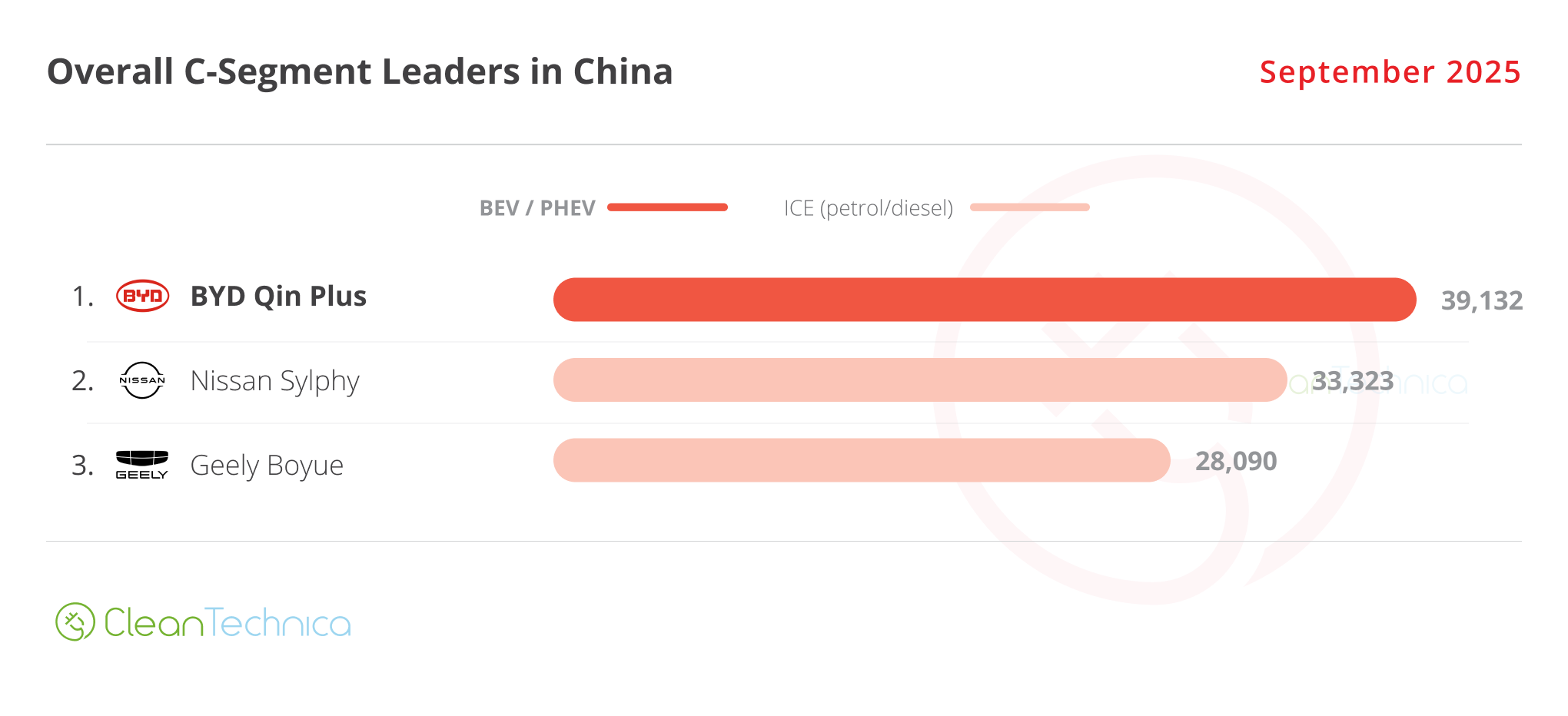

Looking at the best sellers in several size categories, all but the C segment (compact cars) have 100% plugin podiums. In fact, the C segment is the only segment where ICE models still have representatives. In all other categories, ICE models were absent. This is a recurring theme. So, it’s clear by now that the C segment is the hardest of all to convert into EVs.

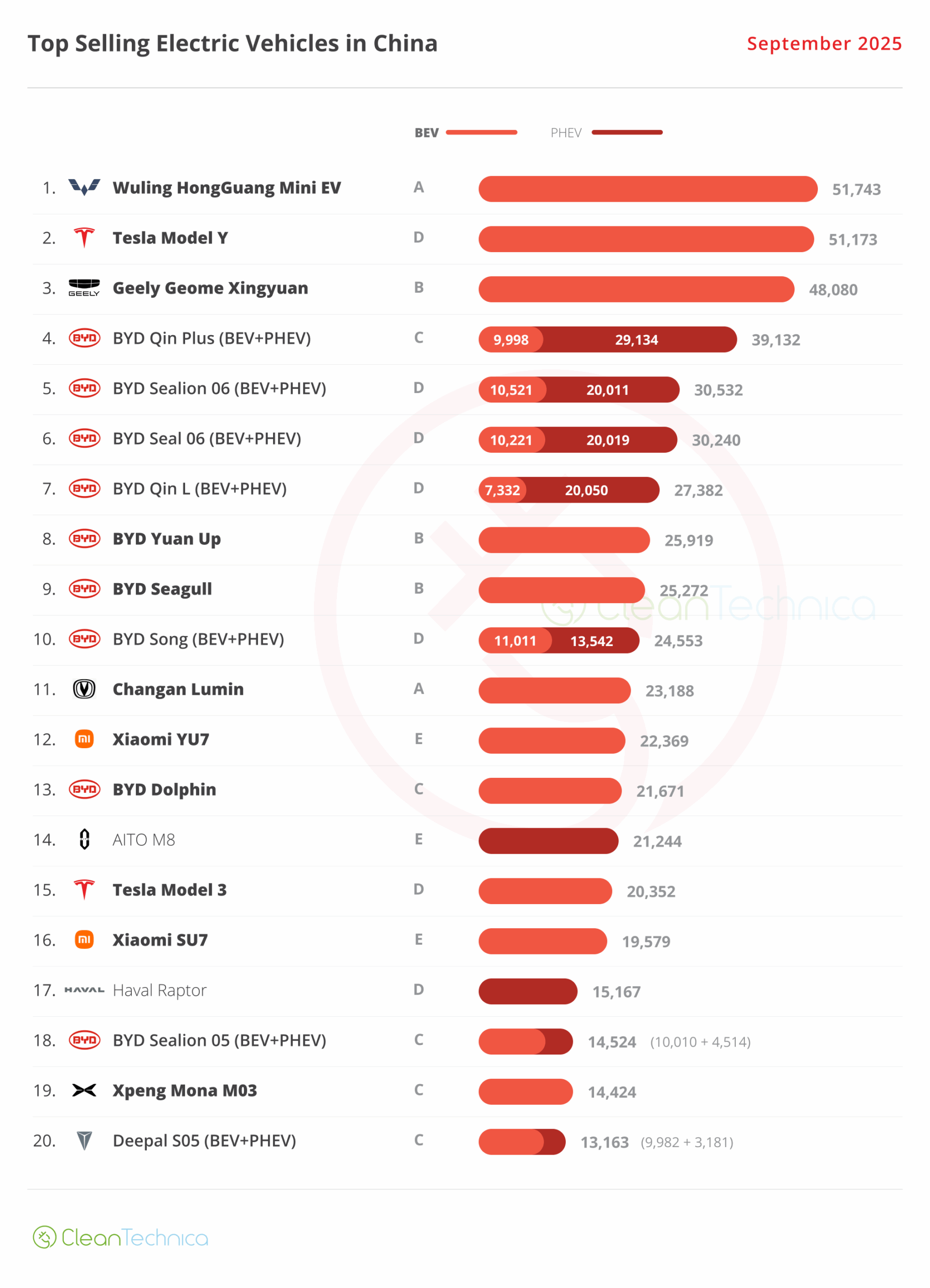

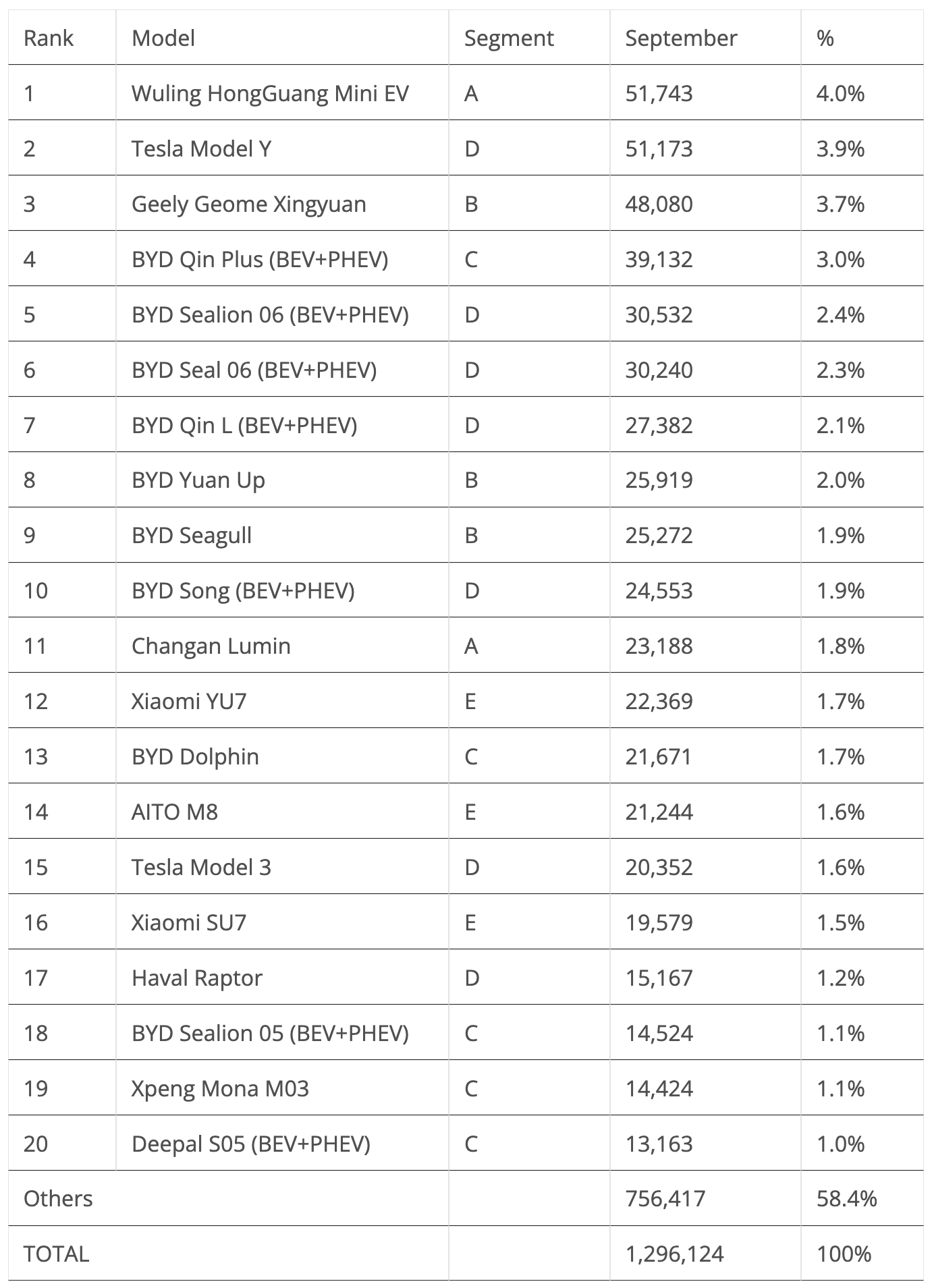

Looking at individual models, the biggest surprise was the podium for the full size category. Xiaomi’s YU7 won the category title in September, and on top of that, Xiaomi had its other model, the SU7 sports sedan, reach the category podium. However, the cell phone maker turned EV startup didn’t get a #1 + #2 win in the full size category this time, as the AITO M8 ended the month between the two Xiaomis.

Elsewhere, while the Wuling Mini EV (A segment) and Geely Xingyuan (B segment) dominate their categories, the BYD Song has disappeared from the midsize podium, giving way to the recently introduced BYD Sealion 06, which now has the role of racing against the Tesla Model Y.

Here’s more info and commentary on September’s top selling electric models:

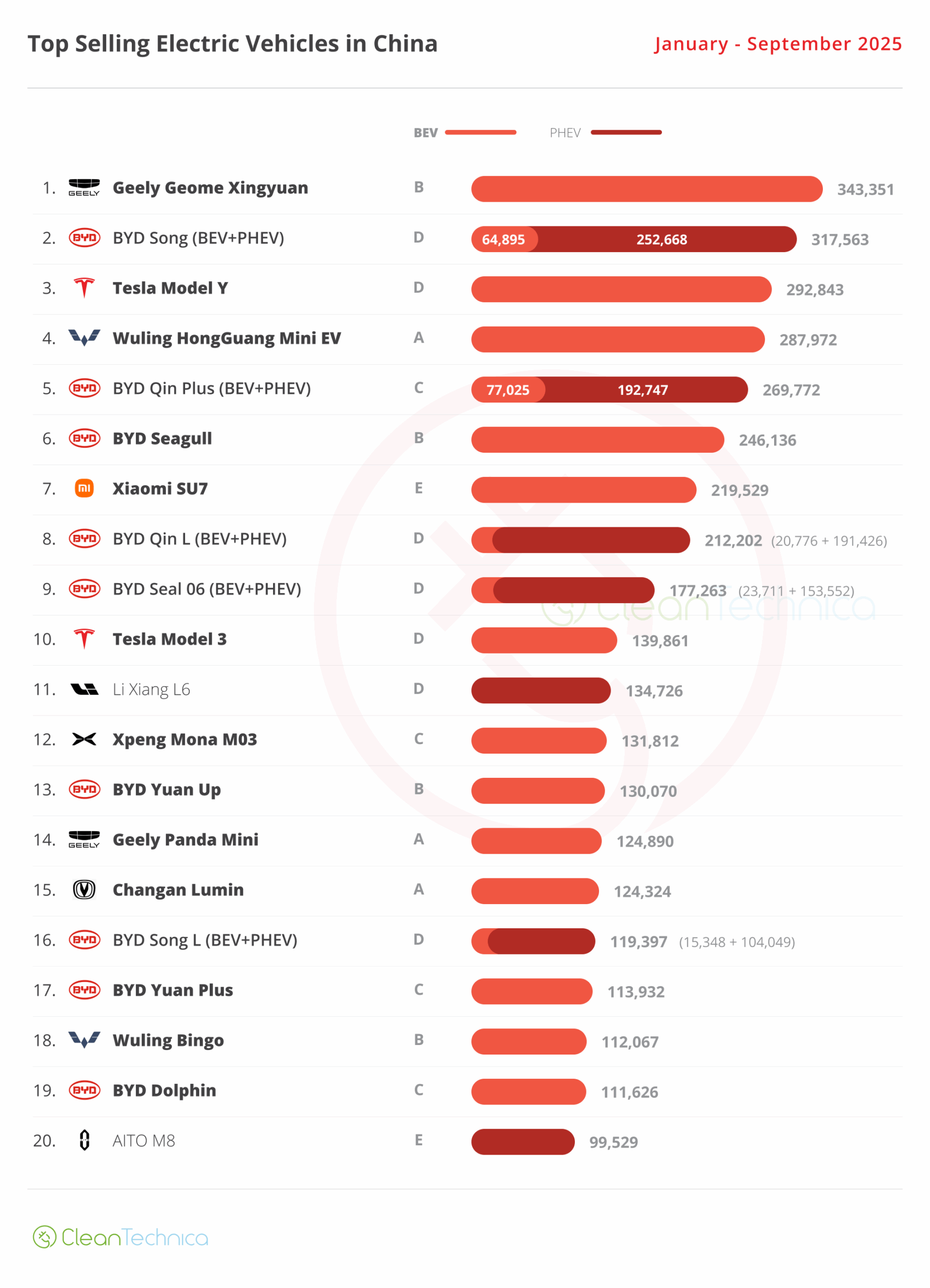

#1 — Wuling HongGuang Mini EV

This tiny EV is taking full profit from its generation change, which happened late last year. It is now back among the top sellers, and in September it collected 51,743 registrations, a significant 79% increase year-on-year, allowing it to snap up the leadership position in that month, its first since July 2022. Thanks to a more rounded design, which kind of reminds of the face of a Panda, and upgraded specs and interiors, SAIC’s smallest hatchback has lost its barebones feel. It now looks more car-like. Wuling even offers a five-door version! Despite all of this, the price hasn’t increased that much, with SAIC’s star model starting at $5,500.

#2 — Tesla Model Y

Last year’s silver medalist had a positive month in September, growing 6% YoY to 51,173 deliveries, in part thanks to its new 6-seat version. This provided it with a podium position. Tesla is clearly trying to stop the sales bleed with new variations, but will it be able to go back to the good old days? Unless Elon has a trick up his sleeve, I very much doubt it, especially with new competition like the Xiaomi YU7 and others like it. The YU7 got hundreds of thousands of locked-in orders within hours. Those orders have to come from somewhere, and with the market already at 50% share, it won’t be just from ICE models…. Yep, Tesla, but also BYD, will suffer.

#3 — Geely Geome Xingyuan

Geely has struck gold with this one. After a number of failed attempts to launch models that would stay in the best sellers table (Galaxy L6, Galaxy E5, etc.), the Hangzhou make finally found the winning formula to not only beat BYD, but also win the leadership race in the fierce Chinese automotive market. With BYD owning most of the market segments, thanks to multiple popular models, the little Xingyuan profited from the fact that BYD was underrepresented in the lower segments, which had left a space between the A to B segment Seagull and the B to C segment Dolphin. With pricing and specs closer to the Seagull, but with an interior space and quality closer to the Dolphin, the small Geely carved out a space of its own, which has been expanding in every passing month. This September, the small hatchback dropped to the last position on the podium, but it still managed once again to continue in record mode (for the ninth month in a row!) thanks to a best ever score of 48,080 units. Starting with an 80,000 CNY (+/-$11,000) price, the buyer gets a 30 kWh LFP battery from CATL, which is nothing to write home about until you realize that its price is closer to the BYD Seagull’s (70,000 CNY for the 30 kWh version) than the BYD Dolphin’s (100,000 CNY). Exports? Surely that must be on the cards. But first, Geely will need to finish the production ramp-up and satisfy its own internal market.

#4 — BYD Qin Plus (BEV+PHEV)

The old dog once again joined the top 5 in September, thanks to 39,132 registrations, a rather good performance. Its sales stayed essentially flat (+1% YoY), and it was once again the best selling BYD on the table. In the same period, its brother in arms, the Song, was down to less than half of last year’s sales! By the way, this was the second consecutive month without any BYD representative on the podium. Troubles ahead for the Shanzhen make? Back to the Qin’s performance, this volume meant that it was the best selling sedan in China, all powertrains counted. The 7-year-old body might be showing some wrinkles, but the low prices still provide significant demand for the sedan.

#5 — BYD Sealion 06 (BEV+PHEV)

BYD’s new midsize crossover scored 30,532 registrations, which was a good performance considering it was only its second full month on the market, and allowed it to win its first top 5 standing, no doubt the first of many. But with the BYD Song apparently going into EV Heaven and the Song L failing to live up to the predecessor’s career, will the Seal 06 be the one to replace the Song on the top of the sales charts? It is positioned at around 150,000 CNY (around 22,000 USD) and has the standard BYD qualities of value for money, design and connectivity. On the EV specs side, the PHEV version has an above average 27 kWh battery, and the BEV version’s top battery has an unimpressive 79 kWh. Also, the 800V architecture is a plus at this price point. This means that the Sealion 06 has enough value for money to have a good career, but it will be difficult, if not impossible, to repeat the Song’s three-peat title streak (2022, ’23, and ’24), as the competition is increasingly more competitive and the Sealion 06 lacks standout features and specs.

Looking at the rest of the best seller table, despite not having any representative on the podium, BYD took over of all places between 4th and 10th, with the Seagull (9th) and Song (10th) in unusually low places. While the SUV’s place can be justified by the fact that it is nearing the end of its career, the Seagull’s drop (-47% YoY) is harder to understand.

Elsewhere, we have two fresh faces (the Haval Raptor and Xiaomi YU7) that stayed on the table, and another that just debuted in the top 20, in the form of Changan’s Deepal S05.

Outside the top 20, we have a number of models landing with a bang this month, with BAIC’s Arcfox T1 being the most impressive of them, not only because it scored a rare five-digit debut month, 10,096 registrations, but also because it is coming from the BAIC stable. BAIC is an OEM that has been outside the top positions in the past few years but has three Best Selling Model trophies in the bag (BAIC EC-Series in 2017 & ’18 and BAIC EU-Series in 2019).

The others were the Fangchengbao Ti7, another rugged SUV coming from BYD’s premium brand, that landed with 8,128 registrations, and the highly anticipated new generation Xpeng P7, which started its career with a strong 8,104 registrations. All the while, the new generation MG 4 is already starting its career with a strong 11,790 registrations. So, although the new MG hatchback doesn’t look as sharp as the original one, it is already leaping ahead of the early sales results of the first generation. It will be interesting to see how the European market will react to it.

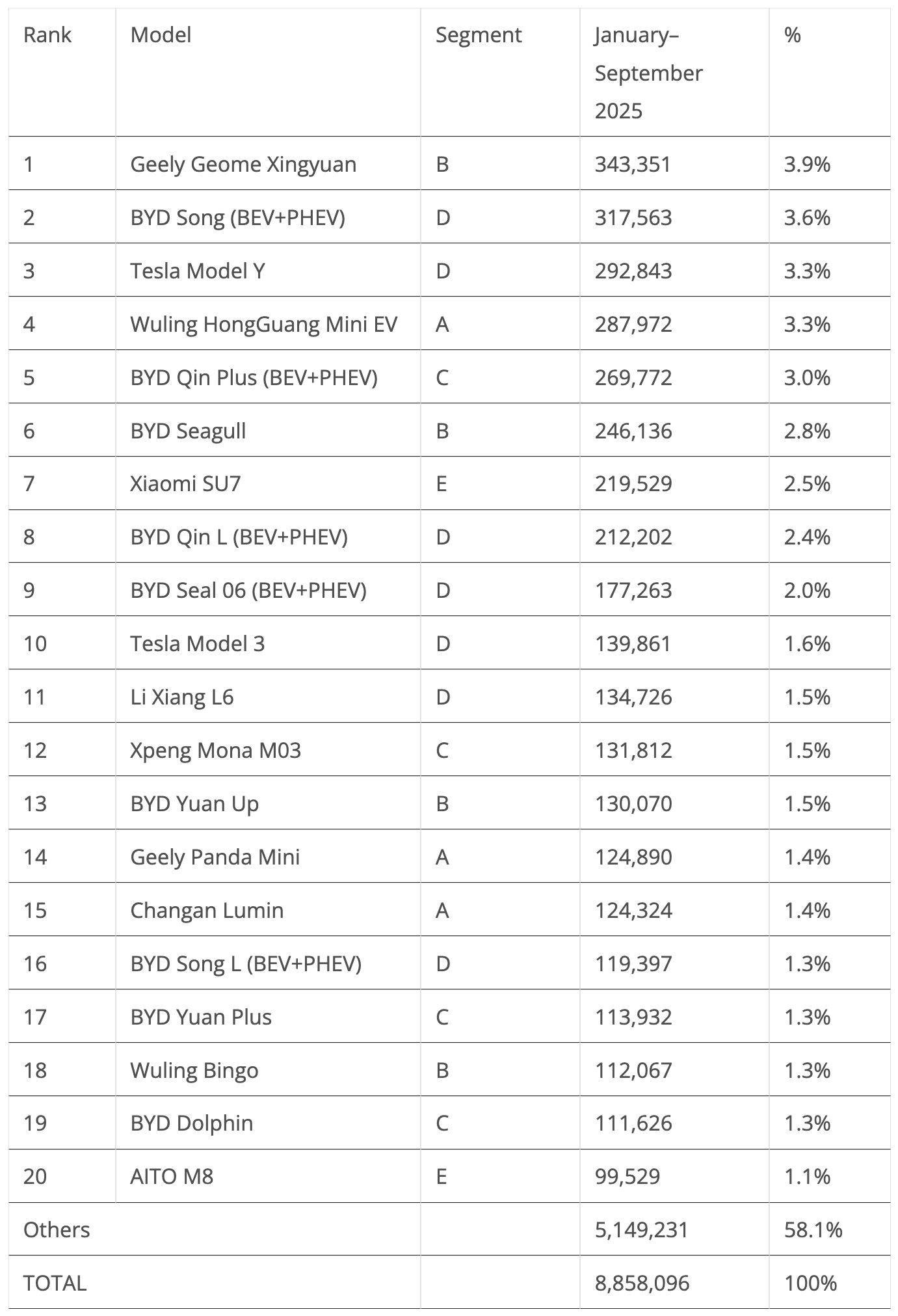

The Geely Xingyuan consolidates power

Yep, looking at the 2025 ranking, the little hatchback seems poised to succeed the aging BYD Song as the best seller in China, and considering current sales trends, it seems the Geely model won’t leave that position anytime soon.

If this trend gets confirmed and the Xingyuan wins the title this year, it will be a first for the Geely conglomerate, and the end of a three-year reign of the BYD Song. And to think that, up until this year, no model from the Geely mothership had even made it to the podium….

Segment-wise, this would also be a significant change. After two years of podiums made up entirely of midsize models, 2025 could be the year that small cars regain protagonism on the podium.

After all, the #3 Tesla Model Y has the tiny Wuling Mini EV just 5,000 units behind it. So, although the US crossover remains the favorite for the bronze medal, it is not impossible that the little city car could end in 3rd. Now, imagine that — two small EVs on the Chinese podium! And people say that small EVs aren’t competitive….

Also interesting to see in the current standing is that we have four models in the top positions, from four different brands! Hurrah for diversity!

Further down, there were a few position changes. Despite a so so month in September (it saw its sales drop 15% YoY), the Tesla Model 3 benefitted from a horrible month from the Li Xiang L6 (down 52% YoY) to surpass it and reach the 10th spot.

Further below, there was good news for BYD, with the Yuan Up climbing two positions in September to #13. But the Climber of the Month was the cute Changan Lumin, which jumped from 18th to 15th position.

Finally, AITO’s M8 large SUV joined the table at #20.

Looking at the overall manufacturer ranking (not just electrics), it seems BYD has found the demand ceiling in its domestic market. September was another month in red, as it saw its sales drop by a significant 16% YoY, the third month in a row of significant drops.

On the other hand, #2 Geely is far from these issues, having seen its sales jump 62% September. This is while most foreign representatives are either stagnating or seeing sales drop. (Most, but not all — Audi was 10th thanks to enviable 11% growth YoY.)

Above Audi, we have the other highlight of the month — fast-growing Leapmotor was at #9, thanks to almost 60,000 registrations. That’s an 85% jump YoY. The startup is currently at the top of its game, and now that it has become profitable, the Valley of Death is behind the nine-year-old startup. A top 5 position seems not only possible, but likely.

But Leapmotor’s startup leadership could be short-lived, because there are two unstoppable trains coming from behind Leapmotor. One is called Xiaomi (#15 in September, up 209% YoY), while the other is Xpeng (#19, up 201% YoY). Which one of them will be the best selling EV startup in 2025? Please place your bets.

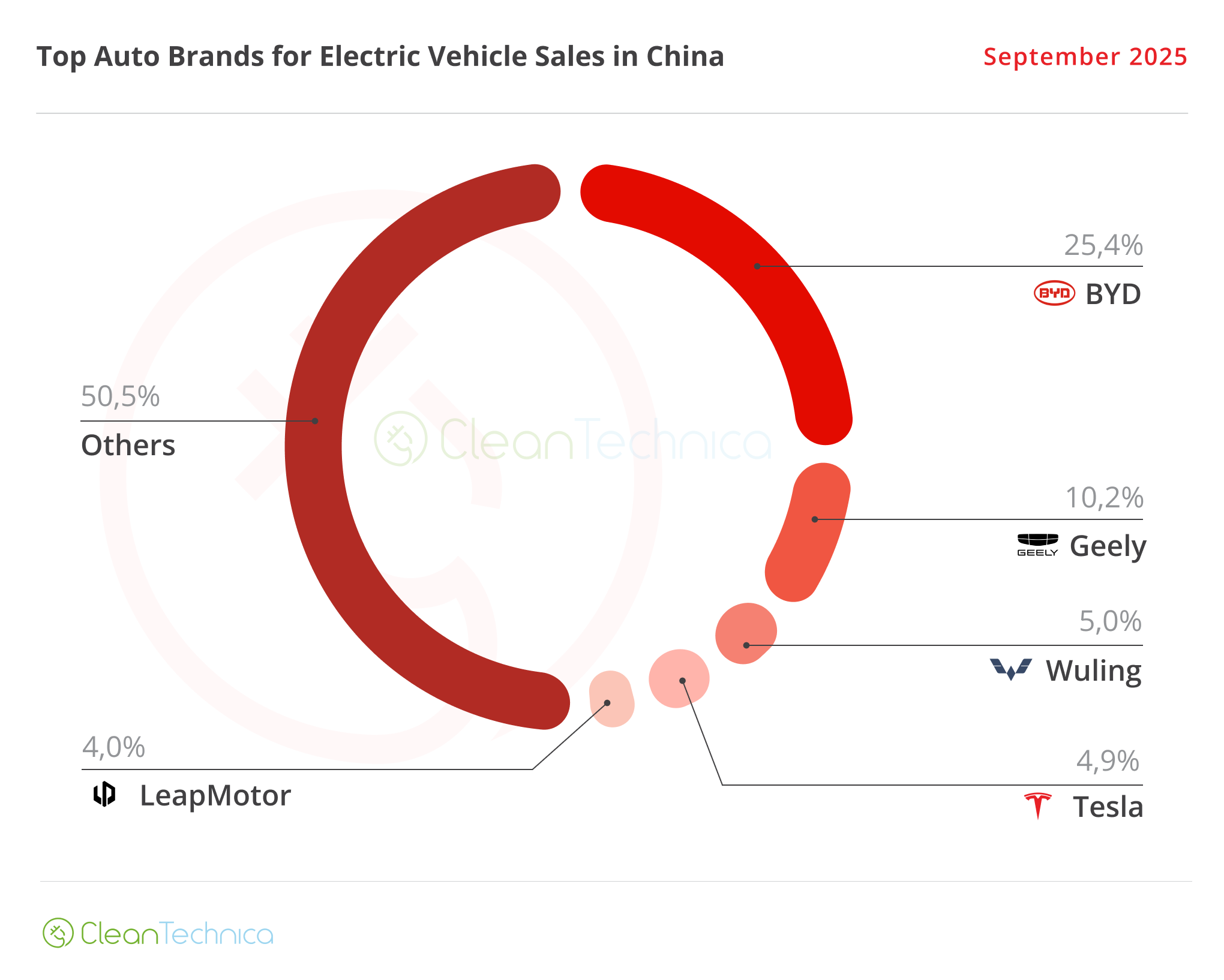

Auto Brands Selling the Most Electric Vehicles in China

Looking at the auto brand ranking for plugin vehicles, there isn’t much news. BYD (25.4%, down from 25,8%) continued its slow descent, but has its leadership position secured this year. #2 Geely (10.2%) is just too far behind to bother in any way.

Wuling (5%) stayed in the #3 spot, but lost some of its advantage over Tesla, which gained some share (4.9% now vs. 4.8% in August).

This means that, with two thirds of the year passed, for the first time since 2019, Tesla can’t reach the podium of the Chinese EV manufacturer table. Will this standing stay this way until the end of the year?

Elsewhere, a rising Leapmotor (4%, up from 3.9% in August) has gained ground over #6 Li Auto, which continues to slide (3.4% now vs. 3.5% in August). In fact, #7 Xpeng (3.2%) is also looking to get closer. Will the Guangzhou startup be able to surpass Li Auto in Q4?

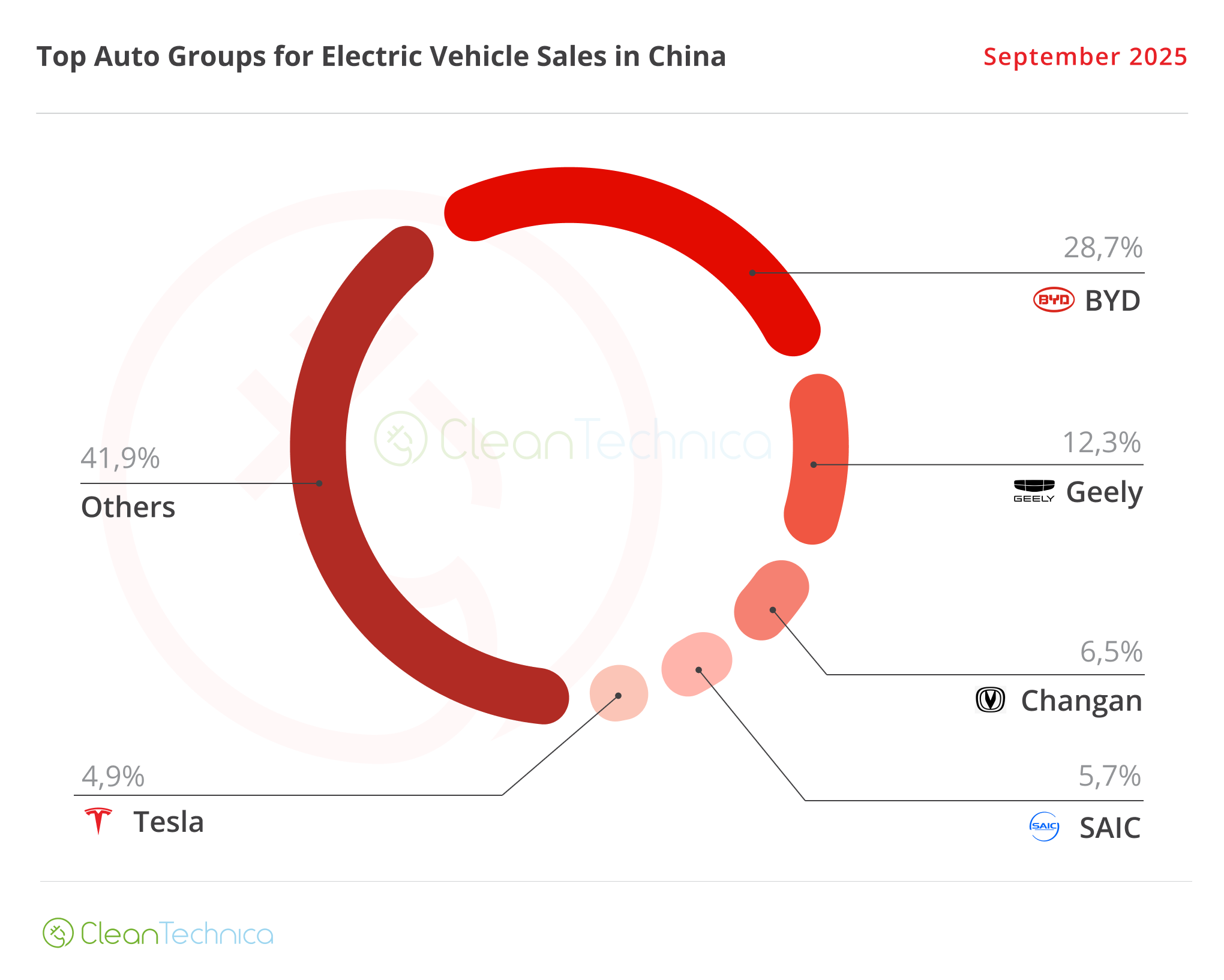

Auto Groups Selling the Most Electric Vehicles in China

Looking at OEMs/automotive groups/alliances, BYD is comfortably leading, with 28.7% share of the market.

#2 Geely is a distant runner-up, with 12.3% share, but with #3 Changan having just 6.5% share, Geely is safe in the runner-up position.

As for #4 SAIC (5.7%), it is stable and should remain in 4th until the end of the year.

Tesla (4.9%, up 0.1% in September) remained in 5th, but Tesla’s 2024 #3 spot in the OEM ranking seems almost impossible to achieve, and it could even be the case that there will be no Tesla on any podium — models, brands, or OEMs — for the first time since 2019!

Fortunately for the US brand, #6 Chery (4.1%) is too far behind to become a real threat to its #5 position.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy