They include a projected rise in non-OPEC production, in addition to Russia’s need to boost supply to increase revenue and the potential for oil demand to slow given already-high interest rates in major Western economies.

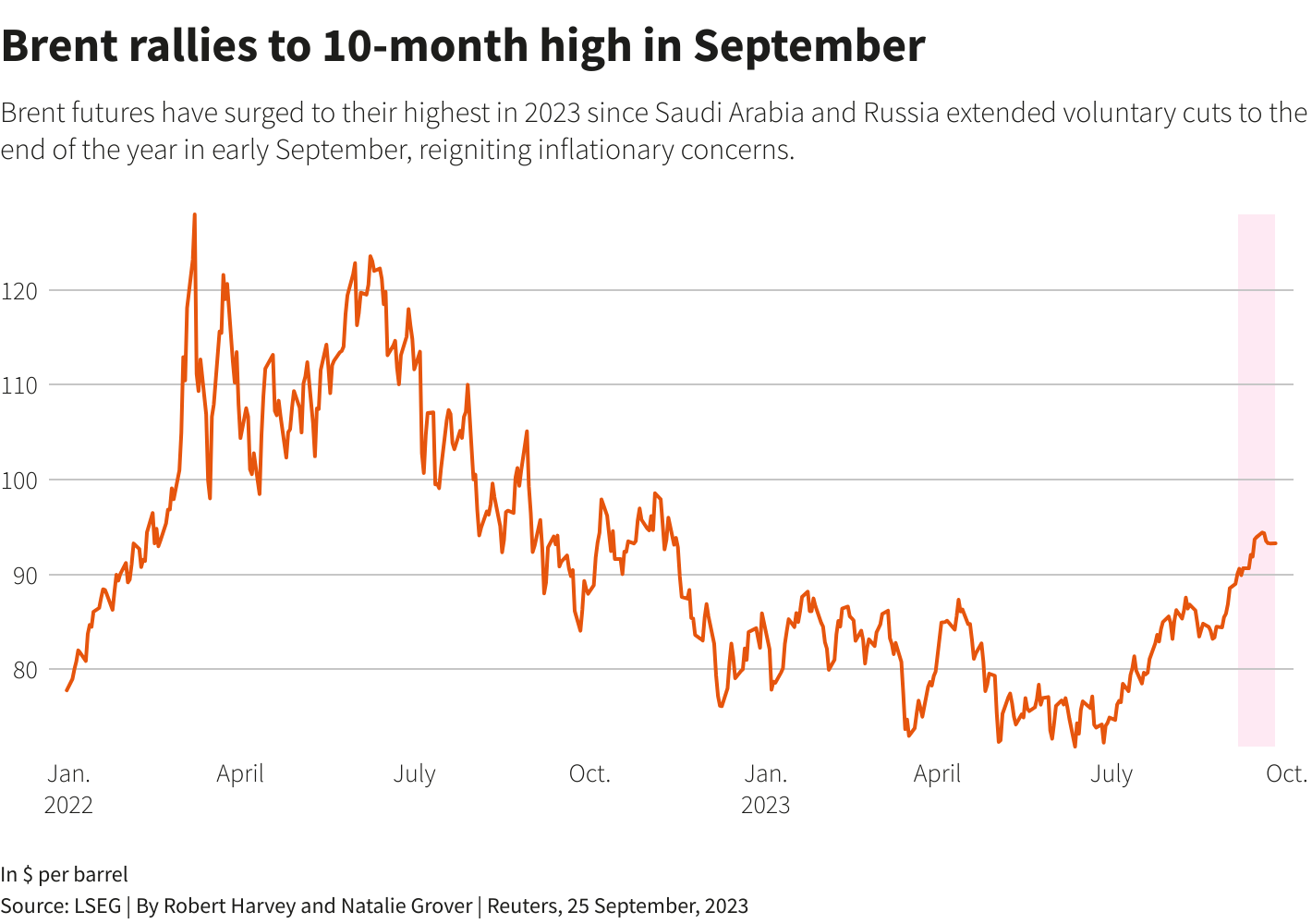

Brent peaked at nearly $96 a barrel last week and U.S. West Texas Intermediate hit $91 a barrel for the first time in 2023.

A growing number of analysts forecast Brent will surpass $100 a barrel this year as demand rises, supply is constrained, and stocks of fuel and crude are relatively low.

Retail fuel prices in the U.S. and Europe have risen to multi-month highs as crude prices have rallied.

“If energy prices increase and stay high, that’ll have an effect on spending, and it may have an effect on consumer expectations for inflation, things like that. That’s just things that we have to monitor,” U.S. Federal Reserve chair Jerome Powell said last week.

Morgan Stanley analysts echoed the sentiment, that although central bankers may be wary of rising oil prices, a rally “must be sustained for some time to have a greater, more durable effect on core prices”.

A long run above $100 could increase inflationary concerns for governments that have hiked interest rates to combat rising prices as their economies emerged from the COVID-19 pandemic.

Non-OPEC+ output growth could calm any rally. Goldman Sachs sees non-OPEC+ supply rising by 1.1 million barrels per day (bpd) by next year, while the International Energy Agency has forecast growth of 1.3 million bpd.

Brazil, Guyana and the United States are among the countries expected to increase output.

The return to investment in and growth from offshore production also make a long-term rally less likely, Goldman analysts said, adding “most of the rally is behind us”.

High interest rates are already curbing demand across Western economies, including for oil.

Geopolitical considerations may also complicate decisions around how long OPEC+ can sustain voluntary cuts.

Supply curbs implemented by the Organization of the Petroleum Exporting Countries and allies (OPEC+), in particular a combined 1.3 million bpd voluntary cut from Russia and Saudi Arabia until the end of 2023, have played a leading role in pushing futures prices to 10-month highs.

But Russia may be unable to curb exports for a protracted period given the toll of the war in Ukraine on its finances, PVM’s Tamas Varga said.

For OPEC’s de facto leader Saudi Arabia, the perennial issue of achieving prices high enough to reward producers without pushing the market to a level that destroys demand and tips the economy into recession is likely to resurface in policy considerations, analysts said.

“I’m not sure there’s much economic sense in tipping the global economy into recession if OPEC+ persevered with these cuts, which makes me question how high the price will go and how sustainable it will be,” OANDA analyst Craig Erlam said.

RATES AND RALLY

After months of aggressive rate hikes to tackle stubborn inflation, policymakers in the U.S. and Europe have signalled hikes are at or near their peak.

The U.S. Federal Reserve on Wednesday pressed pause on interest rates, but did not rule out one more hike this year.

Governments may look at fiscal measures such as cutting fuel duties as a more direct way of limiting the impact of high pump prices, HSBC analyst Ajay Parmar told Reuters.

Gasoline prices breached the psychologically significant $4 a gallon mark for the first time since last October earlier this month, as retail diesel prices hit their highest since December, according to Energy Information Administration (EIA) estimates.

The fuel price rise is a sensitive issue in the run-up to the U.S. presidential election.

President Joe Biden has already promised to cut prices, though has not said how, and in the short term the impact of autumn refinery maintenance on supplies could keep prices high.

Restrictions on fuel exports and increasing refinery utilisation are potential options. The U.S. government already drew on crude reserves last year to add supply to the market.

Diesel and gasoline pump prices in the Euro zone and Britain have also hit multi-month highs, prompting the latest round of government action.

France this week lifted a decades-old ban on retailers selling road fuel below cost to combat inflation.

Energy major TotalEnergies has also agreed to extend its 1.99 euros per litre cap on fuel to the end of 2023.

And in Britain, which is expected to see a general election next year, politicians are likely to hesitate to withdraw a five pence per litre fuel duty cut in place since March last year, executive director of the Petrol Retailers Association Gordon Balmer said.

Reporting by Natalie Grover, Robert Harvey and Mark John in London; additional reporting by Balazs Koranyi in Frankfurt and Dan Burns in New York; Editing by Simon Webb and Barbara Lewis

Share This: