Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

The nation is falling further behind in addressing risk to the most repeatedly flooded homes.

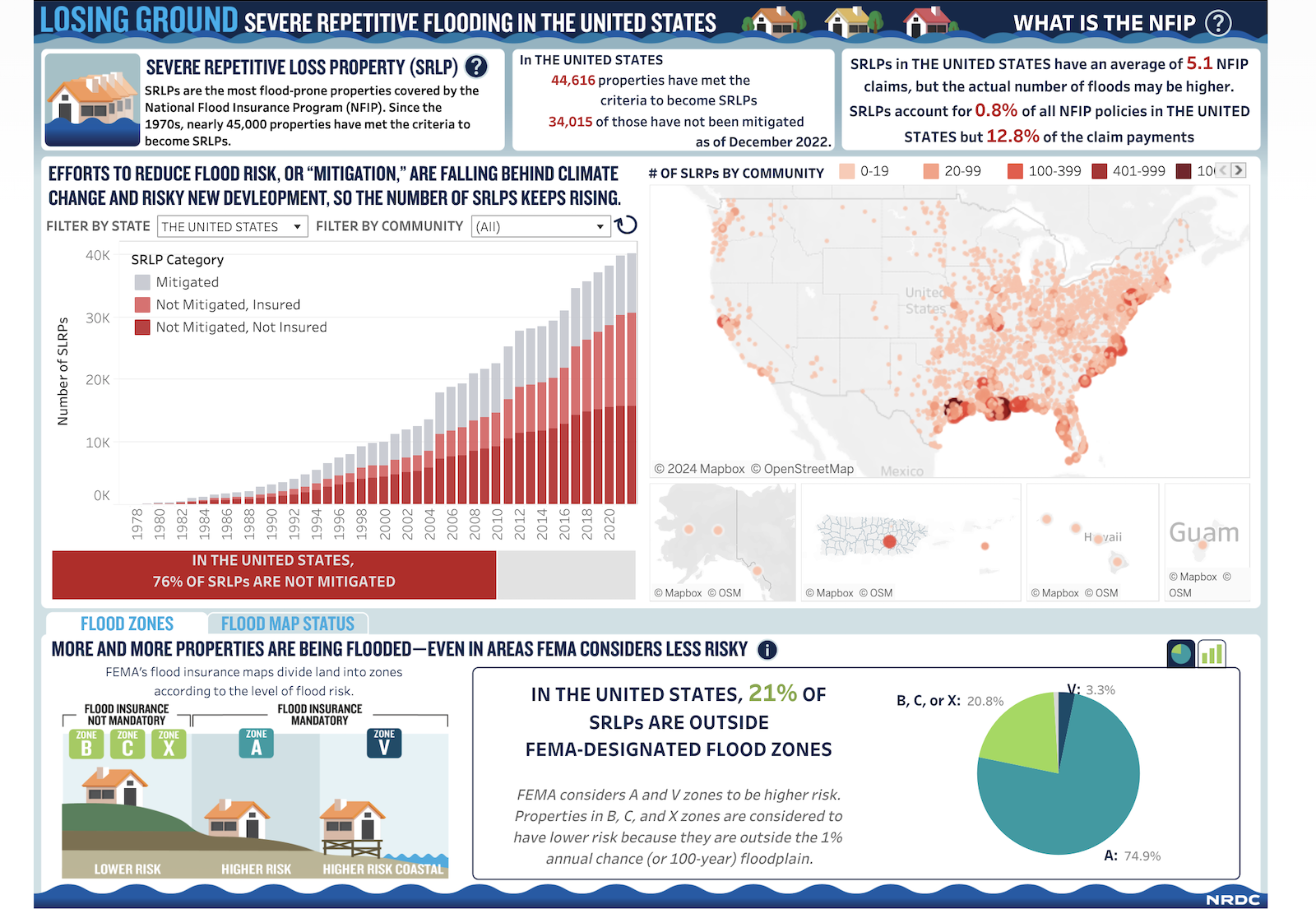

The list of the nation’s most flood-prone homes is growing longer. NRDC’s updated Losing Ground dashboard now includes data on severe repetitive loss properties (SRLPs) from the inception of the National Flood Insurance Program (NFIP) through late 2022. The new information shows a worrying trend: across the country, more properties are being added to the list of SRLPs than are having their risk addressed through hazard mitigation.

Previously, NRDC obtained data from the Federal Emergency Management Agency (FEMA) on all SRLPs in the United States as of May 31, 2018, and used that to create the first version of our Losing Ground dashboard. As of early 2024, the dashboard now contains data through December 11, 2022. Losing Ground shows the number of SRLPs in each state and NFIP participating community, as well as trends in SRLPs over time: how many properties qualified as SRLPs; how many were mitigated; and how many dropped insurance without mitigation.

Access the dashboard and additional information here: https://www.nrdc.org/resources/losing-ground-flood-visualization-tool.

Use the filters at the top of the bar chart to select your state or NFIP participating community, or hover over the left side of the map to see a menu that will let you zoom and pan to a specific location. The main bar chart shows the timeline of mitigated, insured, and uninsured SRLPs. The tabs at the bottom of the dashboard show the NFIP flood zones of SRLPs in the selected location, as well whether the SRLPs predate or postdate local flood maps—in other words, whether they were subject to floodplain management regulations when they were built.

The NFIP was created in 1968 to provide affordable insurance against flood risk and decrease overall risk across the country. Since then, nearly 45,000 properties have met the criteria to become what the program refers to as Severe Repetitive Loss Properties. These properties, the most flood-prone structures insured under the NFIP, have flooded about five times each, on average. Since NRDC published the original version of the Losing Ground dashboard, the total number of SRLPs has increased by over 7,000, but only an additional 630 have received mitigation assistance to reduce their vulnerability to future floods.

Policy gaps at the federal, state, and local level are all contributing to this lack of progress. And addressing these gaps is critical as climate change increases flood risk, putting the households and communities that can least afford it in greater physical and financial danger. The updated dataset illustrates three key points:

The nation is falling even further behind in addressing flood risk to the most repeatedly flooded properties: only 24% of SRLPs have seen action to mitigate their flood risk, down from 27% in 2018. In flood-prone states like South Carolina, Michigan, and Rhode Island, less than 10% of SRLPs have been mitigated. In fact, over the history of the NFIP, more SRLPs have become uninsured (for example, because the homeowner can no longer afford insurance) than have received mitigation. In West Virginia, for example, 73% of SRLPs are uninsured and unmitigated.

The states with the most SRLPs are:

- Louisiana: 9,935 SRLPs (6,599 not mitigated)

- Texas: 9,381 SRLPs (7,460 not mitigated)

- New Jersey: 4,164 SRLPs (3,161 not mitigated)

- Florida: 3,550 (2,821 not mitigated)

- New York: 2,213 (1,966 not mitigated)

More properties are flooding repeatedly in supposedly low-risk areas: 21% of SRLPs are outside of areas that FEMA designates as higher risk of flooding, up from 19% in 2018. FEMA’s flood maps divide land into zones according to the level of flood risk. Locations with a 1% chance of flooding in a given year are considered to be in the “special flood hazard area,” which is sometimes referred to as the 100-year floodplain. Most SRLPs are located in these higher-risk areas, but some communities are seeing more flooding in areas outside the mapped floodplain. For example, in Texas, 43% of SRLPs are located outside the special flood hazard area, suggesting that the state’s flood maps are not accurately capturing current flood risk.

The states with the highest proportion of insured, unmitigated SRLPs outside the special flood hazard area (among states with more than 50 SRLPs) are:

- Texas: 43% outside the SFHA

- Rhode Island: 28% outside the SFHA

- Tennessee: 28% outside the SFHA

- West Virginia: 27% outside the SFHA

- Georgia: 27% outside the SFHA

Newer properties, which should be built to higher standards, are increasingly flood prone: 18% of SRLPs post-date FEMA flood insurance rate maps (FIRMs), up from 14% in 2018. On average, we expect these “post-FIRM” properties, built after flood risks were mapped and floodplain management standards were required, to have lower risk than their “pre-FIRM” counterparts. Disproportionate flood damages among post-FIRM properties may point to outdated standards and increased risky construction in flood-prone areas.

The states with the highest proportion of insured, unmitigated SRLPs that are post-FIRM (among states with more than 50 SRLPs) are:

- Alabama: 61% post-FIRM

- Mississippi: 51% post-FIRM

- North Carolina: 35% post-FIRM

- South Carolina: 31% post-FIRM

- Arkansas: 29% post-FIRM

Increasing numbers of SRLPs without mitigation is a symptom of a multi-faceted problem, and it requires action across levels of government. We need Congressional action to reauthorize and reform the NFIP, updated FEMA regulations for flood risk maps and floodplain development standards, federal hazard mitigation funding that’s accessible to lower-capacity communities, state policies that give residents a right to know their flood risk, and strong local building and zoning codes to stop putting people in harm’s way.

SRLPs represent the tip of the iceberg when it comes to chronic flooding in the United States. Because all SRLPs have been insured by the NFIP, the dataset doesn’t include properties that have never had insurance coverage. This undoubtedly leaves out large numbers of homes and businesses, especially the homes of lower-income families who are less likely to have flood insurance. But steps to reduce flood risk will not only benefit NFIP policyholders—they are essential to creating a more flood-resilient nation overall.

Special thanks to Susan Lee, Data Analysis and Visualization Specialist in NRDC’s Science Office, for her technical and design work!

Originally published on the NRDC Expert Blog. By Anna Weber

Featured image by Arek Socha from Pixabay

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Our Latest EVObsession Video

I don’t like paywalls. You don’t like paywalls. Who likes paywalls? Here at CleanTechnica, we implemented a limited paywall for a while, but it always felt wrong — and it was always tough to decide what we should put behind there. In theory, your most exclusive and best content goes behind a paywall. But then fewer people read it!! So, we’ve decided to completely nix paywalls here at CleanTechnica. But…

Thank you!

CleanTechnica uses affiliate links. See our policy here.