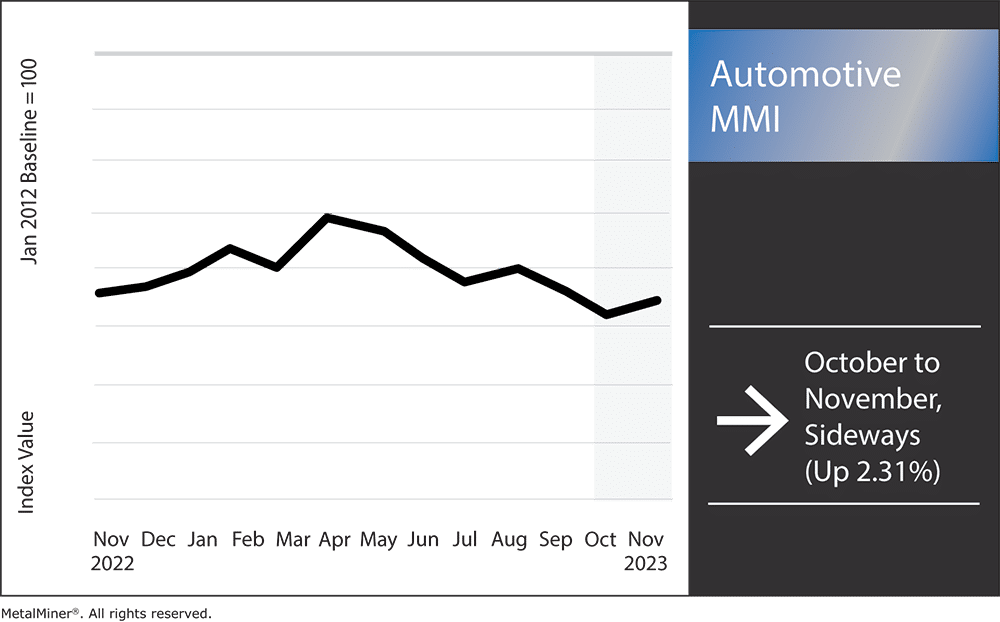

The Automotive MMI (Monthly Metals Index) moved sideways month-over-month, rising in price by just 2.31%. Save for hot-dipped galvanized steel, most parts of the index also traded sideways, mainly due to a lack of strong bullish or bearish pressure. Hot-dipped galvanized proved the only outlier due to steel corporations hiking prices. However, the main headline in US steel news remains the potential end of the UAW strike.

UAW Strike: An End in Sight

After a seven week strike, United Auto Workers (UAW) union and the Big Three automakers recently reached agreements. All three automakers— General Motors, Ford, and Stellantis — achieved tentative agreements with the UAW on October 30, 2023. With record-breaking pay and benefit increases, this essentially puts an end to the first strike against Detroit’s “Big Three.”

Proposed salary increases over the 5-year term, better cost-of-living adjustment offers, and higher 401(k) retirement contributions are all included in the agreements. The terms also bring back a three-year salary progression and cost of living allowances (COLA). That said, the UAW National GM Council still needs to review the deal before submitting it to the membership for a vote.

Meanwhile, estimates indicate that the strike caused billions of dollars in losses to the US economy. In fact, according to the most recent figures from Michigan research firm Anderson Economic Group, the auto industry alone has lost more than $9.3 billion as a result of the strike.

The estimate also indicates that workers lost $579 million in pay, while manufacturers lost $2.68 billion overall. On the other hand, suppliers lost $1.6 billion on their own, while dealers and customers lost $1.26 billion.

Stay up on the latest US steel news. Subscribe to MetalMiner’s free weekly newsletter.

US Steel News: Steel Prices and Demand Impacted by Strike Aftermath

The Wall Street Journal reports that the US steel sector suffered greatly due to the UAW strike, with significant declines in demand, sales, and pricing. During the summer, as a UAW strike became increasingly possible, steel purchases by users connected to the car industry began declining quickly. Indeed, S&P estimates that the strike prevented the production of 6,030 automobiles per day, equivalent to roughly 5,982 tons of steel.

US steel news sources indicate that the American Steel Index dropped 5.92% last month. Meanwhile, spot prices for benchmark coiled sheet steel (a material typically used to build car parts) dropped 40% since April. Currently, the average vehicle’s body, mufflers, exhaust pipes, and other components are still mostly made of steel, which accounts for roughly 54% of the total material content.

Anderson Economic Group’s aforementioned report indicates that the Big Three automakers suffered a loss of $1.12 billion in the first two weeks of the strike alone. When the strike hit the two-week mark, GM estimated a total loss of roughly $200 million. That said, the steel market had been anticipating the strike for most of 2023. This also drove down steel prices, which were already in recovery from poor demand during the pandemic.

Harness data to forge a path to success in steel sourcing using MetalMiner Insights’ powerful long-term and short-term steel forecasting. Ready to learn more?

Consumer Vehicle Increased Despite Strike

In other US steel news, US car sales continue to rise steadily despite the UAW strike. Though the strike proved the longest US auto strike in a quarter of a century, consumer demand remained strong throughout.

Cox Automotive predicted that the number of new car sales in the US would increase about 4% between October 2022 and October 2023, with yearly vehicle sales in October likely to reach close to 15.8 million. This is up 1.1 million from the 14.7 million seen in October of 2022.

Increasing inventory levels throughout the industry proved a major factor supporting the strength of new car sales. In fact, estimates indicate that the industry-wide new vehicle inventory in the US came in at 2.3 million units. This is a significant increase from the 2.1 million recorded in mid-September when the strike began. It is also well above the estimated 1.5 million for mid-October 2022, despite the ongoing UAW strike slowing production across the major Detroit-based automakers.

The auto industry also benefited from increased demand for personal transportation and better supply, with sales of new cars increasing above the market’s supply constraints in the previous year. It seems the need and ability to purchase automobiles still present themselves in sufficient numbers of people and businesses, which ultimately helped to support the overall sales rebound.

US steel news moves fast! MetalMiner’s MMI report includes 10 metal price reports and can serve as an economic indicator for steel contracting, price forecasting, and predictive analytics. Sign up here.

Automotive MMI: Notable Price Trends

- Chinese lead moved sideways, dropping by a slight 1.35%. Prices at the month’s start sat at $2,224.55 per metric ton.

- Hot-dipped galvanized steel enjoyed a steep 11.24% rise, bringing prices to $1,039 per short ton.

- Finally, Korean aluminum 5052 coil premium over 1050 saw a modest increase of 1.32%, and thus maintained a sideways trend month-on-month. This left prices at $3.85 per kilogram.