Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

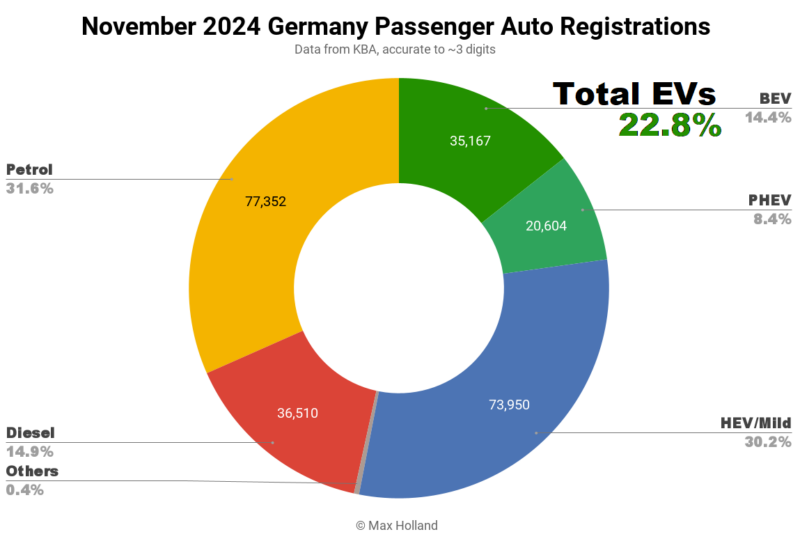

November saw plugin EVs at 22.8% share in Germany, down from 25.7% year on year. BEV sales were down YoY, though from an elevated baseline, while PHEV sales were up 14%. November’s overall auto volume was 244,544 units, roughly flat YoY. The best selling BEV in November was again the Skoda Enyaq, for the third month running.

November’s sales saw combined EVs at 22.8% share in Germany, with full electrics (BEVs) at 14.4% share, and plugin hybrids (PHEVs) at 8.4%. These compare with YoY figures of 25.7% combined, 18.3% BEV and 7.4% PHEV.

The YoY baseline for BEV sales (November 2023) was higher than usual due to a pull-forward ahead of the looming scheduled reduction in the BEV purchase incentive from January 1st 2024. As we now know, the incentive was in fact not simply reduced from January 1st, but instead was summarily cancelled without any notice, in mid December 2023. That baseline pull-forward makes the YoY comparison look particularly weak.

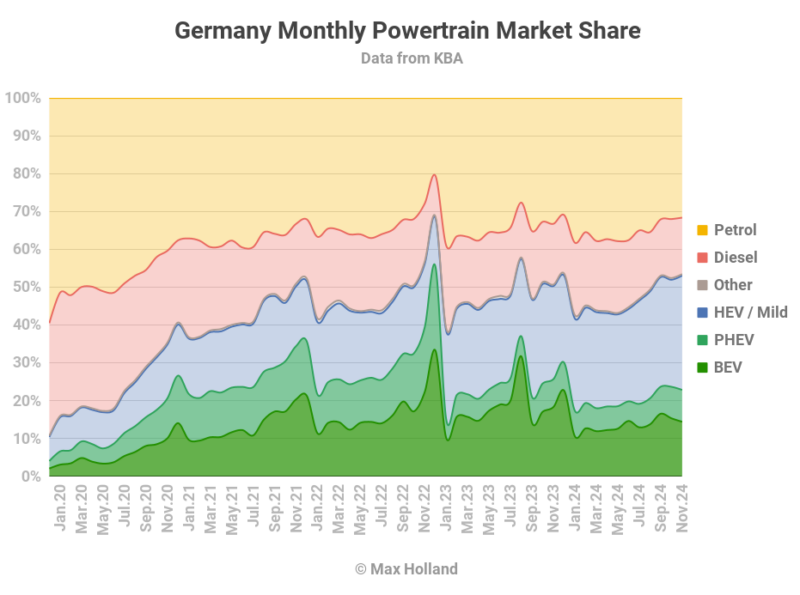

Nevertheless – even putting aside the YoY comparison – BEV sales and market share would typically be increasing slightly as we approach the end of a year, when manufacturers look to improve their fleet-average vehicle emissions ahead of the end-of-December deadline. This year, however, there’s no tightening of emission requirements, so no such push by auto markers – if anything, they are motivated to slow down new BEV deliveries and drag them into 2025, when tighter emissions rules do come into effect.

Simultaneously, the demand side remains weighed down by a weak consumer economy, and BEVs being still overpriced relative to other powertrains. The tighter 2025 emission rules are the main reason why European legacy brands are only now — at the end of 2024 — starting to launch their simple and more affordable BEVs, and are planning to increase their volume in the coming few months, to improve their BEV sales in 2025. This timing is not a coincidence.

On the plus side, there was a decent increase in PHEV volumes YoY, thanks to the new generation of models which now typically have over 50 miles of all electric range. With plugless HEV sales also growing, combustion-only share declined YoY (though less so than BEV share).

The slow but steady decline in diesel sales saw their share reach 14.9% in November, down from 16.1% YoY.

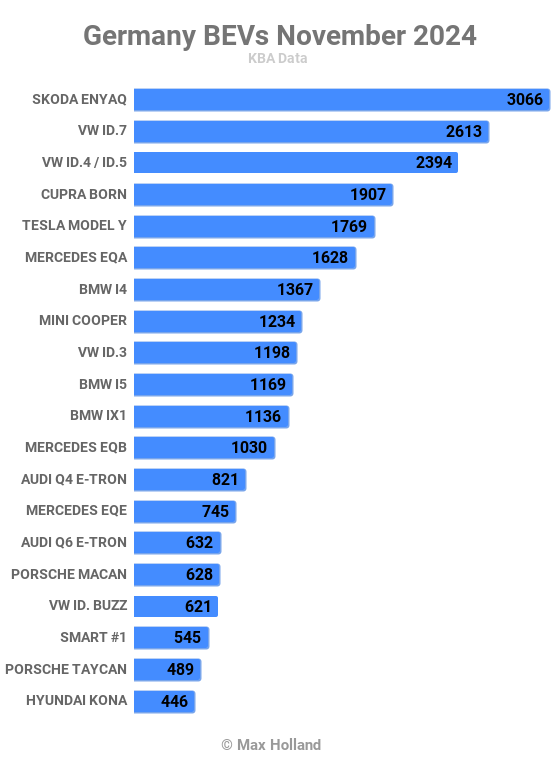

Best Selling BEVs

For the third month in a row the Skoda Enyaq took the top spot in the BEV model rankings, with 3,066 units in November.

In second place was the Volkswagen ID.7, with 2,613 units, and the Volkswagen ID.4/ID.5 came in third, with 2,394 units.

With the Cupra Born in 4th spot, November was another good result in its home market for Volkswagen Group, and a rare repeat of the same domination of the top 4 spots (with the same 4 models) seen in October.

Volkswagen Group grabbing the top 4 spots has only happened once before, in April of this year. Usually the Tesla Model Y spoils the party by appearing somewhere in the top 3, but was in 5th spot in November.

The overall top 20 ranks did not see any huge surprises, with almost all models being close to their recent average volumes, and the only newcomers to the top 20 being the Audi Q6 and Porsche Macan (both of which were largely expected).

October’s new intake of BEV models – the Kia EV3, Ford Capri, Citroen e-C3, and Volvo EX90 – all grew further in November, with the Kia and Ford the strongest, up to positions 30, and 51, respectively.

More BEV model debutantes arrived in November. The highest volume model – at 103 units – was the new Leapmotor T03, a small-and-affordable hatchback which has finally arrived in Europe thanks to a partnership between Stellantis and Chinese EV startup Leapmotor (founded in 2015). For the Leapmotor T03’s basic specs, see my report on China’s affordable BEVs from early this year. It is priced from €18,900 in Germany, with a 37.3 kWh (gross) battery.

Leapmotor didn’t stop there, the brand also launched the C10, a mid-large SUV (4,739 mm), which registered a modest 9 initial units. The C10 is priced from €36,400 for the 66 kWh (usable) battery variant.

The new Skoda Elroq also launched in November, with 46 units registered. The Elroq is essentially a shortened version of the Enyaq, with a length of 4,488 mm vs the Enyaq’s 4,648 mm. It has the same wheelbase, and shares the same doors, front wings and much of the interior, but the rear is foreshortened, with less of an overhang. The entry price for the Skoda Elroq’s 52 kWh (usable) variant is €33,900 in Germany.

Finally, the BYD Sealion SUV also launched in November, with 50 units. The Sealion is BYD’s new mid-large SUV Coupe, with a length of 4,830 mm. For an overview of the BYD Sealion, see the recent Norway report. The Sealion is priced from €47,990 in Germany, for a well specified “entry” 91.3 kWh variant.

We will keep an eye on these newcomers to see how they get on in the coming months.

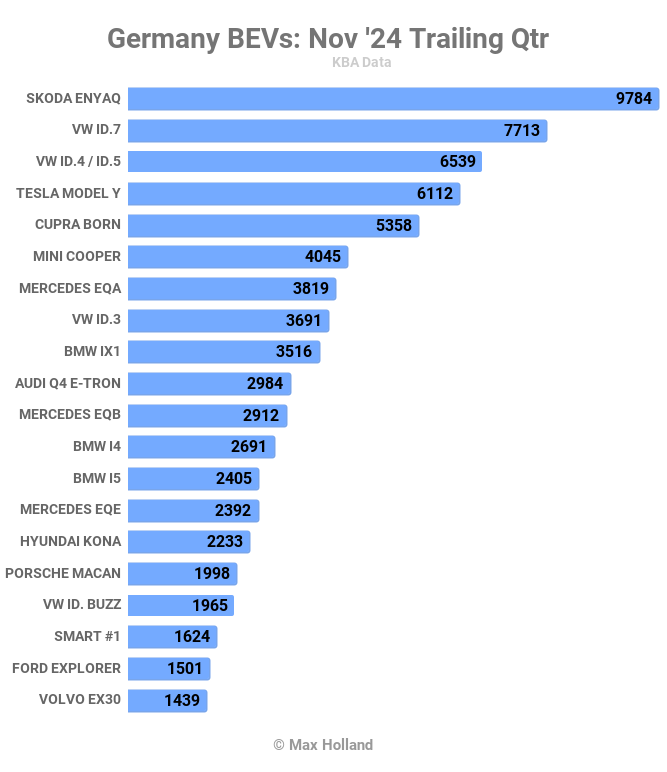

Let’s now check in with the 3-month ranking:

Thanks to a couple of strong months, Volkswagen Group brands now hold the top 3 spots, with the same three models as in the November monthly ranking — the Skoda Enyaq, Volkswagen ID.7, and Volkswagen ID.4 / ID.5.

There are no great surprises elsewhere in the top 20, except for the progress further back by two newcomers. The Porsche Macan has been a great hit in its short time on the market, climbing to 16th spot after just 4 months on sale. This is particularly impressive given the high price point and the fact that the very similar (and also impressive) Audi Q6 e-tron is available for a lower price.

Further back, in 19th spot, the Ford Explorer has also done well, likewise after just 4 months of volume sales. Let’s see if these two new models remain a fixture in the top 20 over the medium-term.

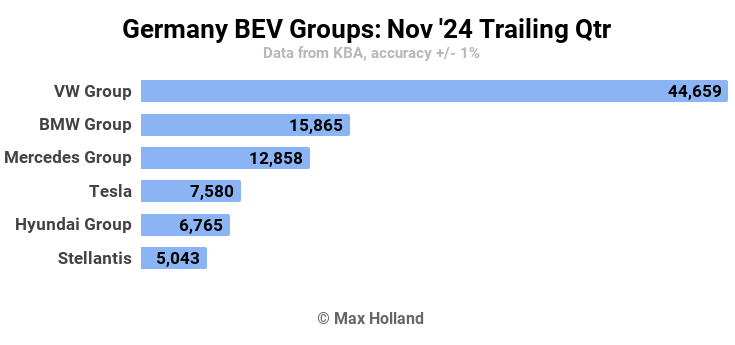

Let’s briefly check up on the manufacturing group rankings:

Volkswagen Group’s strong home lead is clear to see, with near 45,000 sales over the past 3 months, representing an impressive 42.8% of Germany’s overall BEV market. This is a great improvement over 33.9% share in the prior 3-month period (June to August).

The overall ranking of the top 6 groups hasn’t changed since August, but all of the home teams pulled ahead compared to 3 months prior. BMW, in second, gained 1.5% additional share to reach 15.2%, while Mercedes, in third, gained 2.3% share to reach 12.3%. Tesla, Hyundai Motor Group, and Stellantis, each lost a couple of % of market share, though maintained their relative ranking.

Outlook

As mentioned above, one of the main reasons why Germany’s BEV share is so weak, is the poor state of the country’s wider economy. The latest YoY GDP figures from Q3 2024 were recently recalculated and tweaked downwards to negative 0.3% (from their 0.2% previous estimate).

Headline inflation kept on an upward trend, at 2.2% in November, from 2% in October. ECB interest rates are still at 3.4%. Manufacturing PMI did not improve across November, and remains weak at (a revised) 43.0 points, which is flat from October.

As discussed above, we will now have to wait until 2025 to see if the BEV market can get back to a growth trajectory after a miserable 2024 which has suffered from a weak economy, overpriced BEVs, and few-to-no affordable options. At least the tighter emissions regulations of 2025 are now forcing manufacturers to offer more affordable models, to up their volumes, so let’s see if Germany gets back on track.

What are your thoughts for Germany’s prospects for 2025? What models are you looking out for? Please share your thoughts in the comments section below.

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy