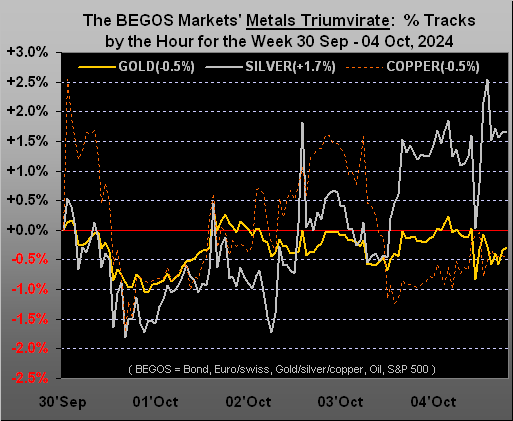

Welcome to edition “Triple-Seven” of The Gold Update, wherein we find the yellow metal having settled yesterday (Friday) at 2673, a -0.3% loss (-8 points) for the week.

Silver however for the same stint settled at 32.45, a +1.7% weekly gain (+0.53 points), achieving en route a nearly 12-year high of 33.23, such level having not traded since 13 December 2012. Not even cajoling Cousin Copper could keep sweet Sister Silver down. ‘Twas a beautiful thing as we here see per the cumulative percentage tracks of the BEGOS Markets’ “Metals Triumvirate” by the hour across this past week:

Silver’s sterling week (whilst Gold was essentially asleep) was enough to bring the (albeit still excessive) Gold/Silver ratio down to 82.4x, its lowest closing reading since 23 July. Moreover, year-to-date expanded Silver’s leading position of the BEGOS Markets, the white metal now with a gain of +35.0%, (followed by Gold at +29.0% and then the S&P 500 +20.6% to round out the podium).

Specific to Gold and the murderous Mid-East mayhem, we were yet again reminded that the yellow metal’s swift upside reaction to geo-political barbarism was at best short-lived, price from late Monday into Tuesday being boosted from 2646 to 2695 only to then see it erode away into week’s end. We’ve written rather extensively on Gold’s “momentary” spikes over geo-political jitters, price then regularly receding.

That in turn reminds us of Gold’s most foundational element of valuation: ’tis not fearful events nor extravagant wedding seasons, et alia. Rather ’tis the debasement of currency that gives lasting value to Gold. And as our opening Gold Scoreboard shows, by Dollar debasement (even as adjusted to the creeping increase in the supply of Gold itself), the yellow metal today “ought be” fetching $3,741/oz. So yes, for you WestPalmBeachers down there, priced today at $2,673/oz Gold remains cheap; and Silver still super cheap given the century-to-date average Gold/Silver ratio is but 68.5x.

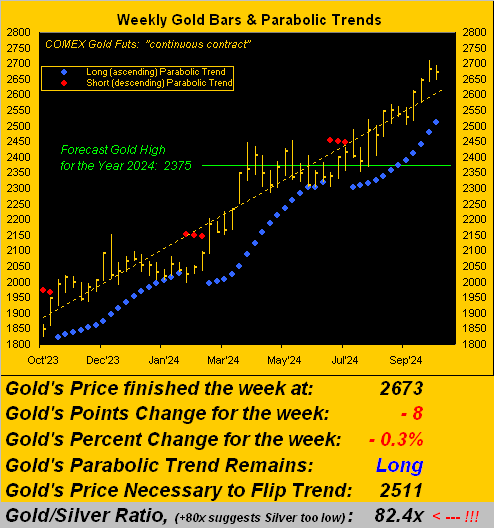

Still in light of Silver’s robust week, Gold stand by rather idly as we here see by the weekly bars from one year ago-to-date. the blue-dotted parabolic Long trend nonetheless continuing to ascend:

Regardless, we’ve this ongoing reminder from the “Nothing Moves in a Straight Line Dept.” that Gold near-term is overvalued vis-à-vis its smooth valuation line (which is different from the broad-term Scoreboard value). Here, the smooth line sets a value for Gold based on its movement relative to those of the five primary BEGOS Markets, namely the Bond, Euro, Gold, Oil and S&P 500. Thus from the website comes that updated view, by which one ought anticipate price reverting to the smooth line which fortunately itself is on the rise and therefore, in part, supportive of Gold’s recent rally:

“Your chart says ‘excessive’, but what happened to your ‘Stock Market Warning’ mmb?“

To be sure, Squire, we issued said “Warning” a week ago. Instead, the S&P 500 sported a +0.2% gain for the week. ‘Tis the way ’tis as The Investing Age of Stoopid blissfully rolls along. The mighty Index today stands at 5751, a mere -16 points below its 5767 all-time high, with FinMedia reports for 6000. That is just another +4.3% up from here. (Note for those of you scoring at home: at 6000, the “live” P/E of the S&P would be 44.4x; ‘course, earnings in the modern investing era have becoming meaningless, so ’tis all good, even as the “non-event” Q3 Earnings Season commences on Monday).

Indeed speaking of “good”, as we work toward the Economic Barometer, how about that StateSide jobs report for September, courtesy of the Department of Labor Statistics? The net “creation” of 254,000 Non-Farm Payrolls was hailed amongst the FinMedia as (ready?) “Blockbuster” and even more superlatively as a “Supernova”. Why, we ourselves were so excited over this apparently history-breaking news that we decided (as you know is our wont) to do the math. And here’s what we found:

- Century-to-date (i.e. from January 2001), Friday’s monthly report was No. 285, for which such amazing job creation ranked as (ready?) 50th-best. One strains to recall what adjectives were used for the prior 49 reports that were even better.

But yes, we get it: ’tis election season and as the economy’s state ultimately redounds to the Executive Branch, “Labor” need ensure its survey results generate energized levels of electoral enthusiasm. Cue The Cars from ’84:  “Uh oh, it’s magic” And as an aside, specific to September’s private sector employment, “Labor” recorded a +78% month-over-month improvement whereas ADP’s report was only half that at +39% … (just one of those things that makes you go “hmmmmm…”)

“Uh oh, it’s magic” And as an aside, specific to September’s private sector employment, “Labor” recorded a +78% month-over-month improvement whereas ADP’s report was only half that at +39% … (just one of those things that makes you go “hmmmmm…”)

Either way, we’re told the economy is humming right along, some indeed invoking the “Goldilocks” descriptor. Really, does it get any better than the following?

‘Course in the midst of all this economic euphoria come the bits from the “You’re Not Supposed to Say That Dept.”, which from this past week include ongoing net contraction for September in both the Chicago Purchasing Managers’ and Institute for Supply Management’s Manufacturing Indices, a slowing in Hourly Earnings and the number worked thereto, a pickup in the prior week’s Initial Jobless Claims, and actual shrinkage in August’s Factory Orders. But “Mum’s the word, Mum.” Right.

As aforeshown, getting it right this past week was Silver, such that we’ll lead the two-panel displays this time ’round with the white metal. Below on the left are her daily bars from three months ago-to-date; but be wary of her “Baby Blues” of day-to-day trend consistency, as upon their breaching below the +80% axis, one ought look to lower price levels. Then on the right we’ve Silver’s 10-day Market Profile with the most dominantly-traded prices by volume tightly nested as labeled:

Too, we’ve the like drill for Gold. Note on the left the “Baby Blues” similarly curling to the downside, whilst on the right the three labeled dominant prices are a bit more spread out than are those for Silver:

We shut down for this week with a heads-up for next week. Our 778th consecutive Saturday edition of The Gold Update is to be composed from a remote, undisclosed, rural location in easternmost England, an area sufficiently primitive that in lieu of digital internet connectivity we must be reliant upon analog telegraph. Indeed, next week’s piece — to literally go “out on the wire” (as dear old Grandpa used to say) from one telephone pole to the next and right ’round the world — shall be quite brief and perhaps even graphics-less. But having never missed penning a Saturday missive across these 15 years, the show must go on, just as does Gold being true money these 5,000 years!

So whilst Tut himself may be out on the town, again we’ll be hunkered well down close to the ground our next missive ’round!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

*******