Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

Plugin vehicles are all the rage in the Chinese auto market, with plugins scoring 876,000 sales (in a 1.76-million-unit overall market). That’s up 23% year over year (YoY).

Looking deeper at the numbers, growth basically came from the PHEV side — BEVs were up by just 1% in June, while PHEVs jumped 70% in the same period, to a record 393,000 units. Breaking down plugin sales by powertrain, BEVs had 55% of sales, or some 482,500 units, below this year’s average of 59%. Clearly, there’s rising popularity of plugin hybrids in this market.

The year-to-date (YTD) tally is around 4.3 million units, a significant rise over the 3.3 million units in the same period of 2023.

Share-wise, June saw plugin vehicles hit a record 49.9% market share! Full electrics (BEVs) alone accounted for 28% of the country’s auto sales. This pulled the 2024 share to 43% (25% BEV), and with the market still with plenty of room for growth, the year should end at around 50%.

Comparing this result with June 2023, at the time, the plugin share was 35% (24% BEV), which means that, while BEVs are experiencing moderate growth (24% vs. 28%), the PHEV share is growing faster (11% vs. 22%). At this pace, we should have the Chinese market fully electrified around 2030, if not sooner.

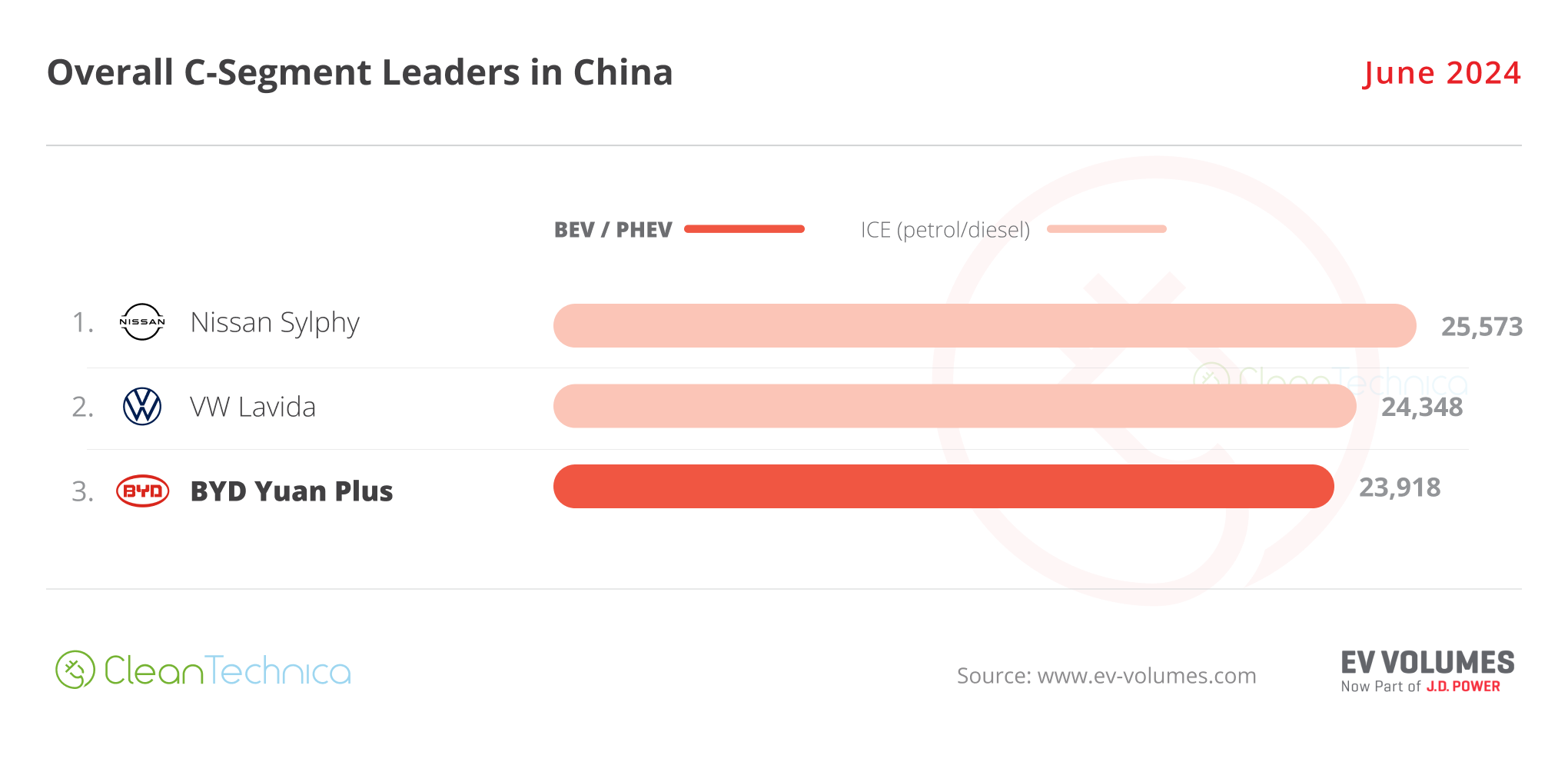

The podium was 100% plugins, with the Tesla Model Y being the best selling non-BYD model, in 2nd. The best selling ICE model was the Nissan Sylphy, in 5th, with some to 26,000 units sold. The Japanese model was the first of four ICE models in the top 10.

Benefitting from its recent War on ICE, BYD placed four models in the overall top 10! Price cuts from the Shenzhen make are pressuring not only the ICE competition, but also its plugin adversaries….

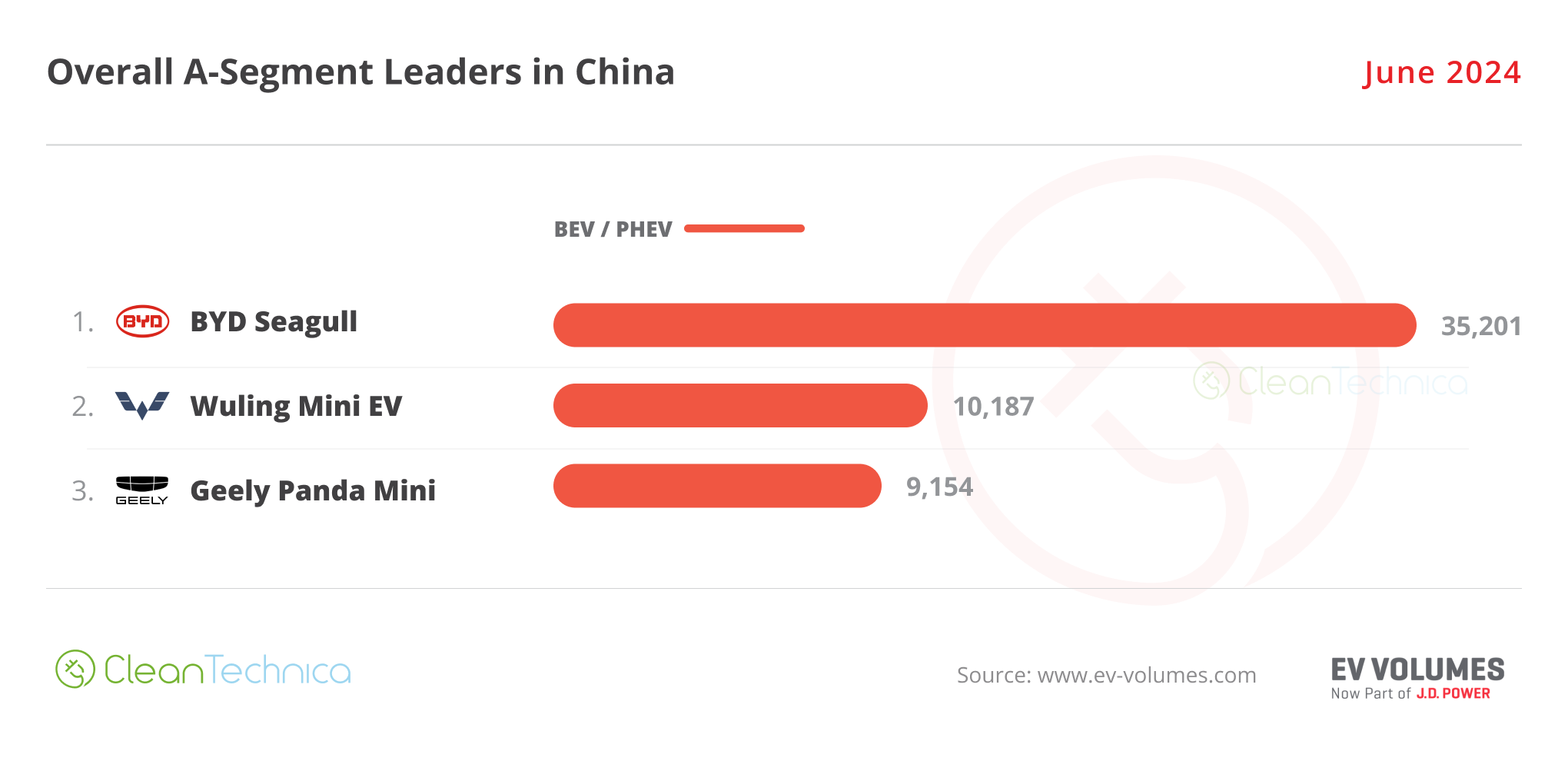

Looking at several categories, all the vehicle segments have 100% PEV podiums with the exception of the C (compact) segment, which is the only category where ICE vehicles are still present. BYD’s upcoming (not so) compact hatchback is surely needed here.

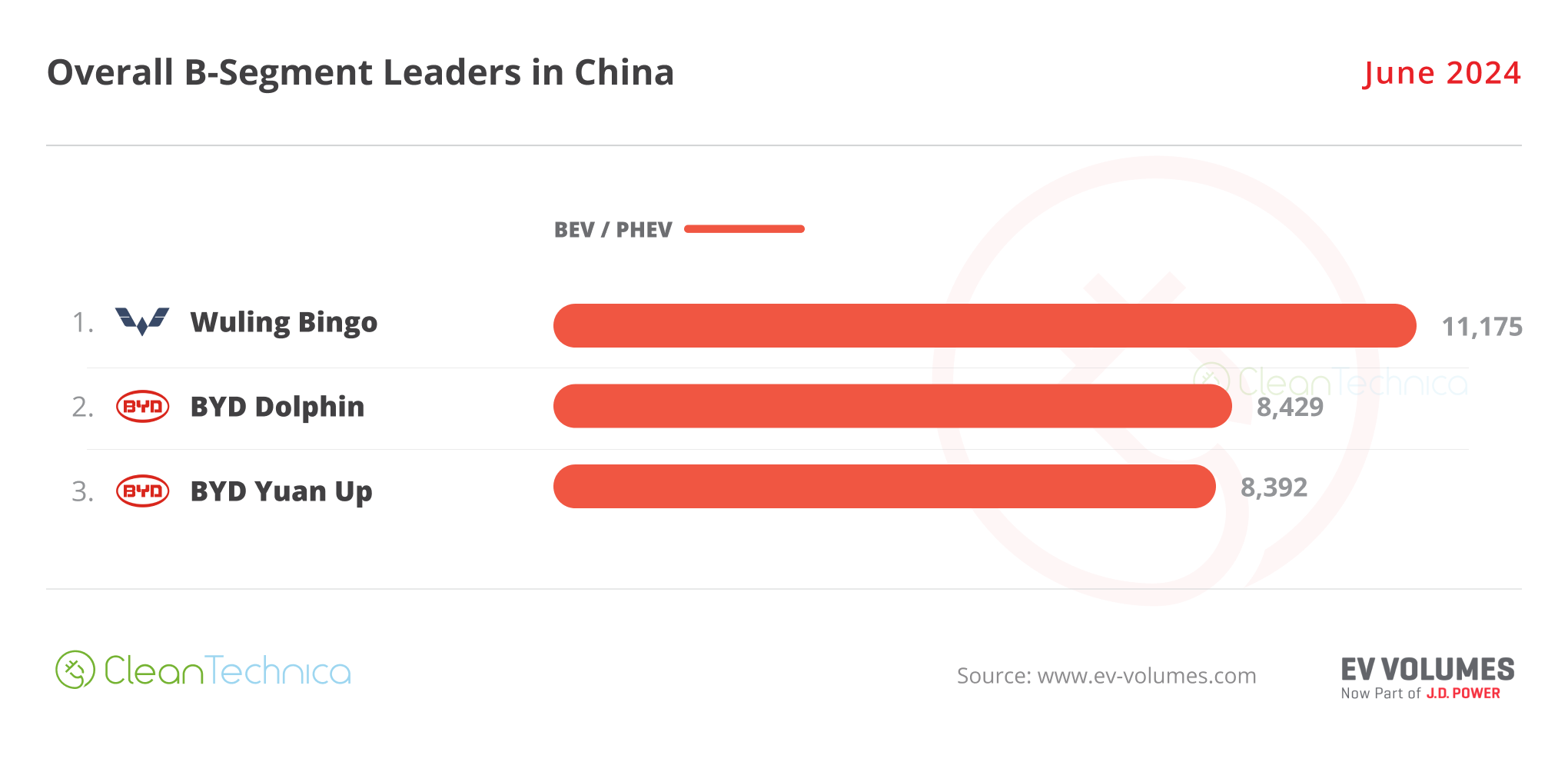

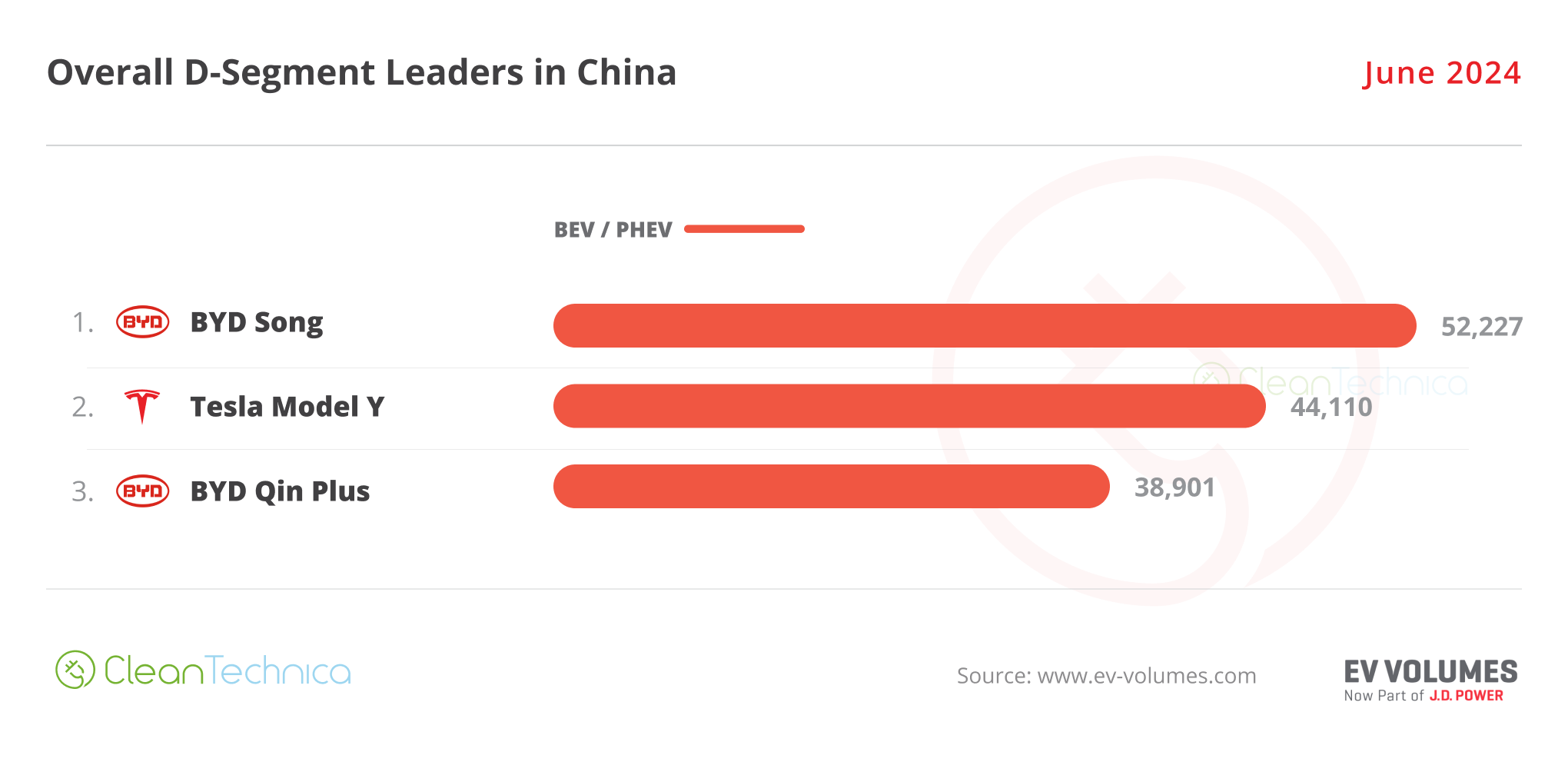

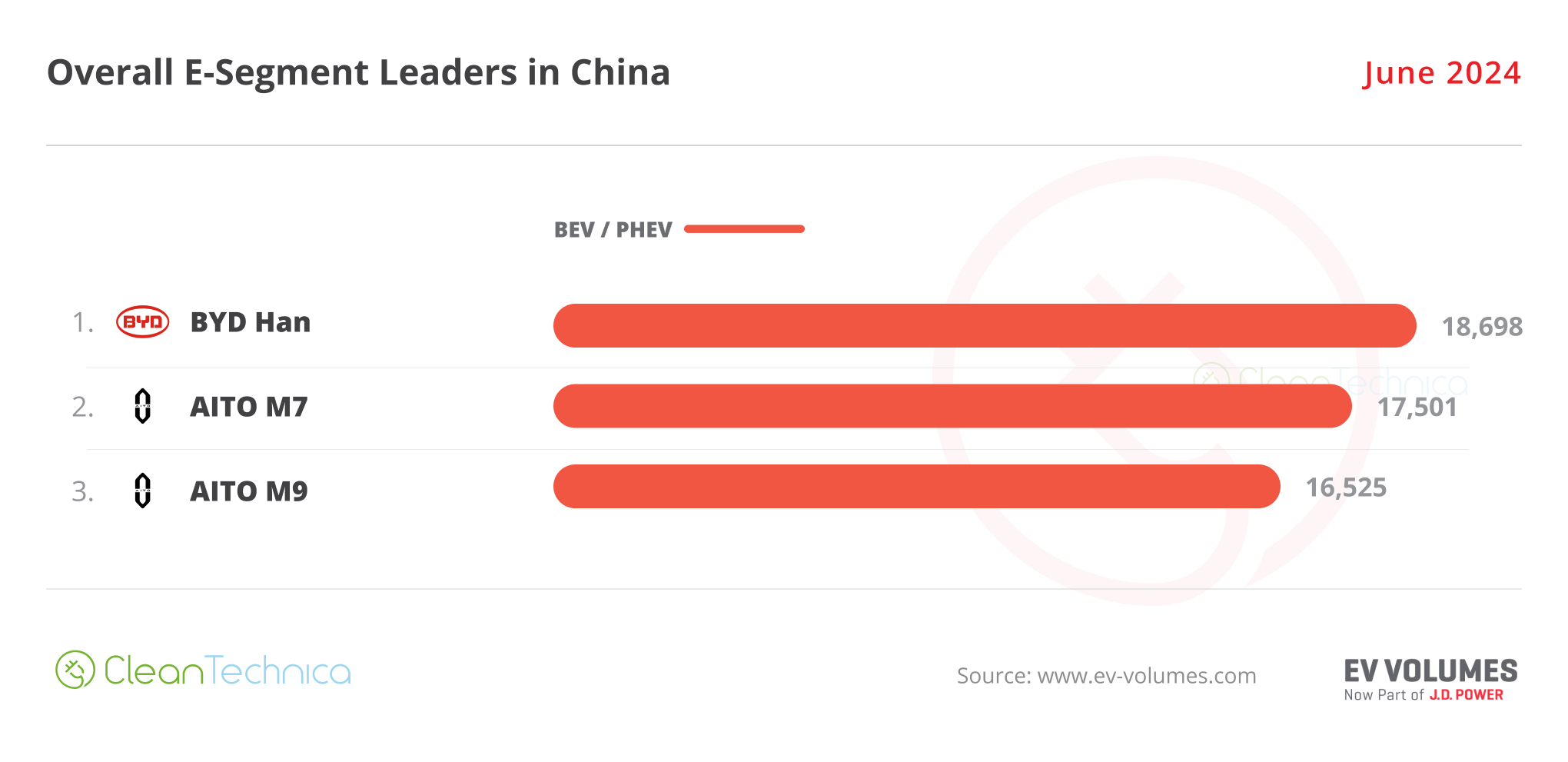

Anyhow, with the exception of the C segment, where the Nissan Sylphy still soldiers on as the sole ICE category leader, plugins rule the other size categories, with BYD ahead of every other vehicle in three categories. Meanwhile, the top spot of the B-segment/subcompact category is now in the hands of the Wuling Bingo, profiting from split sales in the BYD field — between the established Dolphin (8,429 units) and the new Yuan Up (8,392 units). The big surprises this month are coming from the full size category, with the recently introduced AITO M7 ending some 1,000 units below the leader BYD Han. We might have a close race between these two in the following months. The other, more significant surprise in the full size category is that AITO managed to place its XXL SUV, the M9, in the 3rd position, allowing this category to be 100% plugin — and it’s also now a 100% domestic podium. So, this is another category that legacy OEMs can say bye bye to.

Best Selling EVs — One by One

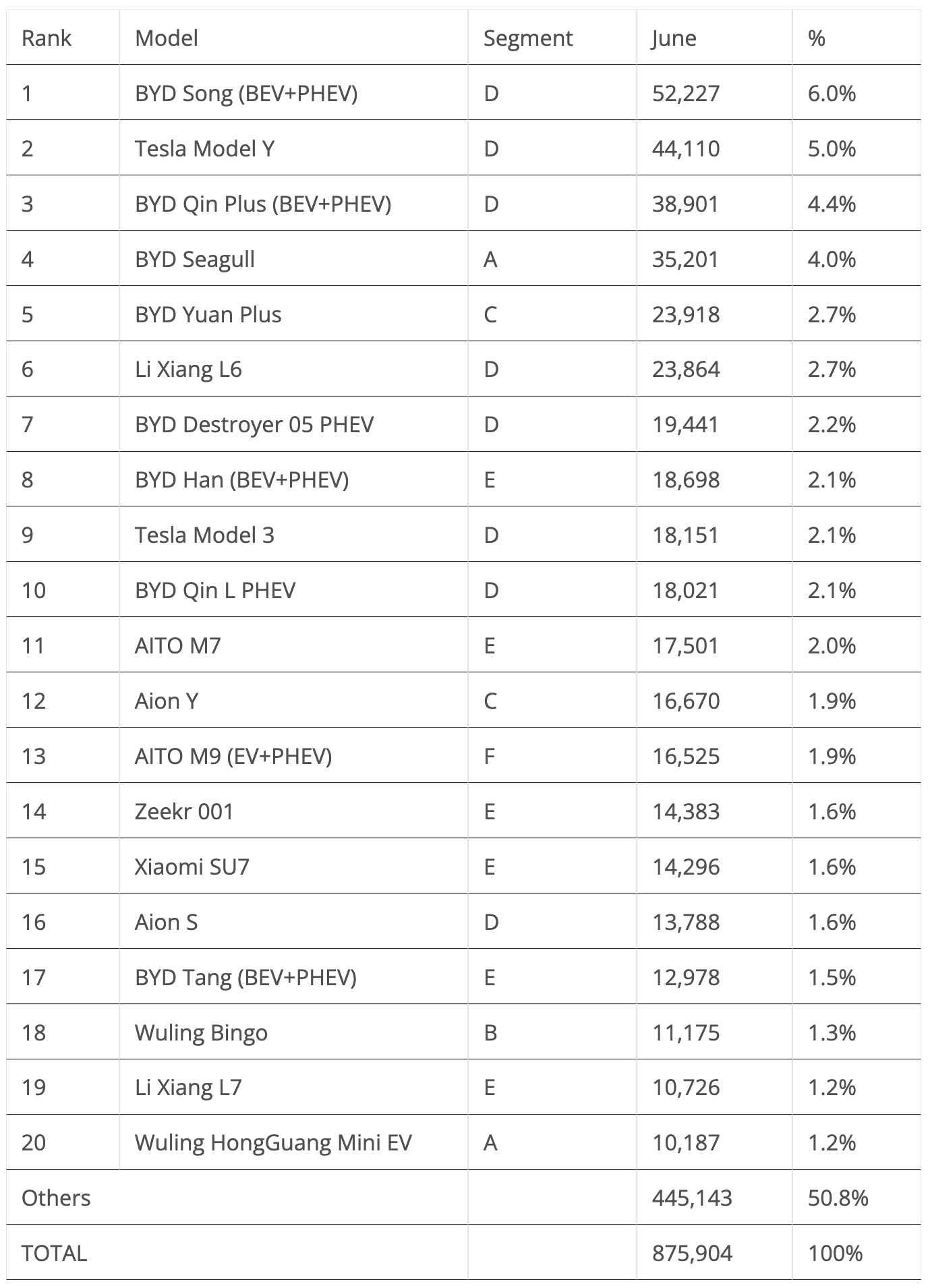

Regarding last month’s best sellers table, the top 4 best selling models in the overall table exactly mirrored the ones in the EV table — which once again proves the merging process that we are witnessing between the two tables. Here’s more info and commentary on June’s top selling electric models:

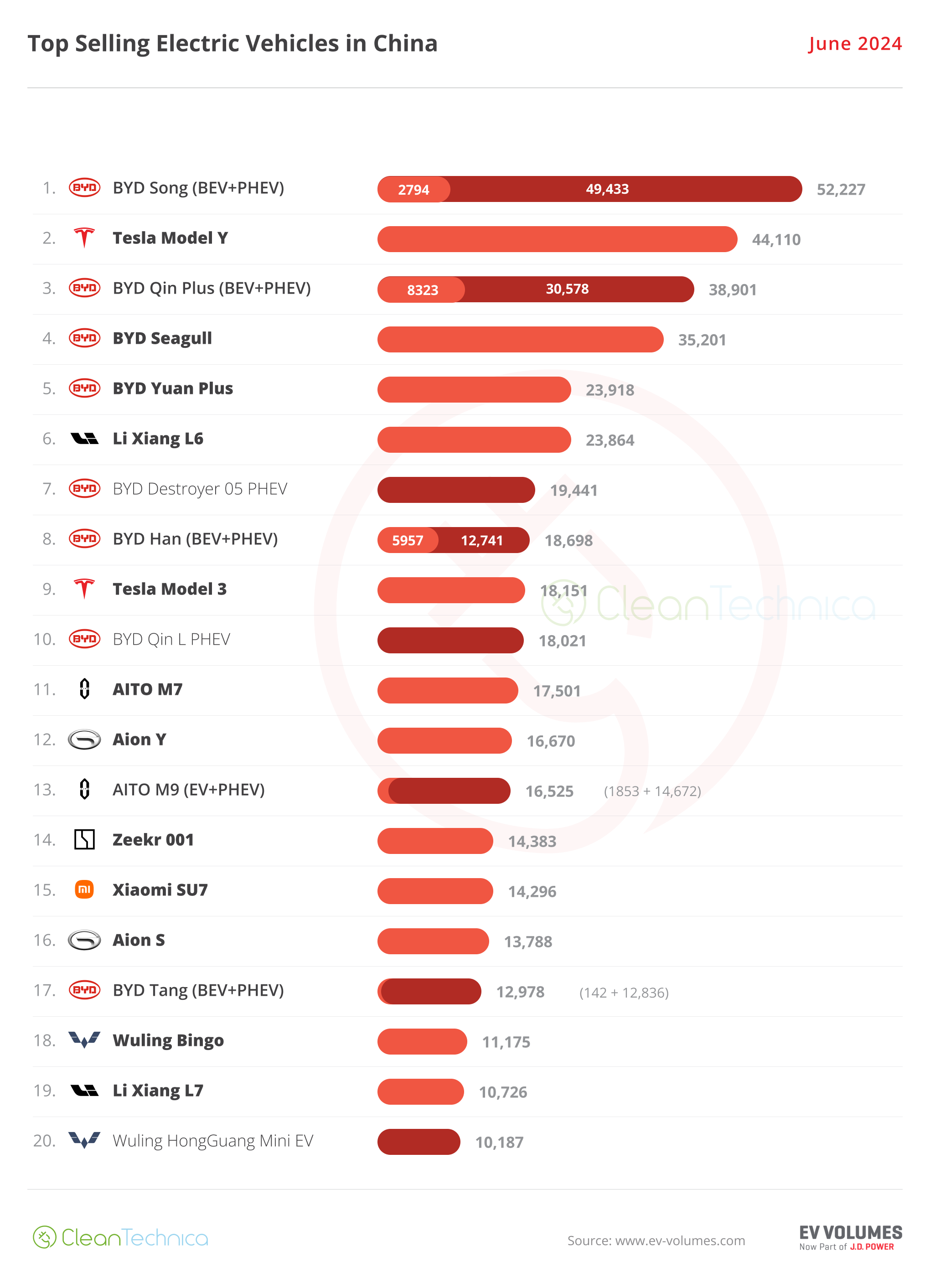

#1 — BYD Song (BEV+PHEV)

BYD’s midsize SUV is the uncontested leader in the Chinese automotive market, and the star player retained the leadership position in June, keeping its rival, the Tesla Model Y, in the runner-up spot. The midsize SUV scored 52,227 registrations, with just 2,794 units belonging to the BEV version. The new Sea Lion 07 (5,193 units in its first full month) is already hurting the Song BEV’s sales. Will the Song continue to rule in the Chinese automotive market? Well, it will depend on the competition, especially the internal competition. In the near future, the Song will have to race against tough internal competition, like the recently introduced Song L and Sea Lion 07, as well as the premium car-on-stilts Denza N7 (a car that sits somewhere between the Tesla Model Y and the Zeekr 001). All of these models also want a piece of the pie. This is probably too much competition inside BYD’s midsize SUV portfolio for the Song to continue clocking 50,000 sales/month, a necessary threshold to continue leading the cutthroat Chinese auto market, but thanks to its recent price cuts, the Song is continuing its success story.

#2 — Tesla Model Y

Tesla’s star model got 44,110 registrations, which allowed it to land in 2nd in the overall ranking. Still, the US crossover saw its sales drop 14% YoY in June. Nonetheless, the Model Y keeps Tesla relevant in the Chinese market — no small feat considering current market trends (the Tesla models were the only foreign models in June’s top 20). Interestingly, its lower-to-the-ground sibling, the Model 3, had a good month in June, with 18,151 sales, its best result this year, but it was still down 20% YoY, dropping faster than its non-facelifted sibling, the Model Y.

#3 — BYD Qin Plus (BEV+PHEV)

Along with the Song, the BYD Qin has been a bread and butter model for the Chinese automaker for a long time. The midsize sedan reached 38,901 registrations in June (8,300 units belonged to the BEV version). This allowed it to be third in the overall market, with the sedan benefitting from being the first pawn launched by BYD in its recent “War on ICE” campaign (aka price cuts). Prices start at 80,000 CNY ($12,000), and demand is bound to stay high. Despite the strong internal competition — a new, fancier Qin L (18,000 units) and a Seal 06 PHEV (7,600 units) had just started their careers — expect BYD’s lower priced midsize sedan to continue posting strong results at the cost of the competition, EV or ICE, all while keeping its external direct competitors — the Tesla Model 3, Wuling Starlight, and GAC Aion S — at a safe distance.

#4 — BYD Seagull

Things continue to go well for the hatchback model, with the small EV securing another top 5 presence thanks to 35,201 registrations. With part of production now being diverted to export markets, it seems demand for the little Lambo is now at cruising speed in China. The perky EV is now a regular in the top 5. Even with its attention now diverted to other geographies, like Latin America and Asia-Pacific, expect the little BYD to continue being part of the BYD pack that populates the Chinese top 10. What about export prospects to Europe? There are talks that the model will be launched in Europe towards the end of the year. Of course, do not expect the low prices in Europe that the Seagull has in China. When the city EV lands, as the Dolphin Mini, European prices will be significantly higher for a number of reasons (tariffs, VAT, etc.), but I wouldn’t be surprised if it started at 17,999€ … which would still be a killer price considering the direct competition is north of 20,000€.

#5 — BYD Yuan Plus

A big beneficiary of the recent price cuts, the compact crossover joined the top 5 thanks to 23,918 sales. With the upcoming launch of the BYD Seal 06 GT hatchback, sales of the Yuan Plus could suffer a bit. The new compact model is somewhat bigger than its crossover sibling (4.63 mt vs. 4.46 mt) and it has a more attractive design, especially inside, which might steal sales from the Yuan Plus. One thing is certain: after so many midsize sedans and crossovers, it was about time for BYD to launch a compact hatchback!

BYD’s Domination in the Top 20

Looking at the rest of the best seller table, there were six BYDs in the top 8 positions. And that’s not all….

… Looking at the rest of the table, we have an amazing eight BYDs, with the surprise being the new BYD Qin L, which shot to 10th in its first full month of sales!

And this kind of domination is happening at a time when BYD has several potential best selling models landing (the aforementioned Qin L, but also the Sea Lion 07, Seal 06 PHEV, Seal hatchback …). Sure, at this point, these models will likely cannibalize existing BYD models, but they will likely also steal sales from the competition.

Although, one starts to wonder at what point BYD’s new model launch fever will start to get counterproductive…. How much is too much?

More Top 20 Notes

Outside the BYD Galaxy, the big highlight is the Li Xiang L6 midsize SUV jumping to 6th, in only its 3rd month on the market. Will we see it break into the top 5? It could well be a breath of fresh air in the top 5, which has been under the leadership of BYD, with only the Tesla Model Y breaking the dulness of the Chinese automotive top sellers.

The AITO M9 was #13, with a record 16,525 sales, 1,853 of them belonging to the BEV version. The flagship AITO is the make’s most recent model, and probably the best of the make so far, so expect the 5.2-meter (205-inch) land yacht to become a frequent presence in the table and a serious contender to the XXL SUV category title, with top 5 presences also a possibility.

The Zeekr 001 was also beating records, in 14th, thanks to 14,383 sales, its best result ever. The flagship model took full profit from the recent refresh.

A final note on the Xiaomi SU7 model: The highly anticipated value-for-money king joined the table in #15, with 14,296 sales, the first time the sporty sedan broke into 5 digits. With over 100,000 units expected to be delivered this year, expect the SU7 to make further jumps in the overall table, maybe reaching the top 5 in a few months.

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Outside the top 20, as usual, there was a lot to talk about, like NIO’s ET5, which reached a record 8,557 sales in June, its best score in the last 17 months.

As previously mentioned, BYD launched a bunch of new models, like the BYD Qin L and its sportier twin, the BYD Seal 06, with both PHEV sedans focussing on value for money. On the crossover side, the Sea Lion 07 is a new BEV midsize crossover, serving as counterpart to the Song L, in the “Ocean Series” lineup.

Looking at foreign OEMs, the two highlights refer to the BMW i3, the China-only BEV version of the 3 Series sedan, which scored a record 6,952 units in June, and the Volkswagen ID.4, which had a year-best score of 6,854 units.

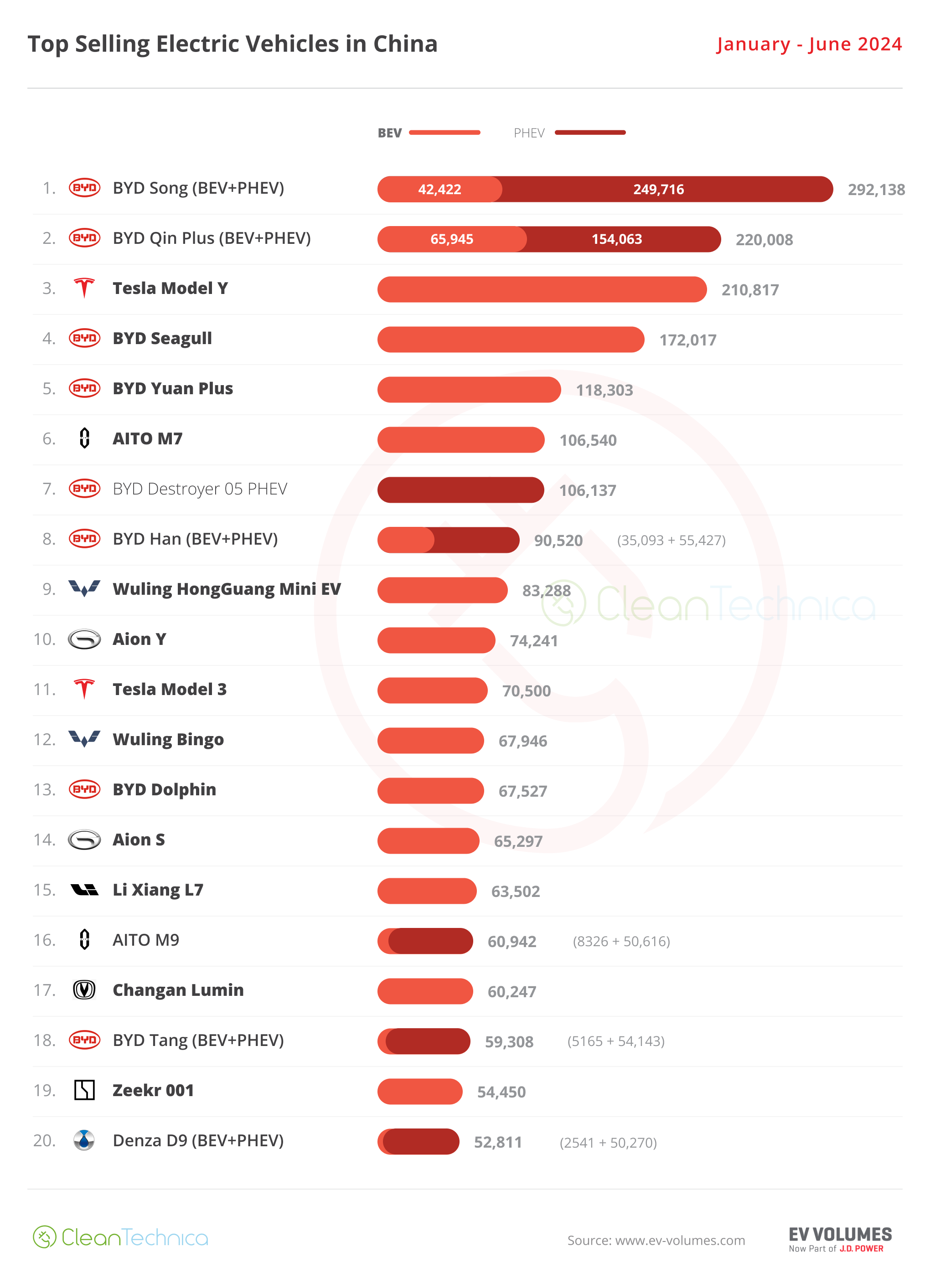

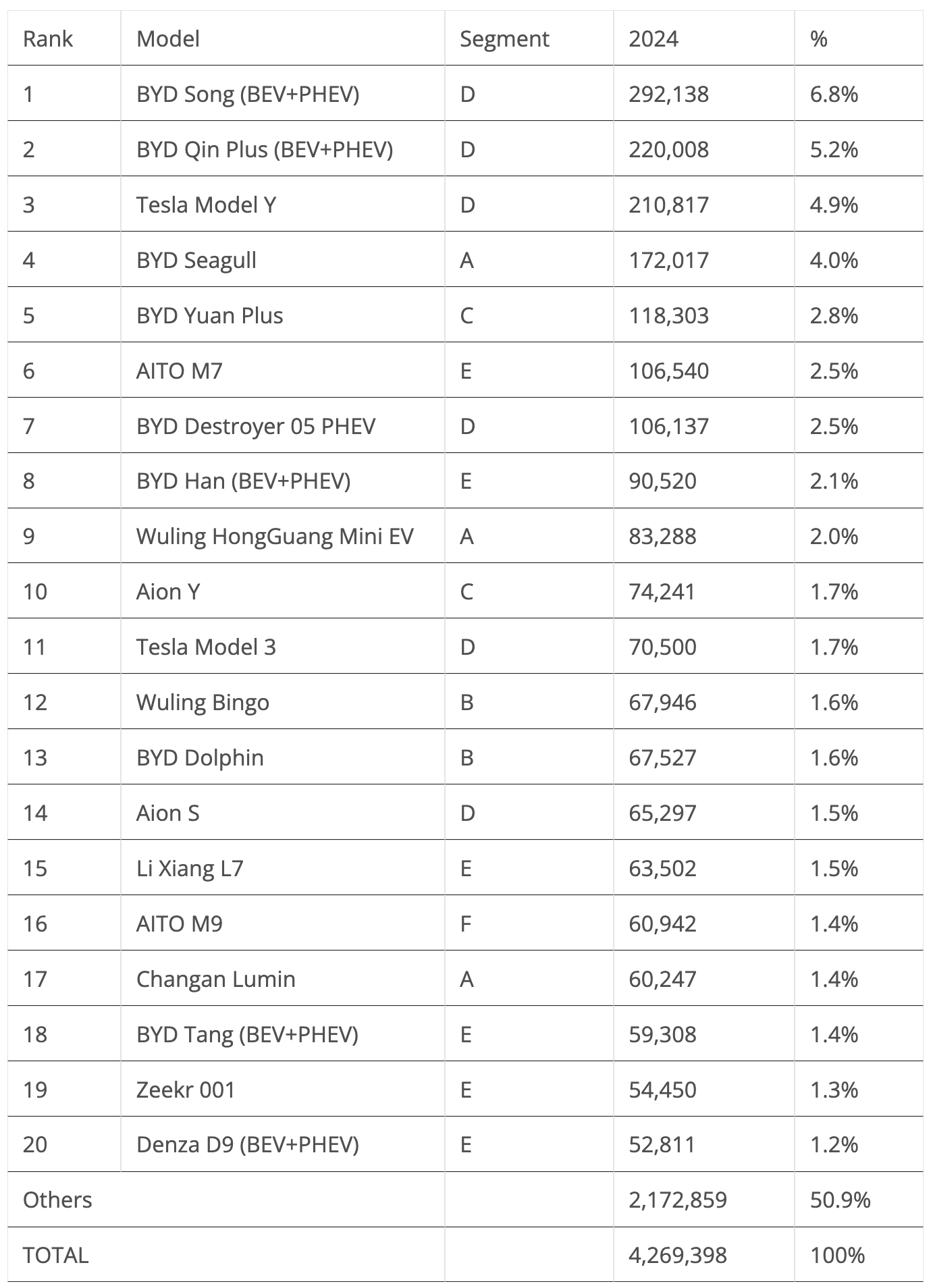

The 20 Best Selling Electric Vehicles in China — January–June 2024

Looking at the 2024 ranking, there’s nothing new in the podium positions, with the podium bearers BYD Song, BYD Qin Plus, and Tesla Model Y safely in their positions.

The same can be said about the 4th placed BYD Seagull, which has distanced itself from the competition — more than 30,000 units separating the little Lambo from the #5 BYD Yuan Plus or the #3 Tesla Model Y.

With the top 4 positions already secured, we have to go down to the 6th position to see some action. The rising #7 BYD Destroyer 05 is now some 400 units from the big SUV AITO M7. So, we might see the hot selling BYD surpass it in July already.

Further down, the Aion Y climbed yet another position, to #10, with the crossover-MPV mashup looking to jump a few more positions in the table soon.

Good news for the Tesla Model 3: profiting from the expected peak performance of June, the US sedan was up three positions, to 11th. Realistically, this is the best that the Model 3 can expect from this market.

Regarding the lower positions on the table, Aion S confirmed a positive month for the GAC brand, with the sedan climbing one position to 14th. The AITO M9 yacht full-size SUV also had a positive month, jumping two positions, from #18 in May, to its current #16 spot.

Finally, in #19, we have another full size model joining the table, as the Zeekr 001 is benefitting from its recent refresh to jump several positions. The flagship Zeekr is the 7th full size model in this top 20, making this category the most represented in the table, which says something about the tastes of local buyers, but also about the quality of Chinese OEMs. Long gone are the days when “Chinese car” rhymed with “Cheap, basic econobox.”

Changes in the Overall Brand Ranking

In June, the top three positions mirrored the 2023 full year ranking, with BYD on top followed by Volkswagen and Toyota. The dynamics are quite different, though. BYD (265,000 sales) grew 20% YoY, while #2 Volkswagen (157,000 sales) was down by 18% and Toyota (133,000 sales) fell by 15%. So, while the first place automaker is still rising fast, the other two are losing significant ground in a fast changing market.

Confirming the domestic takeover, #4 Geely (84,000 sales) had a 2% growth rate, while #5 Honda (69,000 sales), the 4th best selling brand in 2023, crashed 39% YoY. At this rate, Honda’s future looks bleak in China….

#9 Tesla dropped 20% YoY in June, with the best selling US brand in China selling 60,000 units. That’s a stark contrast to some Made-in-China startups, like AITO (+700% YoY), NIO (+98%), and Zeekr (+89%), which are expanding its sales quite fast.

Still, there are others worse than Tesla, and just giving some examples of famous brands, Buick was down 47% in June; Cadillac dropped by 46%; Chevrolet did even worse, cratering a worrying 82%(!); and not wanting to make of this a GM-bashing show, even the all-mighty Volkswagen Group saw its daughter brand Skoda drop significantly (-47% YoY). At this pace of falling sales, several legacy brands and OEMs will have no other solution but to leave the Chinese market in the near future.

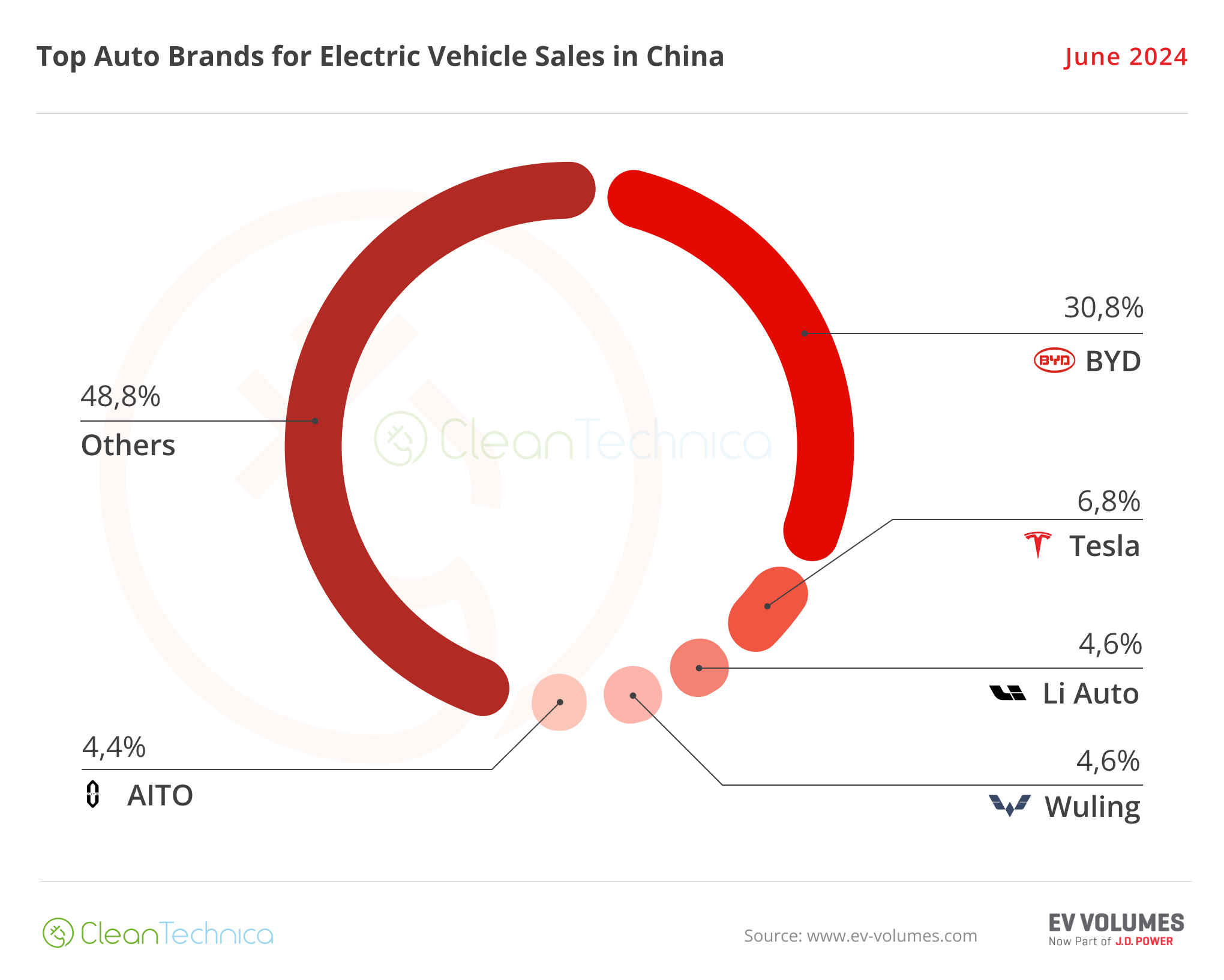

Auto Brands Selling the Most Electric Vehicles in China

Looking at the auto brand ranking, there’s no major news. BYD (30.8%) is firm in its leadership position, and there’s really no way to see this domination ending anytime soon.

Things get more interesting below, though. Tesla (6.8%, up from 6.6%) is now comfortable in the runner-up spot, Li Auto (4.6%, up from 4.3% in May) jumped three positions, to 3rd, benefitting from the popularity of its new L6 model and helped by another bad month from Wuling (now at 4.6%, down from 5.1% — SAIC’s low-cost brand is one of BYD’s War on ICE victims).

Geely also suffered from the recent BYD price cuts, and it has seen its share drop to 3.9% in June, losing its top 5 position on the way. With the tiny Panda Mini (9,154 units) and the Galaxy sub-brand performing below expectations, the Chinese brand is finding it hard to follow the pace of the best selling brands.

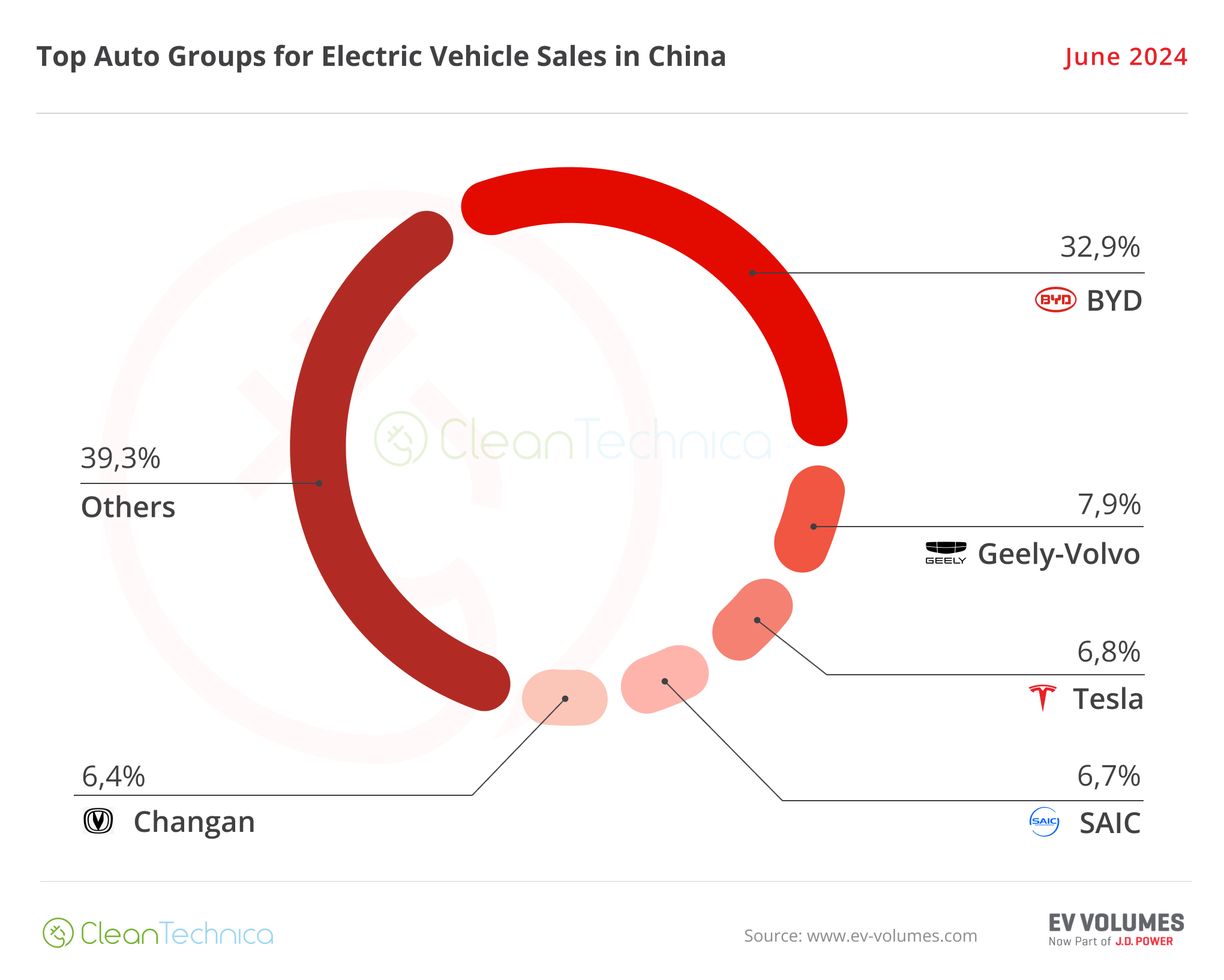

Auto Groups Selling the Most Electric Vehicles in China

Looking at OEMs/automotive groups/auto alliances, BYD Group is comfortably leading, with 32.9% share of the market. That increase in share is mostly thanks to the strong results of the namesake brand. At this moment, it seems BYD has its domestic market domination assured, replicating what Tesla is doing in the USA.

Geely–Volvo is a distant runner-up, with 7.9% share, all while Tesla (6.8%) surpassed SAIC (6.7%) in the race for the last place on the podium.

#5 Changan (6.4%) is currently stable, and could profit from SAIC’s current sales blues to climb another position soon.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Videos

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy