Plugin vehicles are all the rage in the Chinese auto market. Plugins scored over 700,000 sales last month, up 28% year over year (YoY). That pulled the year-to-date (YTD) tally to over 3.2 million units.

Share-wise, with June showing another great performance, plugin vehicles hit 38% market share! Full electrics (BEVs) alone accounted for 25% of the country’s auto sales. This had the 2023 share at 35% (24% BEVs), and considering the current growth rate, we can assume that China’s plugin vehicle market share will end over 40% by the end of 2023.

Another measure of the importance of this market is the fact that China alone represented around 60% of global plugin registrations last month!

Looking at June’s best sellers in the overall market, we see plugins populating the top positions, with 4 plugin models in the overall top 5. And to think: in other markets, we celebrate when one EV breaks into the overall top 10….

But looking at the best sellers by category, we see that some still need a heavy dose of electrification:

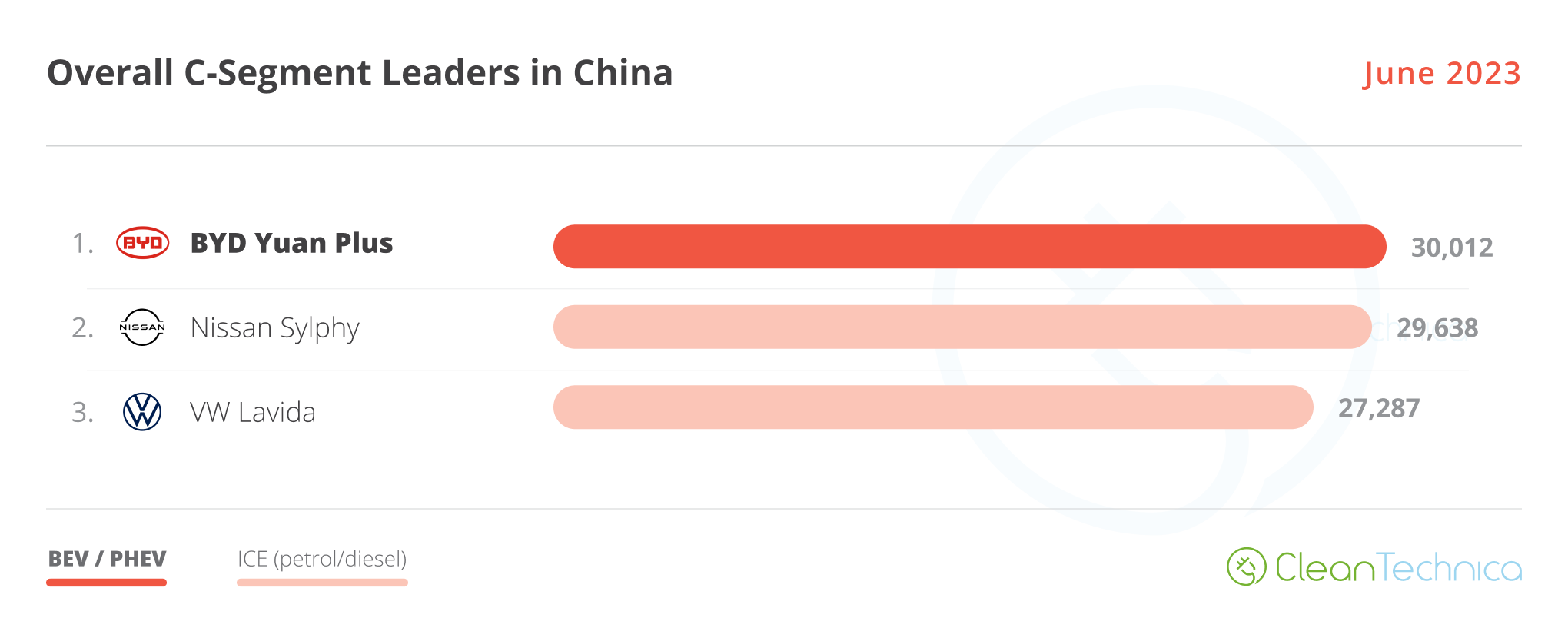

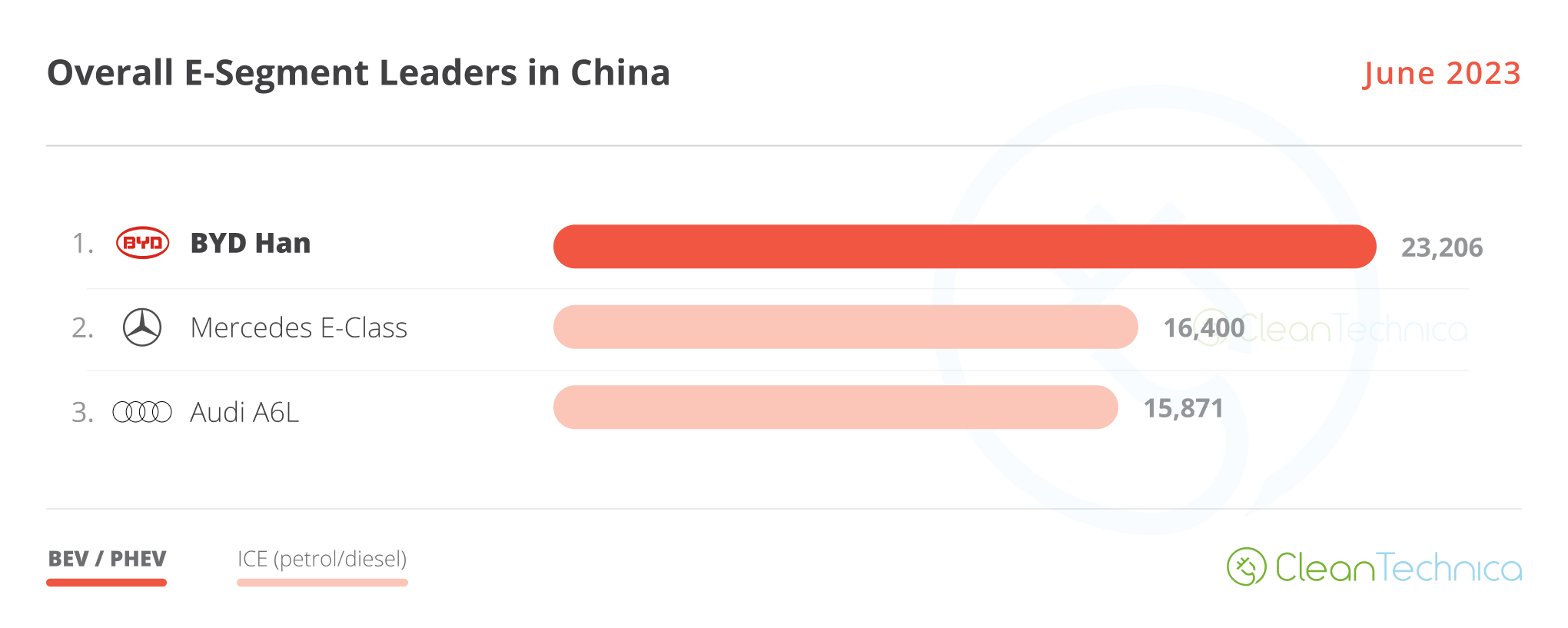

As we can see, while city cars (A-segment), subcompacts (B-segment), and the midsize category (D-segment) are heavily electrified, compacts (C-segment) and full size (E-segment) models still have some work to do.

The full size category is a real case study, as the premium German models remain on top despite the fact that they are essentially ICE-based models. Is it a case that having a big, luxurious ICE car in China is the ultimate synonym of luxury?

The 20 Best Selling Electric Vehicles in China — June 2023

Here’s more info and commentary on June’s top selling electric models, with only BYDs and Teslas in the top 7 positions:

#1 — Tesla Model Y

Tesla’s star model got 51,471 registrations, which allowed it to be the best selling model in the overall market in China. It seems the price cuts have gone well for the US crossover, with the midsizer being able to run at the same pace as the best of the BYD pack. Watching the Model Y’s Q2 sales on an average quarterly basis, thus removing the Tesla factor of valley/peak months, the Model Y ended the quarter with a 36,500 unit/month average, which is a great result for a foreign model in China. In a time when Chinese automakers are in peak form, Tesla is currently the only foreign OEM able to follow the amazing pace of the domestic carmakers.

#2 — BYD Song (BEV+PHEV)

BYD’s midsize SUV was second in the Chinese automotive market, with BYD’s current star player scoring 43,288 registrations. So, will the Song end the year as the best selling model in the Chinese automotive market? Well, it depends on the competition, especially the internal competition. Currently, the Song only has the recently introduced Frigate 07 PHEV as internal competition, but the upcoming Song L (BYD’s take on the Tesla Model Y theme) and its premium cousin, the Denza N7, are both set to land this year. This is probably too much competition inside BYD’s midsize SUV portfolio (the regular Song as the lower priced model, the Frigate 07 & Song L as mid-priced models, and finally the upmarket Denza N7). Also, the current wave of price cuts, which is spreading through the local market, will be a decisive factor. These factors will be decisive for the Song to continue clocking 40,000-plus sales/month, a necessary threshold to continue leading the cutthroat Chinese auto market. Currently, its monthly average now sits at 43,000 units/month, which means that so far, so good.

#3 — BYD Qin Plus (BEV+PHEV)

Thanks to a recent refresh, and especially a price cut, the BYD Qin Plus has been rejuvenated and its sales have jumped again. The midsizer reached 42,887 registrations in June, with the BEV version alone scoring 11,420 registrations. With prices now starting at 100,000 CNY ($15,000), demand is strong again, despite the strong internal competition (the BYD Seal for the BEV version and the Destroyer 05 for the PHEV version). Expect BYD’s lower priced midsize sedan to continue posting strong results, at the cost of its most expensive siblings. It should have no problem keeping its most direct competitors, the Tesla Model 3 and GAC Aion S, at a safe distance.

#4 — BYD Yuan Plus

With 30,012 registrations last month, BYD’s current star player in export markets is also not neglecting its sales in its domestic market. Will the compact crossover continue to grow, both internally and overseas? Outside China, the answer is a resounding “YES,” with the compact EV just starting its career in several markets and still to land in many more. The answer in its home market is … “Maybe.” Considering the current price war in China and the ever increasing competition (the upcoming Zeekr X being just one of many), I believe BYD will focus production of its crossover on export markets, where competition is less blood thirsty and margins are higher.

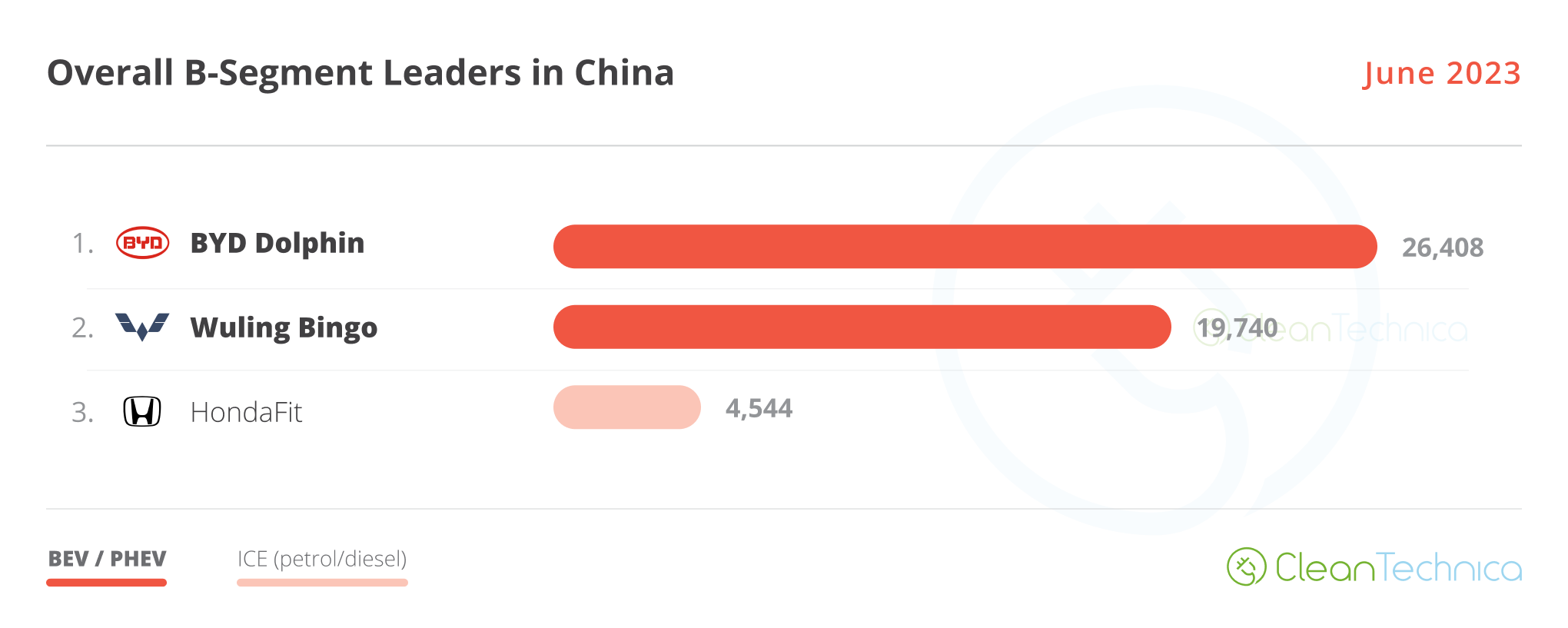

#5 — BYD Dolphin

The small-to-compact Dolphin scored 26,408 registrations. In the past, one could say that the Dolphin had its class all to itself, as its most direct competitors in this category were selling significantly less. This success is now being tested by the recently introduced Wuling Bingo, which clocked a record 19,740 performance in June. Once the Bingo crosses the 20,000 units/month threshold, it could give the Dolphin a run for its money. The race in the small hatchback category could become even more entertaining to follow if the upcoming JAC Yiwei 3, said to receive sodium-ion batteries later this year, also becomes a success.

Looking at the rest of the table, below BYD’s and Tesla’s best sellers, GAC’s Aion S & Y continue to impress, with the sedan ending the month in 8th and the MPV-disguised-as-a-crossover in 9th. Will GAC models be able to reach podium positions? That would at least bring some extra color to the boring and predictable BYD–Tesla domination in the top positions. To be continued….

The main highlight in the top half of the table is the #10 Wuling Bingo scoring a record 19,740 sales, not only beating its smaller sibling Wuling Mini EV, but also now looking to reach the sales levels of the category leader, the BYD Dolphin.

Just below, SGMW’s new baby, the #11 BYD Seagull, had 16,560 sales. That’s a great performance for the little EV, considering it is only in its 3rd month on the market. We might see it jump into the top 5 in September.

Further below in the table, a highlight was in #14, the Li Xiang L7 — the startup’s new full-size, 5-seat SUV (the L9/L8/L7 are all full-size SUVs). The new model had another record month (13,107 registrations). The hot startup brand has another winner on its hands. The cheapest model in the startup lineup (it starts at $49,000) should continue to improve its standing in the near future, with the startup make setting a bullish sales target of 400,000 units this year! And 800,000 in 2024!! And 1.6 million in 2025!!! :0

For these targets to be met, the midsize L6, due to be launched sometime next year, will be a critical part of the puzzle.

Still on the top 20, three other models deserve a mention. The #16 Denza D9, a 21st century-limo large MPV, hit a record 11,058 units, the #17 BYD Destroyer 05 had its first 5-digit performance (10,222 units), while in #18, we have Geely’s Galaxy L7 PHEV, which landed on the market with a bang. Now, will this mean that the Galaxy’s sedan is destined for success? Maybe. Geely has a long line of models that started strong but dropped into irrelevance a few months later. Now, will Geely’s sleek sedan be just another case of the boom–bust story? Discuss.

Outside the top 20, the highlights are varied. In Great Wall’s stable, the ORA Good Cat had 7,658 registrations, its best score in a year. The WEY premium brand delivered 5,506 units of its new Blue Mountain flagship SUV, in only its third month on the market. With a 45 kWh battery, extended-range technology, and full-size length, it is hoping to capture some of Li Auto’s mojo in that category. A future best seller?

Meanwhile, Leap Motor’s C11 midsize SUV scored another record performance, with 8,934 registrations, no doubt helped by the introduction of a range-extended version that is now sold along the regular BEV version. Meanwhile, FAW has shown signs of life, with the Bestune NAT people carrier reaching 5,387 registrations, the MPV’s best score in 18 months. Is FAW finally looking seriously at EVs?

The 20 Best Selling Electric Vehicles in China — January–June 2023

Looking at the 2023 ranking, the BYD Song is well above the competition, while the runner-up BYD Qin Plus has resisted the peak sales of the Tesla Model Y. But will the Chinese sedan continue resisting the US crossover in the future?

Off the podium, the table has remained stable, with the first position change happening only in #13 with the Wuling Bingo jumping four positions to #13. The small EV hopes to reach higher standings (#11? #12?) in July.

Finally, we have the Li Auto L7, which joined the table in June, jumping to #17. That makes three Li Auto models in the top 20. Apart from the all-mighty BYD, no one else has that many models in the top 20, and it speaks volumes about the startup’s current strength.

Top Selling Auto Brands & Auto Groups in Chinese EV Market

Looking at the auto brand ranking, there’s no major news. BYD (35.3%, down 0.7%) remains stable in its leadership position and is looking to win its 10th plugin automaker title this year, while peak Tesla (9.1%, down from 8.7%) is stable in second place.

Third-placed GAC Aion remained stable, at 6.5%, while the SGMW joint venture’s performance was hurt by the Wuling Mini EV sales drop, which wasn’t completely offset by the “Bingo-effect,” dropping its share from 6% in May to its current 5.8%.

Finally, 5th placed Li Auto continues on the rise (4.3%, up from 4.2%). This three-year-old startup is already reaching significant sales levels and looks set to become a force to be reckoned with in the future.

Despite staying off the radar of many analysts, Li Auto’s growth potential, price points, and margins are the most promising among current EV startups. Just to put the company’s amazing growth curve into context, in 2015, three years after the Model S launch, Tesla was celebrating a record 50,000 unit sales a year. At the same age, Li Auto does more than that in two months….

Comparing the top sellers now with what was happening a year ago, while BYD (+8.4% share), Tesla (+0.8%) and GAC (+2.3%) are on the rise, SAIC’s sales bleed has become apparent. The Shanghai-based OEM lost a full 4% share compared with June 2022.

Finally, looking at the overall top 20 ranking, the fastest growing brands are currently the #1 BYD (+72% YoY), #7 GAC (+41%), and #18 Li Auto (+130%!).

This is kind of a perfect s*** storm for legacy OEMs in China, with BYD and GAC going after their mainstream market volumes, Tesla hitting their midsize/premium offers hard, and Li Auto eating its way into the last bastion of profitability for foreign OEMs in China: full size models.

Looking at OEMs/automotive groups/alliances, BYD is comfortably leading with 37% share of the market, while #2 Tesla (9.1%) also remains stable. With the SAIC mothership still in the red, the new Wuling Bingo was not enough to stop the current sales bleed — the Shanghai-based OEM was down from the 7.6% share it held in May to its current 7.4%, which nevertheless was still enough to allow it to retain the last position on the podium.

But with #4 GAC (6.9%) getting closer, SAIC could have its bronze medal in danger soon.

One step down, #5 Geely–Volvo is stable at 5.5% share, up 0.3% share compared to the previous month.

With #6 Changan stable at 4.5%, Geely can rest on its laurels for now while it prepares a way to surpass SAIC and/or GAC by the end of the year. (And maybe go after Tesla in 2024?)

I don’t like paywalls. You don’t like paywalls. Who likes paywalls? Here at CleanTechnica, we implemented a limited paywall for a while, but it always felt wrong — and it was always tough to decide what we should put behind there. In theory, your most exclusive and best content goes behind a paywall. But then fewer people read it! We just don’t like paywalls, and so we’ve decided to ditch ours. Unfortunately, the media business is still a tough, cut-throat business with tiny margins. It’s a never-ending Olympic challenge to stay above water or even perhaps — gasp — grow. So …